Royal Mail Shares Forecast and Price Prediction June 2021 – Is Royal Mail a Good Stock to Buy?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

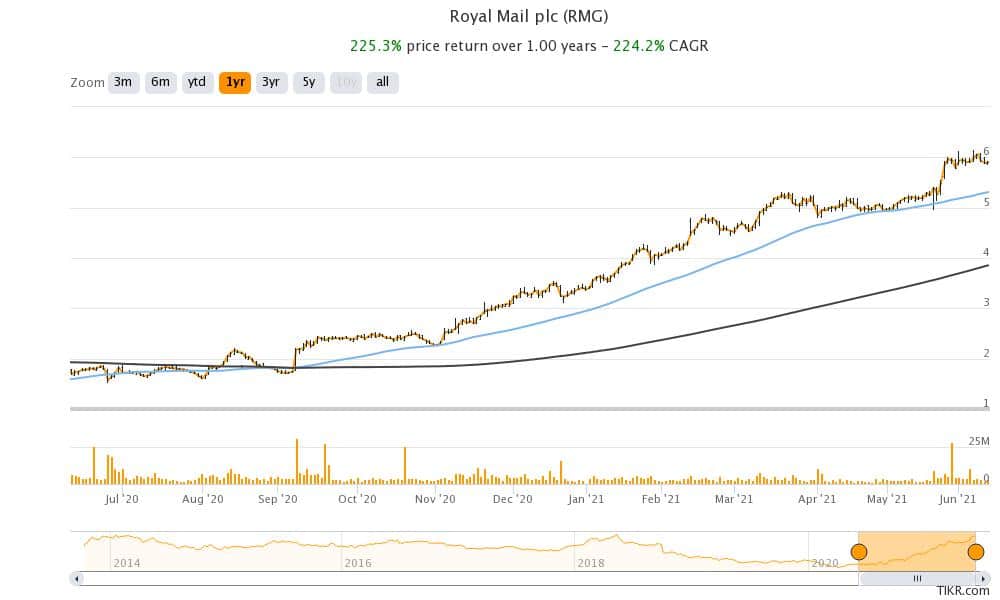

Royal Mail shares have gained almost 75% so far in 2021 and are outperforming the markets by a wide margin. What’s the forecast for the share in June 2021 and should you buy it now?

Royal Mail shares are trading near their 52-week high price of £6.13 and have risen almost four-fold from their 52-week low price of £1.5. This year, we’ve seen a rally in some of the beaten-down shares even as investors have been wary of high-growth tech names.

Royal Mail technical analysis

Royal Mail shares are looking bullish on the charts. The share is trading above the key moving averages including the 50-day SMA (simple moving average), 100-day SMA, and 200-day SMA. Over the last year, the shares have found a strong support near the 50-day SMA which is currently at £5.31. However, after the recent rally, the shares seem to be getting near the overbought territory. Its 14-day RSI (relative strength index) is currently at 63.5 which is not far away from the 70 level above which shares are seen as overbought.

Recent developments

Last month, Royal Mail released its earnings for the fiscal year ended 28 March 2021. Its revenues increased 16.6% in the year while its basic EPS rose from 16.1p to 62.0p over the period. The performance was better than what the company had guided. Like many other companies, it did not provide quantitative guidance as a “number of uncertainties that could significantly influence volumes and costs.”

Royal Mail shares have an attractive dividend yield

The company declared a final dividend of 10p for the last fiscal year and talked about a progressive dividend policy setting the dividend for the fiscal year 2021-2022 at 20p per share. This means a forward dividend yield of almost 3.4% which is over twice of S&P 500’s current dividend yield. Incidentally, the S&P 500 dividend yield is currently way lower than its historical averages as several components slashed their dividends in 2020. Also, the inclusion of non-dividend paying Tesla negatively impacted the S&P 500’s dividend yield.

If you are looking for a good dividend-paying share, Royal Mail will fit the bill with an attractive dividend yield. However, along with the dividends, we also need to look at the potential for capital appreciation which in most cases accounts for the bulk of returns from shares.

