Taylor Wimpey Share Price Forecast November 2021 – Time to Buy TW?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

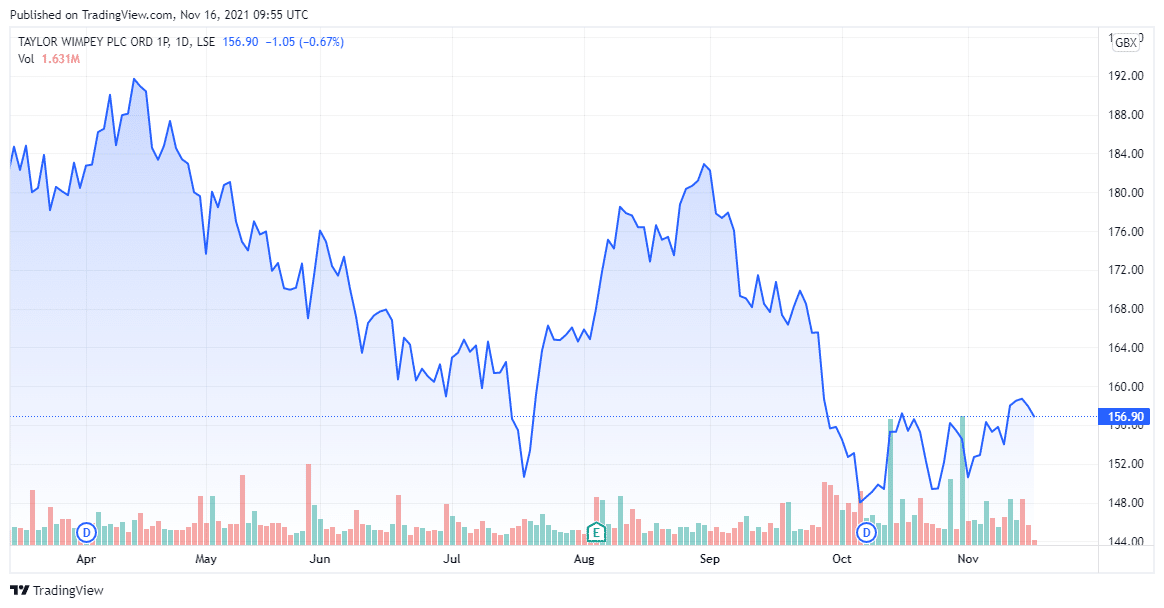

Shares of British-based housebuilding company Taylor Wimpey (LSE: TW) are in the red today, currently trading at 157.55p at the time of writing. Many thought that the company has been in an advantageous position since the UK housing market has exploded in 2021. In reality, the shares have gone nowhere, despite releasing an encouraging trading update recently.

Taylor Wimpey – Technical Analysis

According to the financial statement released by Taylor Wimpey, the market cap of the company is at £5.776 billion with total assets worth £6.158 billion. Revenue for 2020 was at £2.79 billion with a profit margin of 7.78% compared to £4.34 billion in 2019.

Moving averages for Taylor Wimpey such as Exponential Moving Average (10)(156.65), Simple Moving Average (10)(156.49), Exponential Moving Average (20)(155.96), Simple Moving Average (20)(154.65) and Exponential Moving Average (30)(156.49) are pointing towards a buy action. On the flipside, oscillators such as Relative Strength Index (14)(52.87), Stochastic %K (14, 3, 3)(72.85), Commodity Channel Index (20)(78.41), Average Directional Index (14)(14.71) and Awesome Oscillator(3.71) are neutral.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Recent Developments

The biggest news out of Taylor Wimpey is the trading update which the company released some time back, which revealed robust demand from customers. The second half of its financial year saw a sales rate of 0.91 homes per outlet per week. This has risen to 0.95. The company has also added approximately 5500 plots to its short-term landbank during a competitive H2, bringing the total upto 84000. The company continues to target 17,000 to 18,000 competitions per year, supported by a £2.8 billion order book. This translates to an operating margin of 21% to 22% in the medium term.

Management indicated that the company is still on track to meet existing guidance as it is now the UK’s third-largest housebuilder. The increased cost of building homes was offset by the rise in housing prices. The management also expects the situation to improve gradually despite a shortage of materials and drivers across the industry.

The company has underperformed all U.K.-listed peers since March despite the company raising guidance for completion volumes this year. TW had raised 515 million pounds ($704.7 million) in June 2020. This annoyed many investors who thought Taylor’s balance sheet was already strong enough to withstand the pandemic, which was reflected in its share price. The company is set to generate pre-tax profits above pre-pandemic levels by 2022. It has already forward sold 99% of homes which are due for completion this year.

Should You Buy TW Shares?

Investors interested in Taylor Wimpey should look at the dividend rate. While its forecast of 5.4% yield is definitely lower than some of its peers such as Persimmon and Barrat Developments, analysts believe that this will be offset by profits. Profits should be the main concern for investors and they normally prefer receiving small but consistent payouts rather than inconsistent ones. In Taylor Wimpey’s case, market conditions, mortgage availability and government schemes are currently favourable. But there’s no certainty on how long this can last.

Considering the fact that the company’s capital gains haven’t been good, a threat to the dividend rate can be problematic for investors. Compared to where it stood five years ago, TW is only 8% higher. Investors can consider adding TW shares to their portfolio if they remain diversified and hold other FTSE 100 dividend stocks from different sectors. If generating income from your portfolio isn’t a priority for you, there are several other shares that may offer a more balanced combination of capital growth and cash returns compared to TW.

Buy TW at eToro with 0% Commission Now!