Snowflake Stock Price Forecast December 2021 – Time to Buy SNOW Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Snowflake (SNOW) stock was trading sharply higher in US premarket price action today as markets gave a thumbs up to its fiscal third-quarter 2022 earnings.

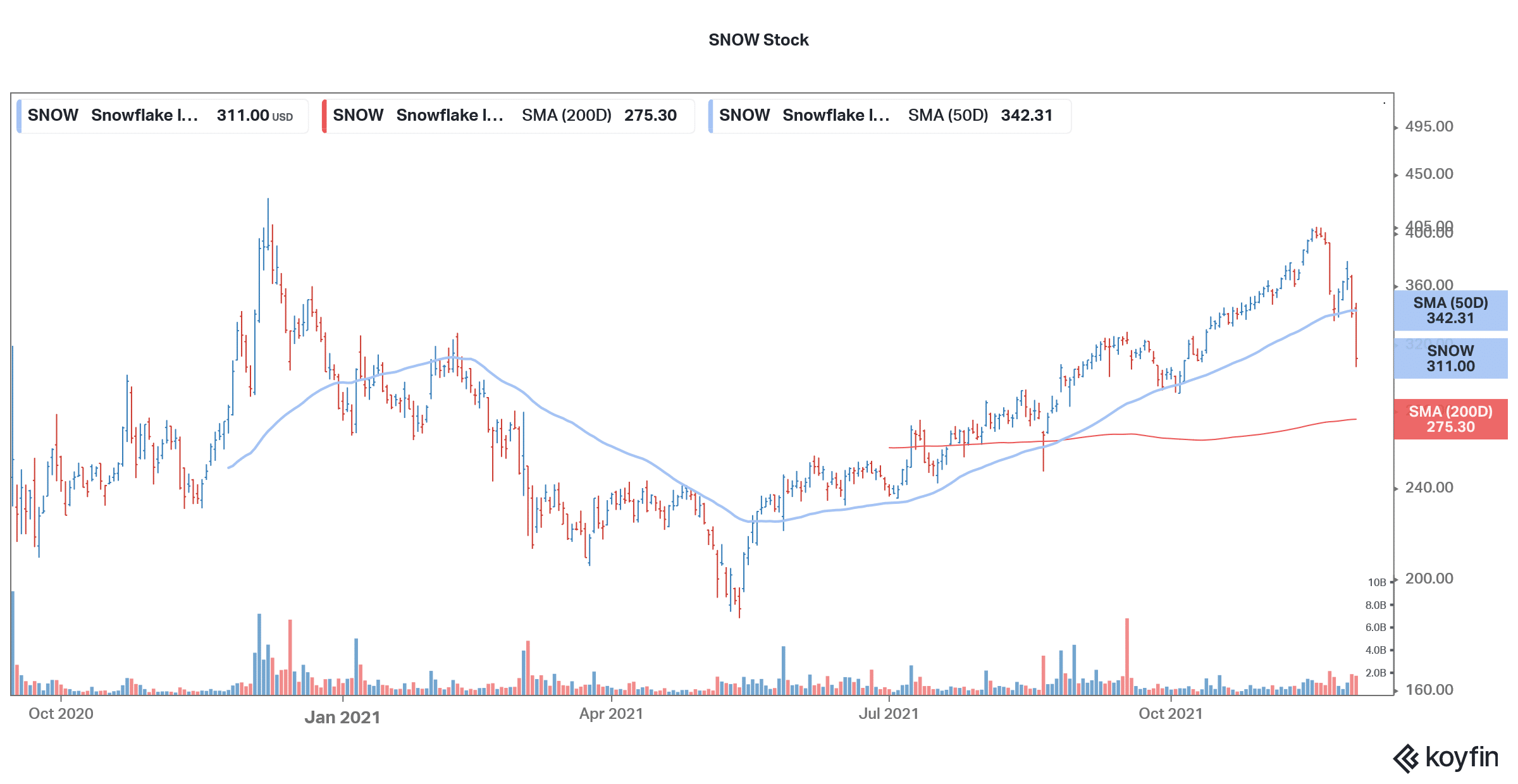

The upwards price action is a welcome break for investors as SNOW stock has otherwise whipsawed this year. The stock is up only about 10% for the year and is underperforming the markets by a wide margin. What’s the forecast for Snowflake stock and is it a good buy in December?

