Wynn Resorts Stock Down 11% – Time to Buy WYNN Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Wynn Resorts stock went down as much as 11% yesterday at $92.25 per share while its price is dropping nearly 6% in pre-market stock trading action today amid news about a potentially steep license renewal process in the corporation’s most important location – Macau.

According to an exclusive report from Reuters, Macau’s government has opened a 45-day consultation on the renewal of gaming licenses for operators within one of the world’s largest and most profitable gambling hubs as officials seek to improve working conditions while ensuring the legality and transparency of all operations.

As part of this regulatory overhaul, Beijing authorities are also aiming to better distribute profits by demanding the participation of local investors in all projects.

Wynn Resorts operates two of the largest properties in Macau including the Wynn Macau and the Wynn Palace. Together, they account for half of the revenues produced by Wynn according to the latest quarterly report released by the company.

How can this regulatory crackdown affect the performance of Wynn moving forward? Is this an opportunity to buy the stock amid unfounded widespread fears about the possibility of Wynn losing its license or are risks too high to consider an investment?

In the following article, I’ll attempt to draft plausible scenarios for the stock considering these latest developments.

67% of all retail investor accounts lose money when trading CFDs with this provider.

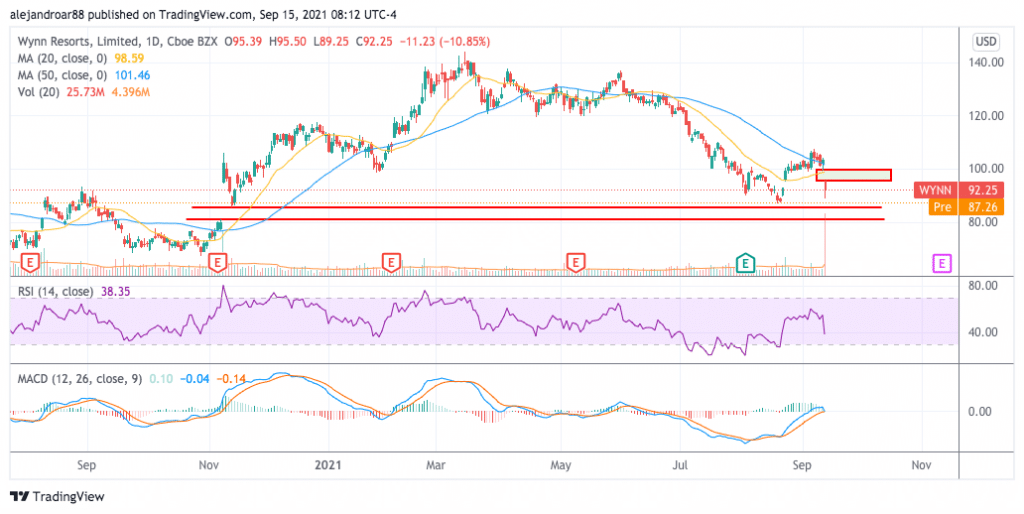

Wynn Resorts Stock – Technical Analysis

Even though a fundamental analysis of Wynn stock may be more enlightening amid the threat that the company’s operations are facing, a quick look at the technical setup could also help traders in determining potential entry and exit prices based on how the stock has behaved recently.

Yesterday’s price action led to a steep decline in the stock price and left behind an ugly bearish gap that may act as resistance moving forward, at least until the situation in Macau becomes clearer.

Trading volumes reflect the extent of the sell-off as a total of 25.7 million shares exchanged hands during the day – a figure that exceeded the daily average by more than 6 times.

Moreover, the MACD oscillator has just turned bearish as it crossed below the signal while it has now entered negative territory. The same goes for the Relative Strength Index (RSI), which has slipped to 38.

That said, it is important to note that buyers showed up yesterday to take advantage of the sell-off as the stock recovered from an intraday loss of 14% to settle at $92.25 or 11% lower.

Moving forward, the outlook for the stock is bearish until the price gap shown in the chart is filled as regulatory risks could continue to weigh on WYNN’s outlook.

Wynn Resorts Stock – Fundamental Analysis

During the earnings call that took place in August this year as part of the release of the company’s Q2 2021 financial results, Wynn’s Chief Executive, Matt Maddox, stated that he felt “really good” about the firm’s ability to renew its license to operate in the region.

License renewals for many casinos in Macau are scheduled to take place in June 2022 although some analysts have cited that this period could be extended for some of the largest operators in case they needed more time to perform the changes brought forward by regulators.

The odds of losing its license to operate in the region seem low and that doesn’t appear to be what the market is worrying about. Instead, it is the cost of any changes on the region’s regulations that may further hurt the company’s bottom-line results what could be dragging stock prices lower.

In this regard, it is important to note that Macau operations for Wynn were the most profitable for the group before the pandemic stroked as their combined adjusted property EBITDA accounted for 76% of the total back in 2019.

Therefore, a significant decline in the firm’s profitability resulting from higher labor costs or taxes may affect Wynn’s performance in the future and that is perhaps what the market is anticipating.

Moving forward, once the scope and reach of the new regulations are clearer, the outlook for the business will be clearer as well as analysts will manage to incorporate any positive or negative impact coming from these changes to their forecasted bottom-line results.

At its current enterprise value of $19.37 billion, Wynn is trading at 10.7 times its 2019 adjusted property EBITDA. This ratio seems conservative and may reflect the extent to which market participants are concerned about a decline in the firm’s ability to maintain or grow these results in the future amid the potentially long-lasting impact of the COVID-19 pandemic and these proposed changes to Macau’s regulatory framework.

Even though the valuation might seem attractive at first glance, it could also be a value trap as Wynn may struggle in the future to deliver the kind of results seen before the pandemic amid its now higher interest expenditures resulting from the additional debt it took to survive the virus downturn.

Moreover, the company’s long-term debt is quite elevated as it stands at around $10.7 billion on assets of $13 billion including $2.8 billion in cash.

All things considered, despite this latest downtick, Wynn does not seem to meet the criteria to qualify as a top value pick.

Buy WYNN Stock at eToro with 0% Commission Now!