UBER Stock Price Up 2.5% – Good Time to Buy UBER Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Uber stock is up 2.5% this morning following the successful IPO of Chinese ride-hailing company Didi Global (DIDI), which is trading 12.4% higher this morning after a choppy first day of trading.

However, Uber shares have been struggling this year as their performance has been anemic regardless of the positive impact that vaccinations have had on the company’s ride-hailing unit.

Could this be an opportunity to buy UBER stock before it breaks out? Was DIDI’s successful IPO an indirect pad on the back for the San Francisco-based mobility company? The following article takes a closer look at Uber’s fundamentals and technical setup to see if that might be the case or not.

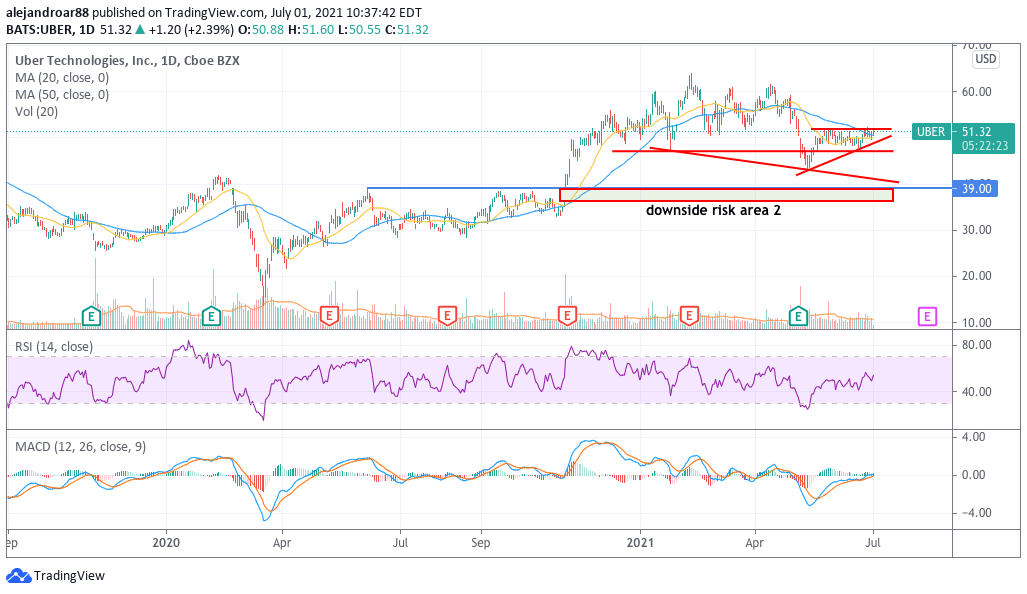

UBER Stock – Technical Analysis

The chart above shows how Uber shares have been trading range-bound between the $47.5 and $52 area lately, possibly as investors are waiting for next quarter’s results to see if the company’s ride-hailing business is recovering as expected.

An ascending triangle formation is reinforcing a bullish outlook for UBER stock. However, that directional forecast will not be confirmed until the price breaks above the $52 level – the triangle’s resistance.

If that happens, a first target for Uber could be set at $59 per share, partially aided by a decent P/S multiple. Meanwhile, further indications that the company is aggressively trimming its losses could lead to more upside as market participants should get excited about the prospect of a profitable Uber.

That said, a break below the company’s long-dated $47 support could lead to a sharp pullback in the stock price, possibly eyeing the $40 are as a plausible landing zone.

UBER Stock Price – Fundamental Analysis

Before the pandemic, Uber revenues had been growing at a fast pace, moving from $3.85 billion to $13 billion from 2016 to 2019.

However, lockdowns dealt a strong blow to the firm’s top-line results as revenues from the ride-hailing unit dropped dramatically – even though they were partially offset by the higher demand seen by Uber Eats during the same period. All in all, sales landed at $11.14 billion last year, resulting in a 14% drop compared to 2019.

This year, Uber’s ride-hailing unit is showing signs of recovering but at a slow pace. Gross bookings for the firm’s mobility segment are still down 41% compared to 2019’s figures while they also came in 38% below the firm’s 2020 readings.

As a result, mobility revenues landed at $853 million during this first quarter of the year, down 65% compared to 2020 and 2019 results. Revenues during these two periods were very similar since the pandemic impacted the firm’s revenue growth during the first quarter of 2020.

Meanwhile, Uber Eats revenues continue to become the safety net that is providing support to Uber’s top-line, with delivery revenues landing at $1.7 billion during the first quarter of 2021 compared to $527 and $536 million the unit brought in during the same period in 2020 and 2019 respectively.

Based on estimates compiled by Seeking Alpha, Uber is expected to generate $15.64 billion in revenue, which would result in a 40.4% jump compared to last year’s top-line figure and a 20.3% advance compared to 2019.

Top-line profitability for Uber has been a bit choppy but has remained within the 30% and 40% range in the past four years. However, the firm is losing sizable amounts every single year, with net losses landing at $3.94 billion last year. That said, during the first quarter of the year Uber managed to trim its losses to $108 million, down from $2.9 billion it shed during the same period in 2019.

For the next quarter, analysts are expecting to see Uber losing around $600 million, which is still an improvement compared to previous years. These lower losses are being aided by lower general, administrative, and research and development expenses.

By the end of the first quarter of 2021, Uber had a long-term debt of $7.56 billion yet its cash reserves ended the period at $6.83 billion. Moreover, the company had around $10 billion in equity investments that should be liquid enough to make this debt go away easily.

These investments include a $5.87 billion equity stake in Didi that could be worth much more than that at the moment after the firm’s successful IPO.

Based on the company’s current market capitalization of $95.33 billion, UBER is being valued at around 5 times its forecasted sales for 2021 excluding cash and highly liquid equity investments from the firm’s market cap.

This multiple is not necessarily conservatively as the company’s mobility segment has not yet fully recovered from the hit it took during the pandemic.

Meanwhile, the company’s losses continue to be quite high and they have become an obstacle for the share price to move any higher.

Buy Stocks at eToro, the World’s #1 trading platform!