PepsiCo Stock Price Forecast October 2021 – Time to Buy PEP Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

PepsiCo (PEP) stock rose 0.6% yesterday which took its YTD gains to 4.7%. Meanwhile, while the stock is underperforming the S&P 500 by a wide margin this year, it is outperforming rival Coca-Cola.

What’s the forecast for PepsiCo stock in October 2021 and should you buy this beaten-down beverage and snacks company?

PepsiCo stock technical analysis

PEP stock is not looking too bullish on the charts. It has been facing strong resistance at the 50-day SMA (simple moving average). The stock also trades 100-day SMA as well as short-term moving averages like the 10-day, 20-day, and 30-day SMA. PEP meanwhile trades above the 200-day SMA which is currently at $146.12 and would be a strong support if the stock were to fall from these levels.

The MACD (moving average convergence divergence) gives a sell signal for PEP stock. While its 14-day RSI (relative strength index) is 39.5 and is a neutral indicator, it is getting near the oversold zone. RSI values below 30 signal oversold positions.

67% of all retail investor accounts lose money when trading CFDs with this provider

PepsiCo stock recent developments

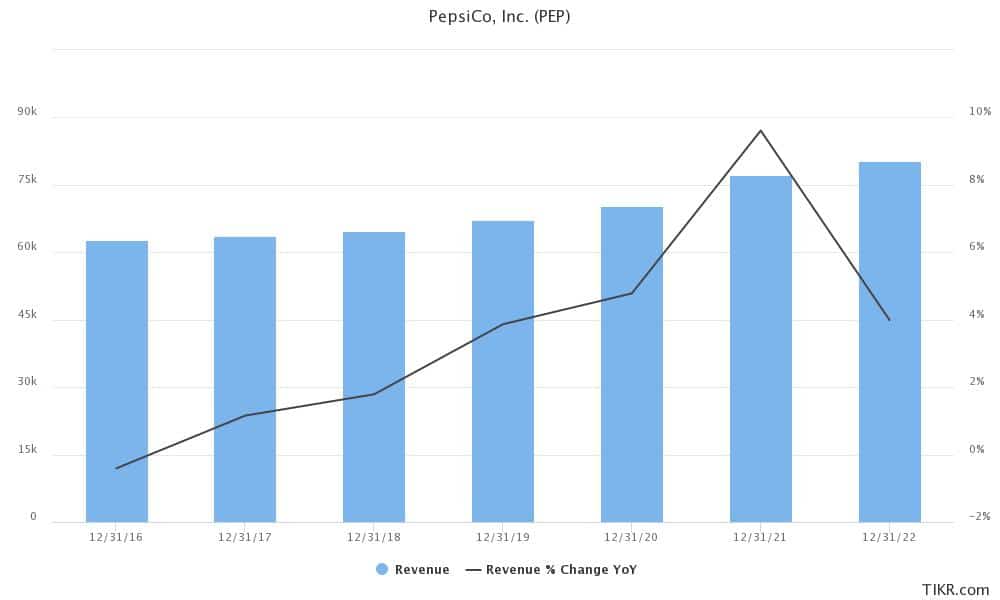

PepsiCo released its fiscal third-quarter earnings yesterday. The company’s revenues came in at $20.19 billion in the quarter which was ahead of the $19.39 billion that analysts were expecting. The company’s net revenue growth was 11.6% in the quarter which includes a 2% impact from currency movement. Its organic revenue growth in the quarter, which is a more prudent metric, rose 9%. In the first nine months of the fiscal year, organic sales increased 8.4%.

PEP reported an earnings beat

5% revenue growth in the fiscal third quarter came from selling higher-priced products. Notably, the company has had to increase prices amid cost escalation. Also, companies have been battling with supply chain problems amid the shortage of labor especially truck drivers. While PepsiCo’s CFO Hugh Johnston said that he expects the supply chain pressures to ease by the end of this year, he said that the company might to increase prices further.

“I do expect there will probably be some price increases in the first quarter of next year as well, as we fully absorb and lock down the impact of commodity inflation,” said Johnston. Meanwhile, the company also raised its full fiscal year revenue growth guidance to 8% from 6% after a strong performance in the quarter.

PepsiCo earnings

Looking at the breakup of different segments, Quaker Foods North America reported a 4% fall in volumes even as the segment’s revenues increased 1% on higher pricing. Frito-Lay volumes in North America increased only about 1% while the company’s beverage sales in the region increased about 3%. According to PepsiCo, it managed to increase its market share in salty and savory snacks in the fiscal third quarter.

