The Oil Glut and the Fallout

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

They call it an oil glut for a reason.

There is too much oil in the system today. The U.S. fracking revolution has added four million barrels of oil to the global supply per day. However, that is just the U.S., and that is just since 2009. Since 1996, it is gone up about 15 million worldwide.

As the world economy has slowed, oil production has ramped up. How could that not end badly?

They call it an oil glut for a reason.

There is too much oil in the system today. The U.S. fracking revolution has added four million barrels of oil to the global supply per day. However, that is just the U.S., and that is just since 2009. Since 1996, it is gone up about 15 million worldwide.

As the world economy has slowed, oil production has ramped up. How could that not end badly?

The crisis has emerged in the past year as oil fell from $115 to $43. Even today’s $60 levels threaten to dismantle many oil producers. Most cannot keep up with the leading producers like Saudi Arabia that operate at absurdly low production costs.

So many look to news that the oilrig count is dropping as a sign that oil will return to triple-digit levels. They think producers will re-inflate the bubble, and soon!

Let me be clear: Oil will not rise above $100 for the next decade or longer… and I continue to predict that it will fall to $10 to $20 in the next several years ahead. That is because much of the oil industry today is built upon a mirage.

When oil crashed from $147 to $32 in a matter of months in 2008, the artificial recovery eventually propped it back up to $115 by 2013. This was thanks to QE and global stimulus.

This and the falling yields on junk bonds helped launch the “fracking revolution” in the U.S. Yields fell from as much as 10% down to 5.5%, and drillers swept this up to fund their operations while investors threw $1 trillion-plus into the enterprise.

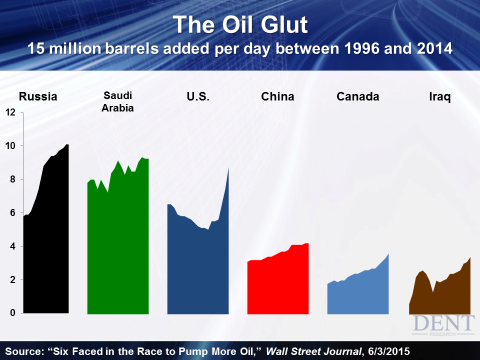

Thanks to the conditions of a drugged-up global economy, the U.S. has shifted (temporarily) from a leading importer of oil to a leading producer. Nevertheless, as I said, other countries have added to the glut.

Russia has added four million barrels to daily production since 1996. China and Canada together have added 2.5 million in that time. In addition, since 2002, Iraq and Saudi Arabia have added another two million each. Just see the chart:

With so many countries competing against each other — driving the supply higher and the price of oil lower — many are operating at their breakeven prices, or lower. They all want greater market share… but at what price?

Saudi Arabia’s breakeven cost is a mere $7 dollars a barrel, but its breakeven cost to meet its bloated government budgets is $103 a barrel. That is a huge difference! Other governments with high budget breakeven costs include Russia, Iraq, Iran, Venezuela, and Nigeria.

The U.S., Canada, and China do not have this problem. If Saudi Arabia wants their market share to continue to grow, oil would have to fall to $55 and stay there… $46 if they want to knock out Russia!

This is the situation we have today. Much of it is thanks to the illusion created by QE and the artificial recovery. But if the oil industry needed an artificial recovery largely driven by QE to save it… QE will be the thing to kill it, too.

I explained last week that the QE policies that have propped up our global economy are finally beginning to crack. When they do, oil costs will fall dramatically. Just remember, it did not even hit rock bottom when it fell to $32 in 2008.

Therefore, up until this point falling oil prices have been more a matter of rising supply. But the next stage will be a collapse in demand. That collapse has already started and will accelerate in the years ahead. Not all of this competition between oil producers today will even matter!

I continue to predict oil will hit $10 to $20 between 2020 and 2023. Most of that drop will happen by early 2017 or so alongside a greater market and economic crash.

I have been saying for years that commodities would fall in the later part of this decade. Many economists and gold bugs were saying they would rise. They do not see that the emerging countries that rely on commodity exports have been crushed when this commodity downturn happens!

Oil will eventually come off of these long-term lows. And the average for the next several years will be more like $40. However, this collapse will force the oil industry to go through a massive consolidation that impacts oil companies around the world.

For the U.S., that means forgetting the 200,000-plus jobs growth we have had for a few years. Much of that jobs growth has come from this sector. And that means that now is not the time to invest in oil. Oil could rise higher with more wells shutting down over the next few years due to falling oil prices — IF the competition amongst producers was the only factor.

Considering the larger threat of a global economic downturn, they are destined to fall much, much lower.

Deflating the Oil Glut: First Supply, Then Demand is republished with permission from Harry Dent Jr.