Snowflake Stock Price Down 22% Today – Time to Buy SNOW Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Snowflake (SNOW) stock is trading sharply lower in US premarket price action today after releasing its fiscal fourth-quarter 2022 earnings. We’ve seen a lot of volatility in tech stocks this earnings season.

Prior to the fall today, SNOW stock was down almost 22% for the year and is underperforming the markets by a wide margin. While it has rebounded from its all-time lows, it is still way below the all-time highs. What’s the forecast for Snowflake stock and should you buy the dip in the cloud company?

Snowflake stock recent developments

Snowflake reported its fiscal fourth-quarter 2022 earnings for the three-month period ending in January yesterday after the close of US markets. It reported total revenues of $383.8 million in the quarter, which was 101% higher than the corresponding quarter in the previous year. The company reported product revenues of $359.6 million in the quarter, a YoY rise of 102%.

The company’s revenues were higher than what analysts were expecting and were also better than its guidance. During the previous earnings call, SNOW had said that it expects to post product revenues between $345-$350 million in the fiscal fourth quarter. The company’s guidance was way ahead of the $315.9 million that analysts were expecting. Meanwhile, the revenue beat over the guidance was quite small as compared to what we’ve seen in the last few quarters.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Key metrics from Snowflake earnings

Snowflake has been working to address perennial losses and they have been gradually coming down. In the fourth quarter, it posted a net loss of $132 million which was below the $199 million in the corresponding quarter in the previous fiscal year. It reported adjusted gross margins of 70% in the quarter, which were slightly below the consensus estimate of 70.9%.

The company had 5,944 total customers at the end of the quarter and 184 of these had an annual product revenue of over $1 million. To put that in perspective, it had 5,416 customers at the end of the previous fiscal quarter and 148 of these had annual product revenues in excess of $1 million. During the quarter, it reported a net revenue retention rate of 178% which was higher than the 173% it reported in the previous quarter. Also, it had remaining performance obligations of $2.6 billion, which was 99% higher than the corresponding quarter last year.

SNOW guidance

More than the earnings, the fall in SNOW stock has to do with the guidance. In the fiscal first quarter of the current year, the company expects to post product revenues between $383-$388 million, which would mean a YoY growth between 79-81%. In the full fiscal year, it expects its product revenues to rise between 65-67%. While the guidance was slightly ahead of estimates, markets are concerned over the slowing growth.

Ahead of the earnings, analysts were expecting SNOW to report higher guidance than the consensus estimates. JP Morgan analysts said ahead of the release that “Given a strong demand environment, we believe Snowflake’s FY23 outlook can land well above consensus, as some of its recent product innovations and investments see wider penetration.”

Stifel had said, “We expect management to follow historical patterns and guide conservatively on both the top and bottom line, but we do expect the current FY23/24 revenue estimates to move higher post the print.” While SNOW said that it was being conservative with the guidance, markets are not too pleased with the projections.

Several companies have disappointed this earnings season

Companies as diverse as Affirm, Snowflake, Facebook, and Netflix have plummeted after providing tepid guidance. Amid the rising US interest rates, a worse than expected growth slowdown is the last thing that investors want. No wonder, companies that reported lower than expected guidance have plummeted after the release.

Snowflake IPO

Snowflake went public in 2020 and was the biggest software IPO ever. It raised the IPO price range multiple times and eventually priced it at $120 per share. The stock doubled on listing leading to massive gains for investors. Incidentally, Snowflake was the rare IPO that Berkshire Hathaway bought. The conglomerate continues to hold the stock since then. While it was likely a different investment manager and not Warren Buffett who made the investment, it is nonetheless a stamp of approval for the company’s prospects. Salesforce had also co-invested in SNOW’s IPO.