The company’s volume growth in North America was softer as compared to some of the other regions. Meanwhile, the outdoor beverage business has been the most challenging for beverage companies like Coca-Cola and PepsiCo as there is still a restriction on outdoor activities like sports. However, now the company’s outdoor beverage sales are only about 10% lower than the 2019 levels.

As more people get inoculated and more outdoor restrictions are eased, the away-from-home beverage sales might also pick up.

PepsiCo stock price forecast

After the recent underperformance, the forecast for PEP stock looks positive. The stock has received 12 buys, 10 holds, and one sell ratings. Its median target price is $167 which implies an upside of 10.5%. The street high target price of $185 is a premium of 22.5% over current prices.

Interestingly, there hasn’t been any major analyst action after the company’s fiscal third-quarter earnings. That said, a section of the market has been apprehensive about PepsiCo’s valuation and in July Credit Suisse had downgraded the stock as the brokerage wasn’t comfortable with the valuations.

PEP target price

However, UBS upgraded the stock to buy earlier this year while raising the target price to $165. “We consider PEP’s valuation … to offer favorable entry point given PEP’s positioning as a beneficiary of continued at-home consumption momentum and on-premise reopening. PEP is a story of consistency and proven execution with category and geographical diversification,” said UBS.

Notably, PepsiCo has been investing in the brand which would lead to long-term value creation. “We believe PEP is only at the midpoint of an investment cycle that will yield a sustainable improvement to top and bottom line growth,” added UBS analysts in their note.

PEP stock long term forecast

In a response to an analyst question on the company’s long-term growth outlook after the high growth in the preceding some quarters, PepsiCo did not provide a definitive answer. However, it said that the growth in 2022 would be in line with the long-term forecasts. The company also expects supply chain pressures to ease next year. Wall Street analysts expect the company’s revenues to rise 4% next year. However, analysts might revise the estimates once PepsiCo provides the guidance during the next earnings call.

While the demand for carbonated beverages is expected to come down over the long term, PepsiCo’s pivot towards healthier beverages and snacks would help offset the impact

Should you buy PEP stock?

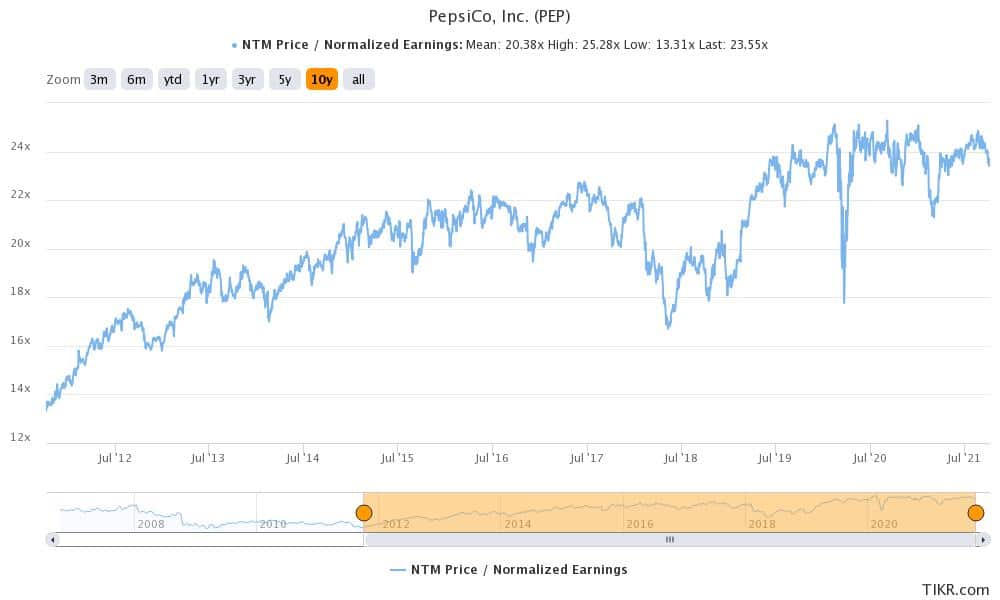

PEP stock trades at an NTM (next-12 months) PE of 23.5x. Now, while the multiples are higher than the ten-year average of 20.4x, the stock doesn’t appear overvalued at these prices. Also, if you are looking for a defensive stock, PepsiCo would fit the bill with its dividend yield of 2.85%. While PEP might not be a multibagger like some of the growth names, the stock would appear attractive if you are a conservative investor.

Buy PEP Stock at eToro from just $50 Now!