Snowflake reported better than expected earnings

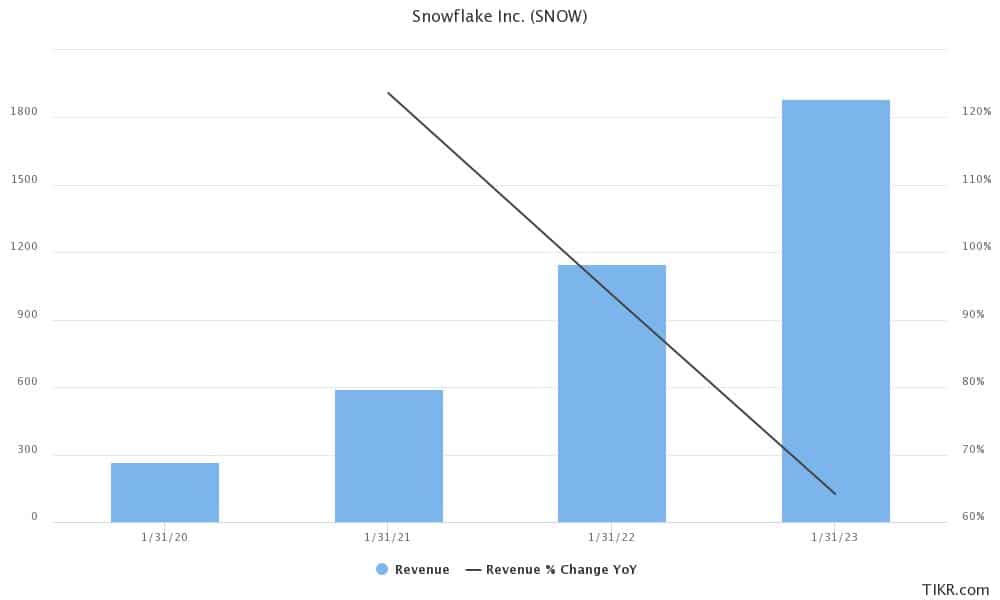

Snowflake reported total revenues of $334.4 million in the quarter ended October which was 110% higher than the corresponding period last year. The revenues were also way ahead of the $305.6 million that analysts were expecting. The company reported product revenues of $312.5 million which were 93% higher than the corresponding quarter last year. The product revenues were also higher than the $280-$285 million that the company had guided for in the previous quarter.

In his prepared remarks Frank Slootman, Chairman and CEO, Snowflake said “Continued international expansion during the quarter resulted in product revenue from the EMEA and APJ regions up 174% and 219% year-on-year, respectively.” He added, “Our vertical industry focus is an important evolution of our selling motion and Snowflake continues to see broad industry adoption.”

68% of all retail investor accounts lose money when trading CFDs with this provider.

SNOW’s loss was less than expected

While Snowflake’s topline growth shattered estimates, its losses were also lower than what analysts were expecting. The company’s net losses per share narrowed to 51 cents, which was half of what it posted in the corresponding quarter last year. Analysts were expecting the company to post a loss per share of 60 cents.

The company has been posting losses, like most other growth companies. However, the management is addressing the profitability issue. In the first-quarter earnings call it said that it has renegotiated with cloud providers and also implemented a change in storage compression. The CFO Mike Scarpelli said that SNOW is working on expanding the margins in the long term and achieving profitability. The third-quarter earnings show that the efforts to address the massive losses are now bearing fruits.

Other key takeaways from Snowflake’s earnings

At the end of October, SNOW had a net revenue retention rate of 173% which looks quite healthy. The company had 5,416 total customers at the end of the quarter. Of these 148 customers had trailing 12-month revenue in excess of $1 million. It had remaining performance obligations of $1.8 billion, a YoY increase of 94%.

The metrics have improved significantly as compared to the fiscal second quarter also. The company had 4,900 customers at the end of the fiscal second quarter with a revenue retention rate of 169%. The remaining performance obligations were $1.5 billion at the end of July and 116 of its customers contributed $1 million or more to its trailing 12 months revenues.

Snowflake’s earnings reveal that the company is adding more customers gradually, including larger ones. The customer stickiness is also good on the platform which would drive long-term value for investors.

