Peloton Stock Price Fell 78% Last Year– Time to Buy PTON Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

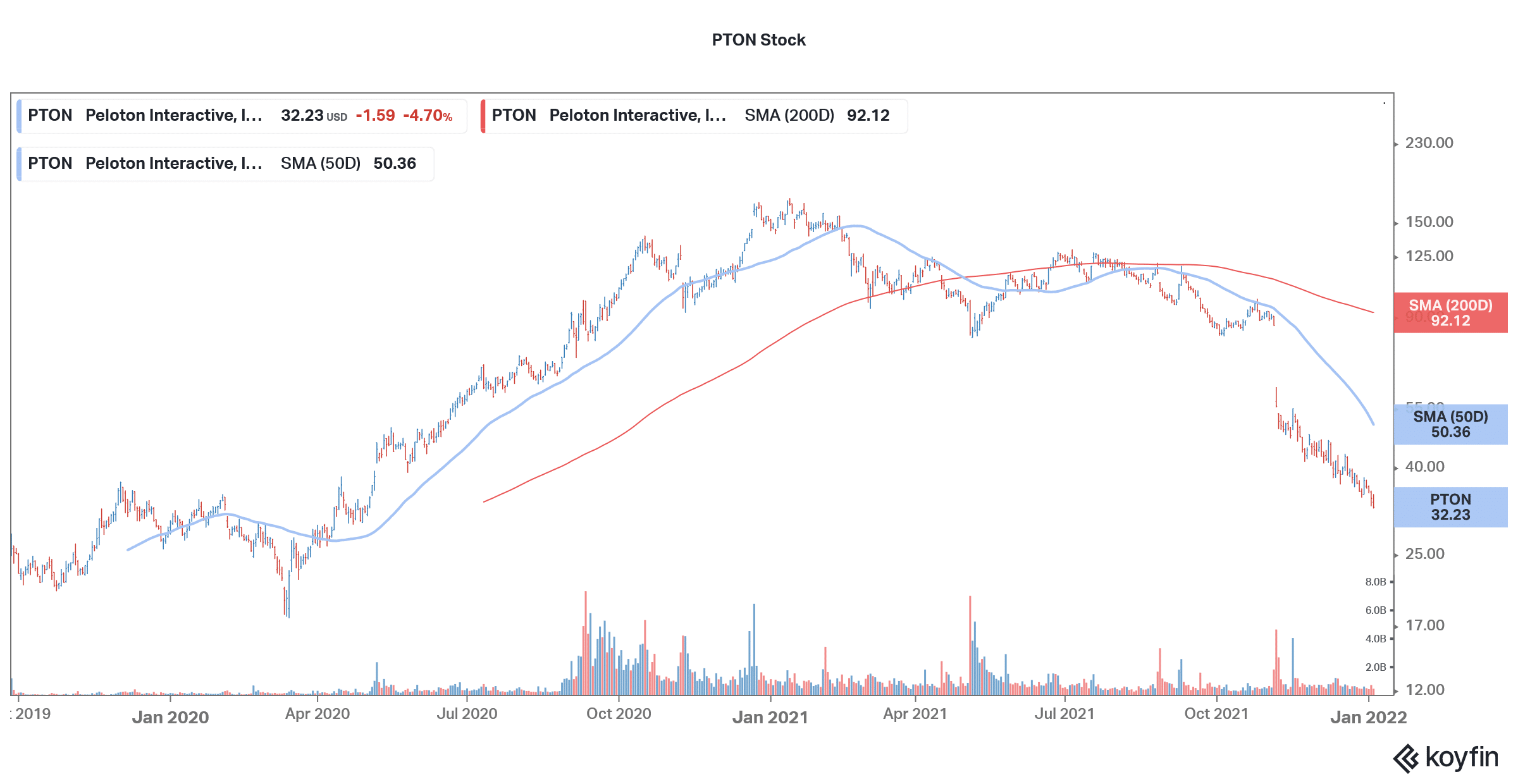

For stay-at-home companies, 2021 was a mirror opposite of 2020. While these stocks rallied sharply in 2020 amid changed consumer behavior, they came under pressure in 2021 as consumer behavior reverted towards pre-pandemic times. Peloton (NYSE: PTON) stock is now down 78% over the last year and is among the worst-performing stay-at-home stock.

2022 is not looking any good for PTON stock and it has hit a new 52-week low of $32 in the very first trading week of the year. The stock is now trading close to what it did before the pandemic and has pared all the gains of 2020. The stock is now down 81% from its 52-week highs. Beachbody, which went public through a SPAC reverse merger last year, and expected to capitalize on the strong demand for stay-at-home health equipment companies, is also trading at a fraction of its highs. What’s the forecast for Peloton stock and could it rebound in 2022?

The Fed’s rate hikes are negative for growth stocks

The rally in growth names was punctured in the first quarter of 2021 amid the rise in bond yields. Markets expected the Fed to raise rates to tame inflation even as the US central banks kept on describing the price rise as “transitory.” Now, the Fed no longer harps on the term and would end the bond-buying in this quarter itself. The minutes of the Fed’s December meeting were hawkish than expected. While markets are prepared for rate hikes in 2022 and brokerages have quite tepid expectations from the US stocks in the year, a faster than expected tightening could have been the worst thing, especially at a time when the omicron variant cases are surging across the country.

