What to Expect from Tesla’s Q1 2023 Earnings This Week?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Tesla would release its earnings for the first quarter of 2023 on Wednesday. Here’s what Wall Street is expecting from Tesla’s earnings release.

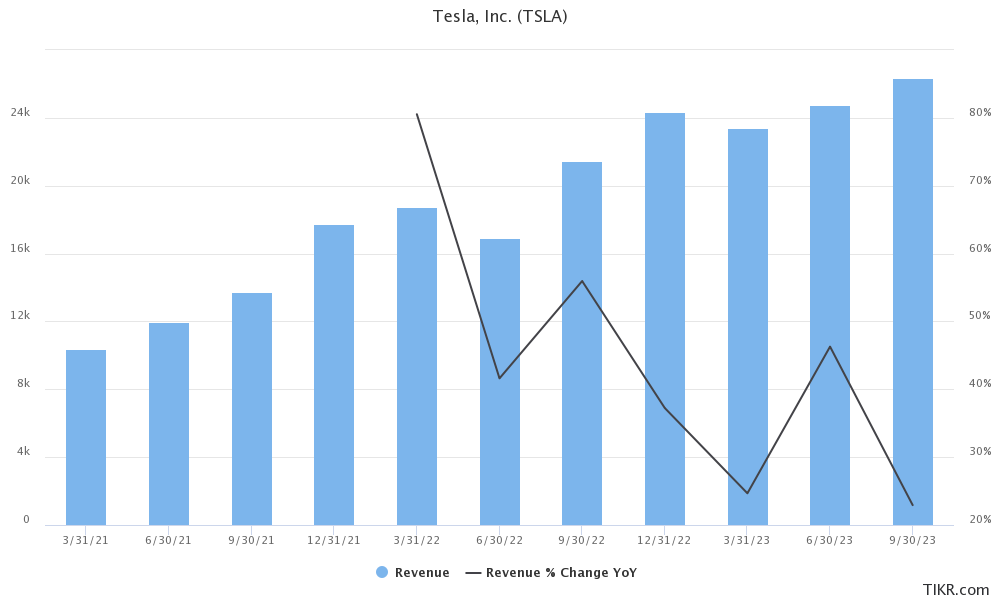

Analysts polled by TIKR expect Tesla to report revenues of $23.38 billion in the quarter, 24.7% higher than the corresponding quarter last year. While the company also gets revenues from sales of carbon credits and energy products, most of its revenues come from automotive sales.

Tesla produced 440,808 cars in the first quarter and delivered 422,875 of these. While production rose 44% deliveries rose only 36% YoY. For the last many quarters, Tesla’s deliveries have trailed production.

Tesla’s price cuts might dampen margins in the quarter

Notably, while Tesla’s deliveries rose 36% in the quarter, analysts expect its revenues to rise less than 25% in the quarter. The anomaly is due to massive price cuts. Tesla has lowered its car prices multiple times this year including in key markets like the US, Europe, and China.

The company’s price cuts have raised fears of a price war and are also expected to be a drag on its profit margins. Tesla’s gross margins fell in the fourth quarter and analysts expect margins to contract further in the first quarter.

Consensus estimates call for an adjusted EBITDA margin of 18.8% in the first quarter as compared to 22.2% in the previous quarter.

Tesla’s profits doubled last year

Tesla has now posted profits for three consecutive years and the profits have been gradually rising. The metric more than doubled last year led by higher deliveries.

The company said that its average vehicle selling prices have been coming down. It emphasized that increasing the affordability of Tesla cars is crucial if the company has to become a multi-million vehicle producer.

EV price war

Other automakers have also cut prices after Tesla which many see as signs of a price war. However, given its industry-leading margins, Tesla is better placed than others – especially the loss-making startup EV companies.

Tesla is investing in new plants and had $22.2 billion as cash and cash equivalents on its balance sheet at the end of 2022. The cash pile would help the company increase its production capacity.

What would markets watch in Tesla’s Q1 2023 earnings call?

Tesla’s automotive gross margin might be in focus during the Q1 2023 earnings call. The company has admitted that price cuts would lead to lower margins and the upcoming earnings release would provide insights into how much impact they actually had.

The company might also provide more details about its newly-announced factory in Mexico. Tesla also announced a new factory in China to produce Megapacks, its energy storage product.

Tesla might also provide an update on the ramp-up at Berlin and Austin Gigafactories. During the Q4 2022 earnings call, it said, that the Shanghai Gigafactory has the capacity to produce more than 750,000 Model 3/Y cars annually. The Freemont plant has an annual capacity to produce 550,000 Model 3/Y and another 100,000 Model S/X. Its Texas and Berlin Gigafactories, which are ramping up production fast can produce over 250,000 Model Y cars every year.

Musk Might Comment on Demand

There have been concerns over the demand for Tesla cars. Musk began the Q4 2022 earnings call by addressing the demand question and he said he wants to “put that concern to rest.”

He added, “Thus far in January, we’ve seen the strongest orders year-to-date than ever in our history. We currently are seeing orders at almost twice the rate of production. So, I mean that — it’s hard to say whether that will continue twice the rate of production, but the orders are high.”

He reiterated similar views at the company’s annual investor day on March 1. During the company’s Q1 2023 earnings call, Musk might again address the “demand question.”

Model 3 suspected images

Just days ahead of Tesla’s Q1 2023 earnings, leaked images of a revamped Model 3 car appeared on the internet. During the upcoming earnings, the company might provide an update on the rumored revamp – along with the low-cost platform that Musk talked about during the investor day.

EV competition is rising

The competition in the EV industry is rising and last month Volkswagen unveiled the ID. 2all with a starting price of around $26,600 and a range of 279 miles. The company has stepped up its game and recently announced a nearly $200 billion investment, two-thirds of which would go towards tech and electric vehicles.

Volkswagen is the market leader in the European EV market and has set itself a target of capturing around 10% of the US market share by 2030 which is over twice its current market share.

Hyundai also announced an $18 billion investment and is targeting to become the third largest EV player. Tesla is set to witness increased competition in the coming years as buyers would now have multiple EV options to choose from.

While legacy automakers were somewhat slow in realizing the pivot to EVs, they have now doubled down on efforts to ramp up their EV production capacity. Ford is targeting an annual EV capacity of 2 million by 2026 while rival General Motors, which has said that it would sell only zero-emission cars by the middle of the next decade, is targeting a 1 million EV capacity by 2025.

Analysts on Tesla’s Q1 2023 earnings

Goldman Sachs is bullish on Tesla stock ahead of the Q1 2023 earnings. In its note, it said, “We remain positive on Tesla shares, although we modestly lower our 2023/2024 EPS estimates & our 12-month price-target reflecting the lower US vehicle pricing the company instituted on 4/6/23. …. We maintain our Buy rating on TSLA shares as we continue to believe that the company is well positioned for long term growth given its leadership position both in terms of cost structure and as a full solution provider in clean mobility (e.g., software, services, and charging).”

Bard is also bullish on Tesla stock heading into earnings and said in its client note “TSLA’s leadership in scale, technology, manufacturing, cost, and depth of talent continue to differentiate it from competitors. We believe TSLA is best positioned to weather economic headwinds which appear imminent for 2H23 and believe the long-term setup is strong.”