PING Stock Price is Down 3.5% – Time to Buy PING Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Ping Identity Holding (PING) shares is down 3.5% since last week after the company priced a share offering from existing shareholders for around $144 million at $24 per share on 15 June, with the news causing a sharp 8% single-day drop.

Ping Identity, a company that provides access protection solutions for multiple clients including cloud providers and software-as-a-service (SaaS) companies have had quite a bad year following a disappointing Q4 2020 earnings report as sales came 8% below analysts’ estimates for the period – a situation that has plunged the stock price as much as 17.6% in 2021.

Could this be an opportunity to buy a company whose services are becoming increasingly important in a world where cybersecurity threats are getting scarier? Join me in the following article as I take a closer look at PING’s fundamentals to see if this latest drop resulting from the company’s share offering could be providing a buying opportunity for long-term investors.

Buy PING stock at eToro, the World’s #1 trading platform!

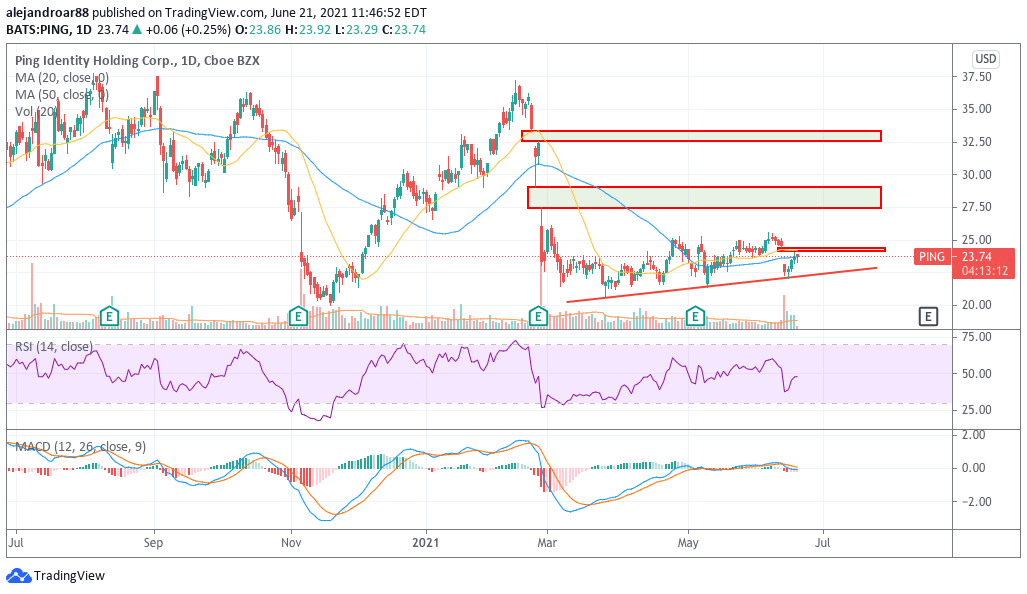

PING stock – technical analysis

The chart above shows the extent of the negative momentum that the stock has been seeing lately, with two major bearish price gaps left behind as a result of the company’s disappointing results back in the fourth quarter of 2020.

Even though the stock has been staging a slow comeback on the back of a series of higher lows, the path to recover that lost territory seems quite challenging.

For now, the stock price is on an uptrend. However, the bearish price gap left behind after yesterday’s share offering announcement might present an obstacle for the price to continue its advance.

If bulls manage to reclaim the $25 level, chances are that PING could soon tag the lower end of the February price gap at $27.5 for a near-term upside potential of 10%. However, if market participants reject a move above the $25 area, the odds would be in favor of a bearish outlook, with the first area of support found at around $22 for an 8% downside risk.

PING stock – fundamental analysis

Ping Identity (PING) is a Denver-based cybersecurity solutions company that provides multiple different ID verification services to banks, health care, and aerospace companies – among others – that are seeking to protect their systems from being accessed by unauthorized third parties.

The company went public in 2018 and has failed to deliver any meaningful jumps in its top-line results, as PING’s 2020 sales landed at $244 million or $1 million higher than the year before.

Meanwhile, the company provided revenue guidance of $265 million for its 2021 fiscal year, resulting in an 8.6% advance compared to last year’s sales. This guidance came slightly below the market’s forecast for the period, which means that PING is struggling to grow its sales at the pace that the market would expect for a company in such a promising sector.

Moreover, gross margins for PING have been deteriorating progressively since the fourth quarter of 2018 at least, moving down from 86.1% back then to 78.2% by the end of the first quarter of 2021.

Moreover, the company has swung to negative EBITDA since the fourth quarter of 2020 as operating expenditures have increased significantly from $50.2 million back in the first quarter of 2020 to $66 million during the same period this year as a result of higher stock-based compensation expenses.

This has resulted in the company reporting higher losses per share of $0.20 during the first quarter of 2021 compared to $0.05 during the same period a year ago.

The deterioration of the firm’s profit margins along with slower-than-expected revenue growth seems to be have been the catalyst for the most recent sharp decline in the stock price, with the stock displaying an accumulated loss of 34.4% since its post-pandemic peak of $36.25 per share seen in February this year.

From the perspective of solvency, PING’s net debt currently stands near zero while the company’s assets, excluding cash, stand at $820 million including $616 million in goodwill and intangible assets.

At the moment, PING’s market capitalization stands at $1.95 billion, which results in a forward price-to-sales ratio of 7.4 based on the company’s forecasted sales for 2021 while PING is not showing signs that it might be able to turn a profit any time soon.

Based on the firm’s stalled growth and unimpressive prospects, this stock seems heavily overvalued. Moreover, the weight that intangible assets have on its balance sheet makes the company’s share price highly sensitive to the impact of impairments.

Buy PING stock at eToro, the World’s #1 trading platform!