The rate hikes are especially negative for growth names that have their earnings skewed towards the future. Future cash flows get discounted at higher rates thereby reducing their present value and by extension the fair value of the stock.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Peloton is facing multiple troubles

But then, rate hikes are not the only trouble that Peloton is facing. In what looked damaging for Peloton’s brand, a fictional character in Sex and the City died while using Peloton equipment. There couldn’t be any further negative publicity for the company whose equipment was involved in a fatal accident. While initially, the company’s response to the accidents wasn’t up to the mark, it went for product recall.

Meanwhile, Peloton hasn’t taken too kindly to the portrayal of its equipment and has hit back with a counter advertisement narrated by Ryan Reynolds. “And just like that… the world is reminded that regular cycling stimulates and improves your heart, lungs and circulation, reducing your risk of cardiovascular diseases. Cycling strengthens your heart muscles, resting pulse and reduces blood-fat levels,” said the ad.

PTON is facing a growth slowdown

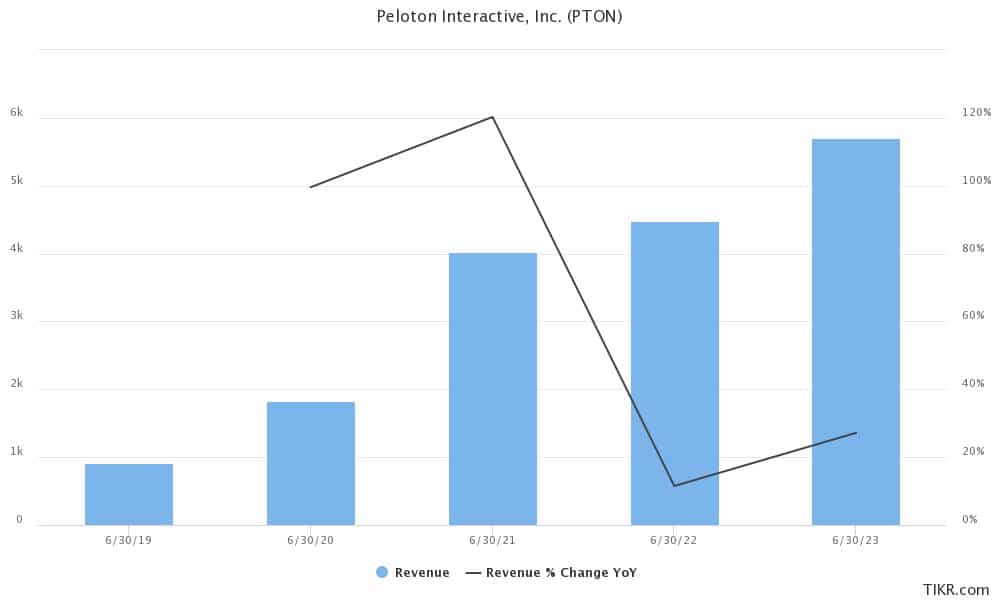

Peloton also lowered its guidance for the fiscal year during the earnings call in November. It said that its revenues would be between $4.4-$4.8 billion in the full fiscal year, which was way above the previous guidance of $5.4 billion. The company expects to post gross margins of 32% in the year. PTON expects to have between 3.35-3.45 million connected subscribers by the end of the year. It, however, expects to post an EBITDA loss between $425-$475 million in the year.

While the company lowered the guidance, some of the Wall Street analysts even find the toned-down guidance too high. JPMorgan analyst Doug Anmuth lowered PTON’s target price from $70 to $50. He expects the company to post revenues of $4.2 billion in the fiscal year, which is even below the company’s low end of the guidance. Anmuth also lowered the projected subscriber numbers and expects it to report 2.79 million connected subscribers in the fiscal second quarter, which is below the company’s estimates.

Analysts have pointed to slowing search for Peloton on the web and lower footfalls on the website and app for lowering their target prices. Also, some have also pointed to the slowing growth of social media followers of Peloton instructors.

Analysts slash PTON’s target price

Raymond James analyst Aaron Kessler expects Peloton to slash its guidance for the full year yet again when it reports the fiscal second-quarter earnings. “When Peloton provided guidance, we believe the company was assuming a return to stronger seasonality in the December quarter following the slower summer seasonality,” said Kessler.

He has a base case target price of $38 on the stock. His bear case and best-case target price are $27 and $51 respectively. Baird analyst Jonathan Komp also recently lowered his price target to $70 from $90.

Peloton stock forecast

Wall Street analysts have a split rating on PTON stock and 10 of the 27 analysts covering the stock rate it as a buy. 15 analysts have a hold rating while the remaining two rate it as a sell. The stock’s median target price of $69.96 is a 106% premium over current prices. The street high target price of $110 while $30 is its street low target price. Since the company’s earnings, analysts have been slashing their target price and the current consensus target price is almost half of what it was prior to the earnings.

PTON stock long term forecast

The long-term outlook for home fitness equipment companies like Peloton looks positive. While the growth rates of 2020 might not be sustainable, the industry should see secular growth over the long term. PTON is also building a factory in the US to support the demand.

From the home fitness market, Peloton is now also diversifying into the commercial market. Earlier this year, it had acquired Precor and is now integrating the two businesses to target the hospitality sector. International expansion would also drive value for Peloton.

We could see a hybrid model in workouts also and both gyms and home equipment companies can flourish. However, in the near term, slowing growth and rising rates might continue to take a toll on Peloton stock.

Should you buy Peloton stock?

Peloton stock looks like a high-risk buy. If the company can convince markets that its long-term growth outlook is intact, it could see better days.

Buy PTON Stock at eToro from just $50 Now!