Tesla Had Its Worst Week of 2023: Here’s What Analysts Are Saying

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Tesla (NYSE: TSLA) stock lost 15% last week and had its worst week of 2023. It was also a bad week for the broader markets, which notched the worst week in a month. Here’s what analysts are saying about TSLA after the recent crash

Key takeaways from TSLA’s Q3 earnings

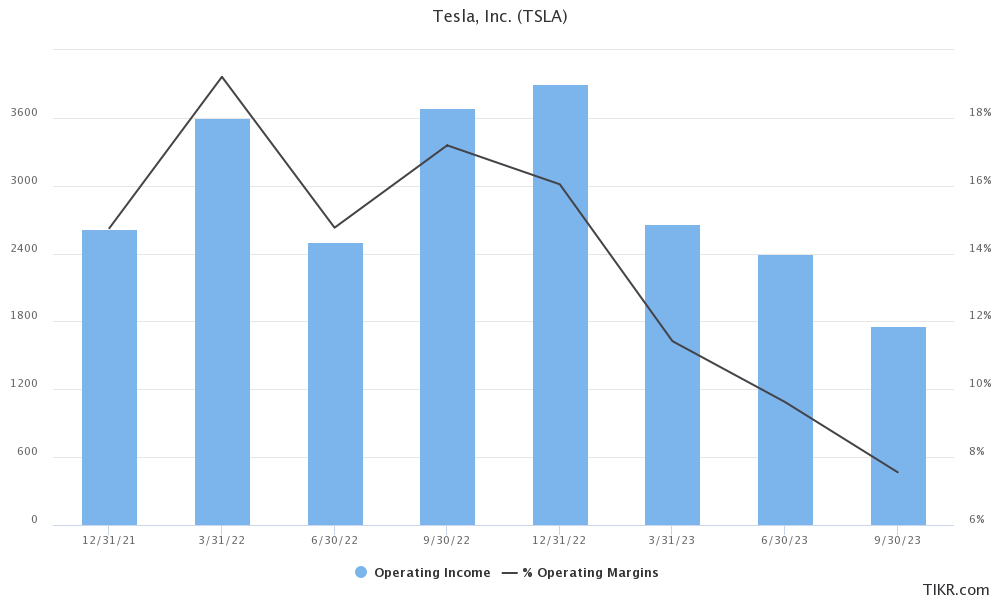

Tesla reported its Q3 2023 earnings last week. It generated revenues of $23.35 billion in the quarter which was below the $24.1 billion that analysts expected. The company’s per-share earnings of 66 cents also trailed the 73 cents that analysts expected. Notably, it is the first time in over four years that Tesla missed both topline and bottomline estimates.

The Elon Musk-run company had previously missed Q3 delivery estimates and as has been the case for the last few quarters, it lowered car prices following the delivery miss.

Tesla has been cutting car prices

Tesla’s website lists the starting price for the Model 3 at $38,990 while the Model Y at $45,990. After these price cuts, Tesla has lowered the prices of the Model 3 standard version by almost 17% in the US since the beginning of the year.

The price cuts have taken a toll on Tesla’s margins and its operating margin dipped to a mere 7.6% as compared to 17.2% in the corresponding quarter last year. The company’s margins have been falling for the last many quarters and in Q2 they fell in single digits. The deterioration in margins continued in Q3 as well.

The EV price war is taking a toll on the profits of automotive companies and companies are toning down their ambitious EV plans. Ford expects EV adoption to be slower than what it previously envisioned and said that its annual capacity would now hit 600,000 by the end of 2024 instead of this year which it previously expected. It also said that it might not hit the 2 million production capacity by 2026.

Earlier this month, General Motors also announced that it would delay the production of all-electric trucks at its Orion assembly plant to 2025.

Musk sounds alarm on the global economy

Musk, who has been predicting a recession for quite some time now and has put the blame on the US Federal Reserve portrayed a grim picture of the economy during the Q3 earnings call as well.

He said, “I am worried about the high interest rate environment that we’re in. I just can’t emphasize this enough, that the vast majority of people buying a car is about the monthly payment. And as interest rates rise, the proportion of that monthly payment that is interest increases naturally.”

He also put a question mark on the near-term trajectory of Tesla’s upcoming Gigafactory in Mexico and said, “I think we want to just get a sense for the global economy is like before we go full tilt on the Mexico factory.”

Tesla Cybertruck deliveries to begin in November

Musk also tried to temper down the expectations from Tesla’s upcoming Cybertruck. While he termed it an “amazing product” and “potentially our best product ever” he stressed “I do want to emphasize that there will be enormous challenges in reaching volume production with the Cybertruck and then in making a Cybertruck cash flow positive.”

He said that demand is not a concern for Cybertruck considering the over 1 million reservations but said that it could be upto 18 months before the product becomes free cash flow positive. While Musk was non-committal on 2024 volumes of Cybertruck he said that the company could reach an annual run rate of 0.25 million cars by 2025.

Musk harps on the AI opportunity

Musk meanwhile harped on the AI opportunity and said, “We will continue to invest significantly in AI development as this is really the massive game changer, and I mean, success in this regard in the long term, I think has the potential to make Tesla the most valuable company in the world by far. If you have fully autonomous cars at scale and fully autonomous humanoid robots that are truly useful, it’s not clear what the limit is.”

Analysts’ reaction to Tesla Q3 earnings

Many Wall Street analysts lowered Tesla’s target price following the Q3 earnings report. Goldman Sachs, for instance, lowered its target price by $30 to 4235 and said, “We believe the 3Q report will add to near-to-intermediate term investor concerns given company commentary that the current macro backdrop/higher rates could gate its growth (including how quickly it ramps factories), and comments that the initial Cybertruck ramp could be slow (due to the quantity of new features and technologies Tesla will be using, not due to demand with >1 mn reservations).”

Bernstein analyst Toni Sacconaghi who is among the most bearish on Tesla stock among Wall Street analysts raised a pertinent question “5% auto revenue growth, collapsing margins and trading at 200x FCF — is the story broken?” He added, “In many ways, Tesla is increasingly looking like a regular auto company.”

Jefferies and Wells Fargo also lowered Tesla’s target price to $250 each.

Citi is on the sidelines on Tesla stock

Citi lowered Tesla’s target price to $255 from $271 and prefers to be on the sidelines for now. Analyst Itay Michaeli said in a client note that the sentiments in the US EV market are “decisively negative on the view that Tesla’s price cuts haven’t unlocked significant demand and have made it more difficult for competitors to successfully ramp EVs.”

Michaeli added, “We suspect Tesla’s Q3 results will worsen this sentiment, but we see several unique factors (structural density, regional, product, IRA) that argue for the broader U.S. EV market performing better vs. prevailing sentiment over the next 12-24 months.”

Morgan Stanley analyst and noted Tesla bull Adam Jonas meanwhile maintained his overweight rating on Tesla stock and reiterated that over three-fourths of his Tesla valuation is from the non-auto business which includes energy, insurance, and autonomous driving.

Meanwhile, while the massive drop in Tesla stock had left a hole in investors’ pockets, Musk also lost billions of dollars in his net worth.