Royal Mail share forecast

Royal Mail shares have a median target price of £5.95 which is similar to its current share price. The highest target price of £10 is a premium of 68% while the lowest target price of £2.84 is a discount of almost 52%. Of the 15 analysts covering the shares, 10 have rated it as a buy or some equivalent while the remaining five rate it as a hold.

Analysts are getting bullish

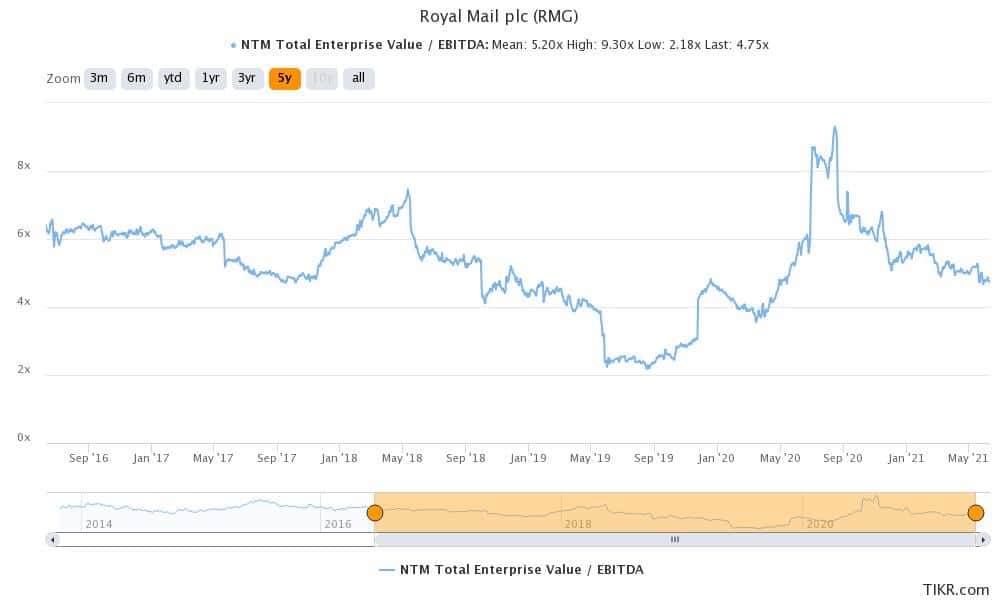

Citi is the most bullish brokerage on the shares and added it to its Europe “focus list.” The brokerage had backed Royal Mail shares in 2020 also after the shares had tumbled amid the COVID-19 uncertainty. The bullishness has played out well and the shares are up sharply since Cito’s upgrade. “We upgraded the stock in April 2020 on the hoped-for acceleration in parcel volumes and in November we argued for the potential for a pricing increase in parcels,” said Citi analysts in their note. Citi values Royal Mail shares at 7x its EV-EBITDA (enterprise value-earnings before interest, tax, depreciation, and amortization).

In May, JP Morgan also raised the target price for Royal Mail shares from £6.85 to £8.01. It had expressed its surprise over markets not reacting positively to its bumper fiscal 2021 earnings.

Royal Mail shares look undervalued

Royal Mail shares currently trade at an NTM EV-EBITDA multiple of 4.75x. The multiple has averaged 6.06x over the last year and 5.2x over the last five years. The current multiples are lower than what the shares have traded historically. Also, given the strong growth in demand from the e-commerce sector, the shares can trade at a higher multiple than it is currently trading at.

Parcels accounted for 72% of its last year revenues. It was the first time in the company’s five-decade history when revenues from parcels exceeded that from letters. In the last fiscal year, GLS revenues increased 27.8% which was over twice what Royal Mail revenues increased. The company expects GLS revenues to increase at a CAGR of 12% between the fiscal year 2019-20 to the fiscal year 2024-2025. Over the period, it expects the business’s operating profits to more than double to €500 million.

Royal Mail has a strong balance sheet and had a debt of only £457 million at the end of the previous fiscal year, down sharply from £1.1 billion at the end of the fiscal year 2019-2020.

Overall, Royal Mail shares look attractively priced and a good buy at these prices.

Looking to buy Royal Mail shares now? Invest at eToro!

75% of all retail investor accounts lose money when trading CFDs with this provider.