Snowflake stock forecast

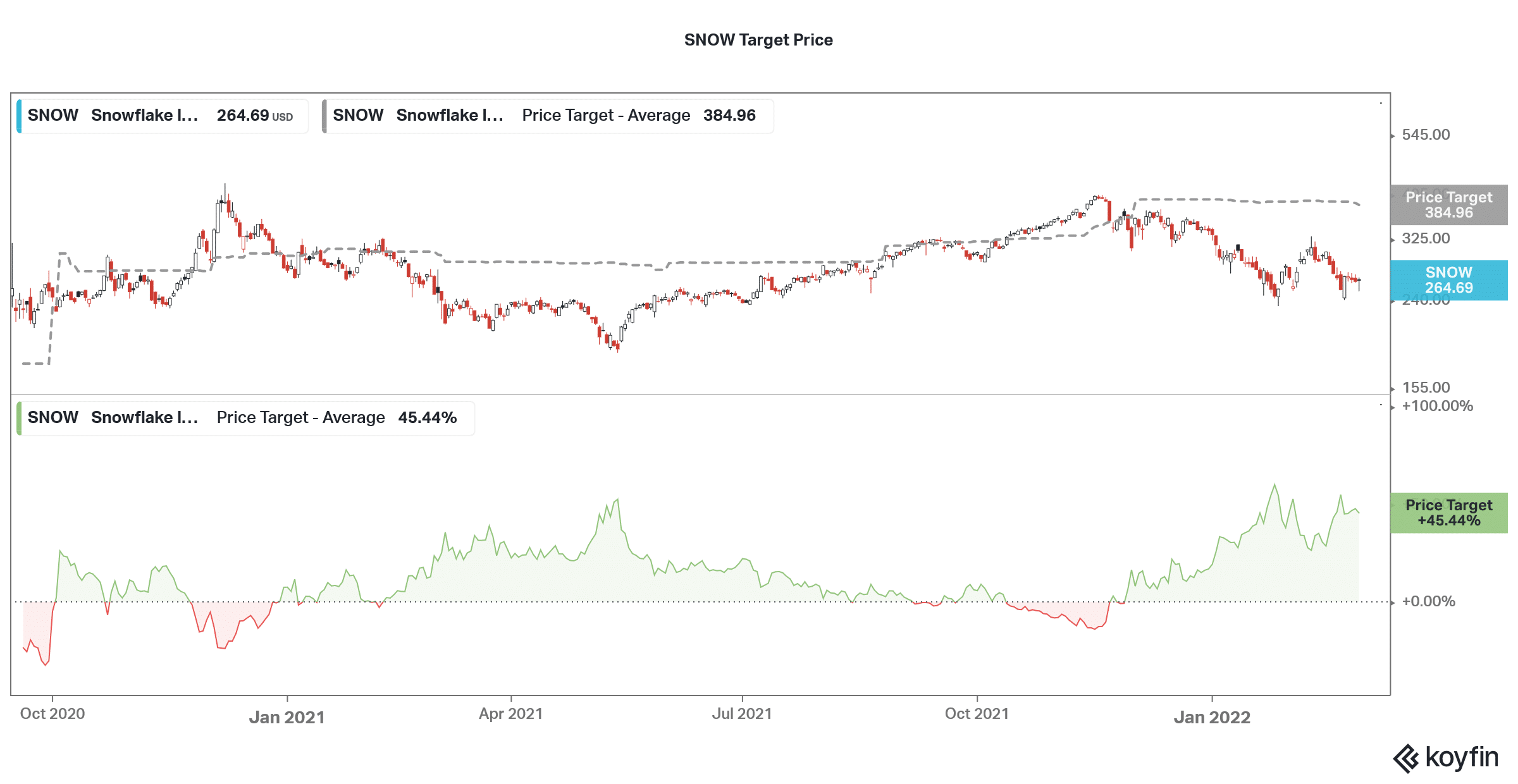

Wall Street analysts have a consensus buy rating on Snowflake stock. Of the 29 analysts covering SNOW, 19 have a buy rating while ten have a hold rating. None of the analysts have a sell rating on the stock. Its median target price of $387.50 is a premium of 45.7% over current prices. The street high target price of $575 is a 116% premium while the street low target price of $290 is also 9% above current prices.

SNOW stock long term forecast

Snowflake expects to post product revenues of $10 billion by the fiscal year 2029 which would be similar to the calendar year 2028. This would mean a revenue growth CAGR of almost 44%. In the last fiscal year, its revenues surpassed $1 billion. SNOW remains a play on the cloud transition.

Should you buy SNOW stock?

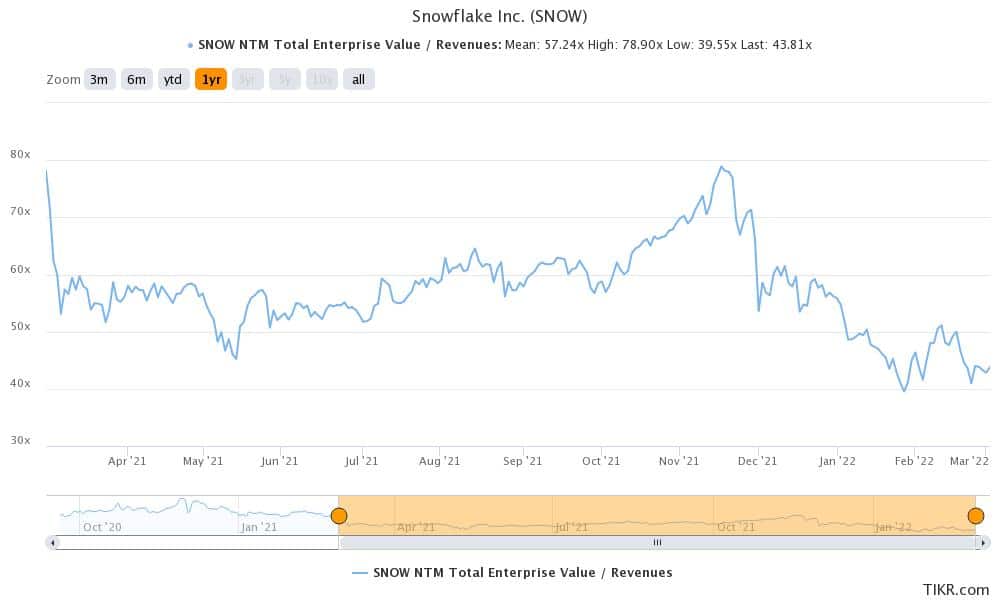

Based on the traditional valuation metrics, Snowflake has always been among the most richly valued stocks. Despite the recent crash, it trades at an NTM EV-to-sales multiple of 43.8x. Loss-making richly valued tech companies have been under tremendous pressure and SNOW is no exception. However, it remains a good way to play the cloud industry, which is among those industries that should see secular growth.