SNOW’s guidance was also better than expected

Snowflake’s guidance for the fiscal fourth quarter was also ahead of what analysts were expecting. The company expects to post product revenues between $345-$350 million in the current quarter which was way ahead of the $315.9 million that analysts were expecting. The company expects to post product revenues between $1.126-$1.131 billion in the full fiscal year. This would imply the company’s product revenues almost doubling this year.

Notably, while a lot of growth companies, especially the stay-at-home plays are witnessing a growth slowdown, SNOW continues to witness strong growth.

Snowflake stock price forecast

Snowflake’s median target price of $360 is a premium of 16.9% over current prices. Its lowest target price of $275 is a discount of 11.5% while the highest target price of $575 represents a potential upside of over 85% over the next 12 months. Wall Street analysts meanwhile have a mixed forecast on the stock. Of the 30 analysts polled by CNN Business, 15 have rated SNOW as a buy while 15 analysts have given it a hold rating. None of the analyst has a sell or equivalent rating on the stock.

Last month, Credit Suisse initiated coverage on SNOW stock with an outperform rating and $455 target price. BTIG Research also boosted its target price on the stock. However, Rosenblatt Securities downgraded the stock from a buy to neutral.

SNOW stock long term forecast

Credit Suisse analyst Phil Winslow believes that Snowflake stock is a long-term winner and would continue to grow at a higher pace. Snowflake expects to post product revenues of $10 billion by the fiscal year 2029 which would be similar to the calendar year 2028. This would mean a revenue growth CAGR of almost 44%. The company’s product revenues are set to exceed $1 billion in the current fiscal year only.

Should you buy Snowflake stock?

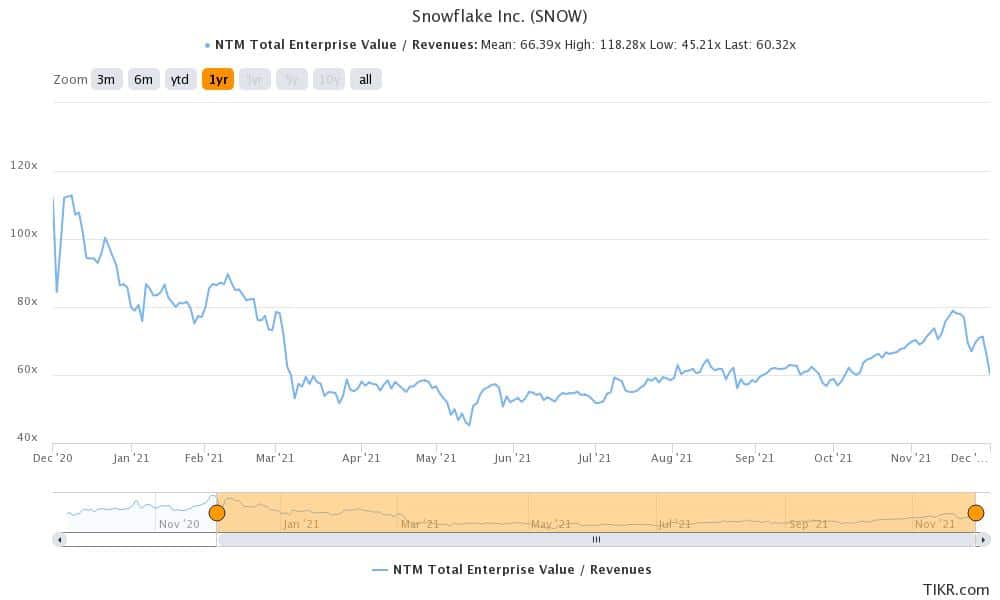

Growth hasn’t been much of a concern for SNOW investors. However, a section of the market has been apprehensive of its valuations. The stock trades at an NTM (next-12 months) EV-to-sales multiple of 60x. The valuations look high on an absolute level. However, they look reasonable when looked at in the context of its high growth.

SNOW stock is trading above its 200-day SMA (simple moving average). It looks set to move above its 50-day SMA also looking at the premarket price action.

Incidentally, Snowflake was the rare IPO that Berkshire Hathaway bought. The conglomerate continues to hold the stock since then. While it was likely a different investment manager and not Warren Buffett who made the investment, it is nonetheless a stamp of approval for the company’s prospects.

SNOW looks among the best ways to play the cloud industry which is among those sectors that are expected to witness strong secular growth over the next decade.

Buy SNOW Stock at eToro from just $50 Now!