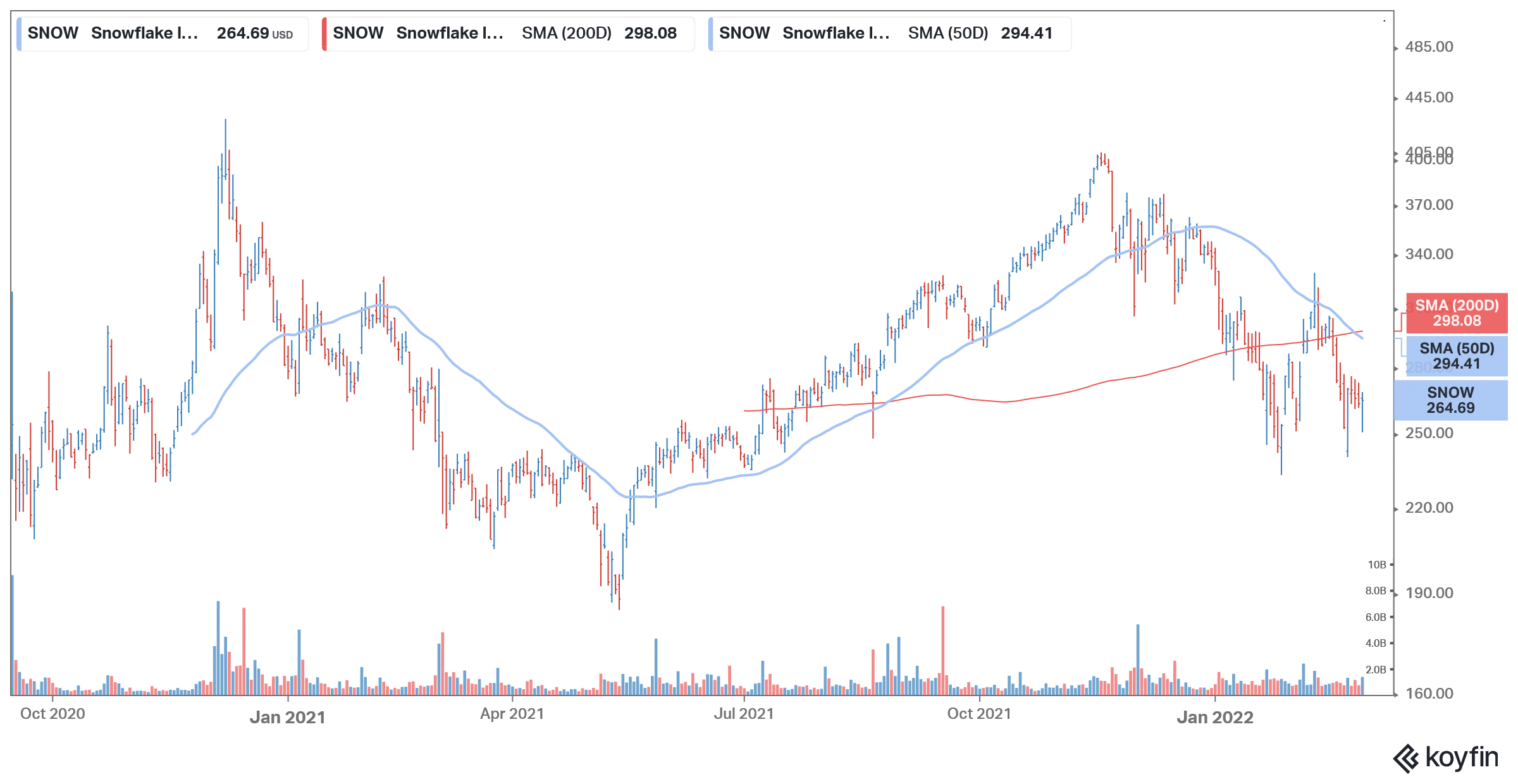

However, it looks weak in the short-term considering the sell-off in growth names, which might not yet be over. The stock is looking bearish on the charts as well and there has been a death cross formation where SNOW’s 50-day SMA fell below the 200-day SMA. While the death cross is a lagging indicator, it nonetheless signals a prolonged bear market in a stock.

Buy SNOW Stock at eToro from just $50 Now!