Peloton Stock Price Down 16% in 2022 – Time to Buy PTON Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

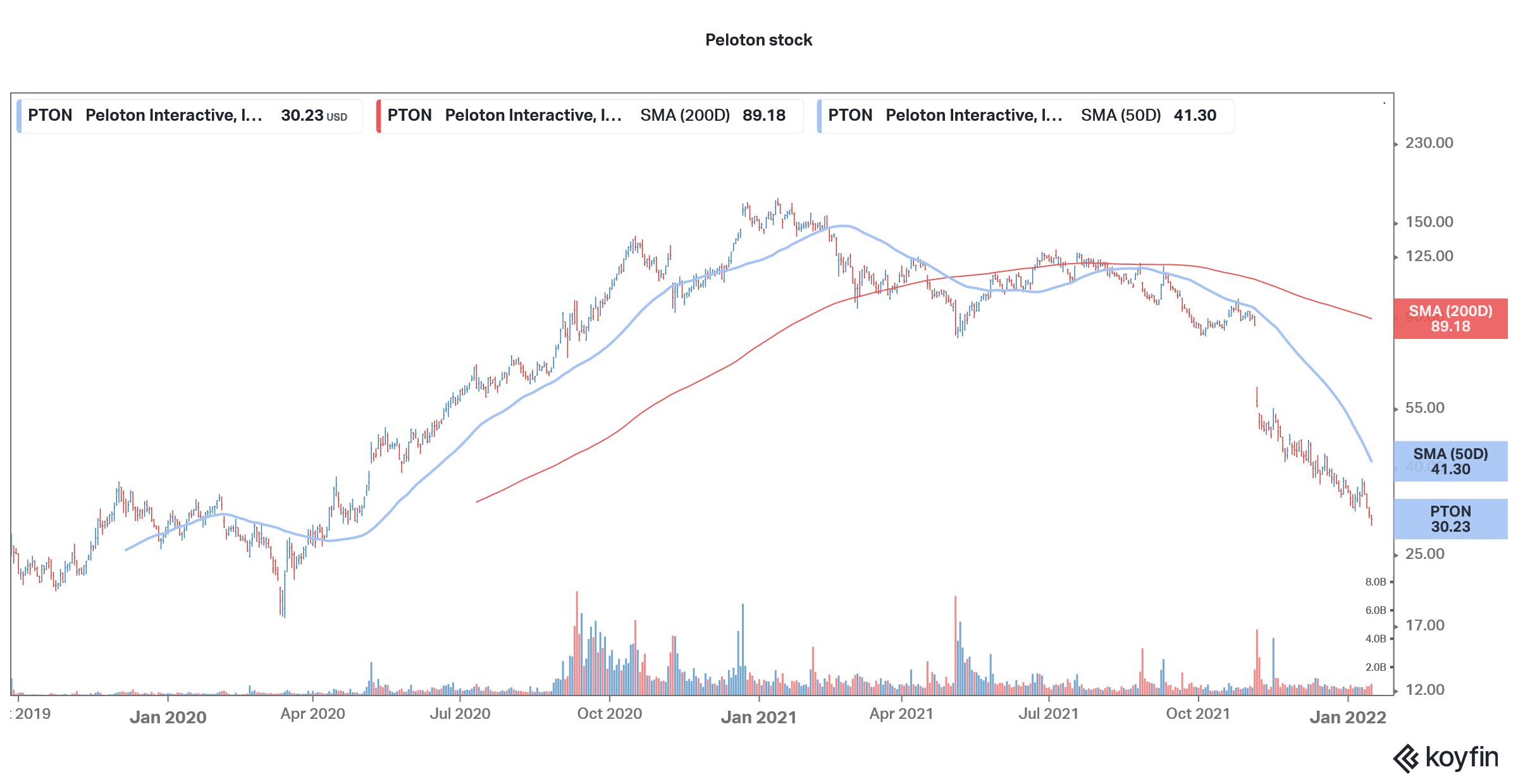

Peloton (NYSE: PTON) stock fell 3.5% yesterday and hit a 52-week low of $29.11 intraday. The stock is now down 15.5% in 2022 and has continued its dismal run from the last year.

In 2021, PTON stock fell 76% and was the worst-performing Nasdaq stock. While the entire stay-at-home pack saw selling pressure, PTON was especially under pressure. The stock had risen 440% in 2020 as stay-at-home stocks rallied. However, now the stock has fallen to levels last seen at the beginning of 2020. What’s wrong with PTON stock and should you buy the dip in the stock?

Peloton stock recent developments

Peloton has reportedly hired management consulting giant McKinsey to study the business structure and suggest steps to reduce the costs. The company already has a hiring freeze in place and has reportedly asked employees at the retail stores to take customer service calls during lean periods. At the end of June, the company had 123 stores in North America and Europe. As part of the cost-cut initiatives, it might close down some of the stores. The company had 6,743 employees in the US at the end of June, which was over twice what it had a year back.

68% of all retail investor accounts lose money when trading CFDs with this provider.

PTON had slashed its guidance

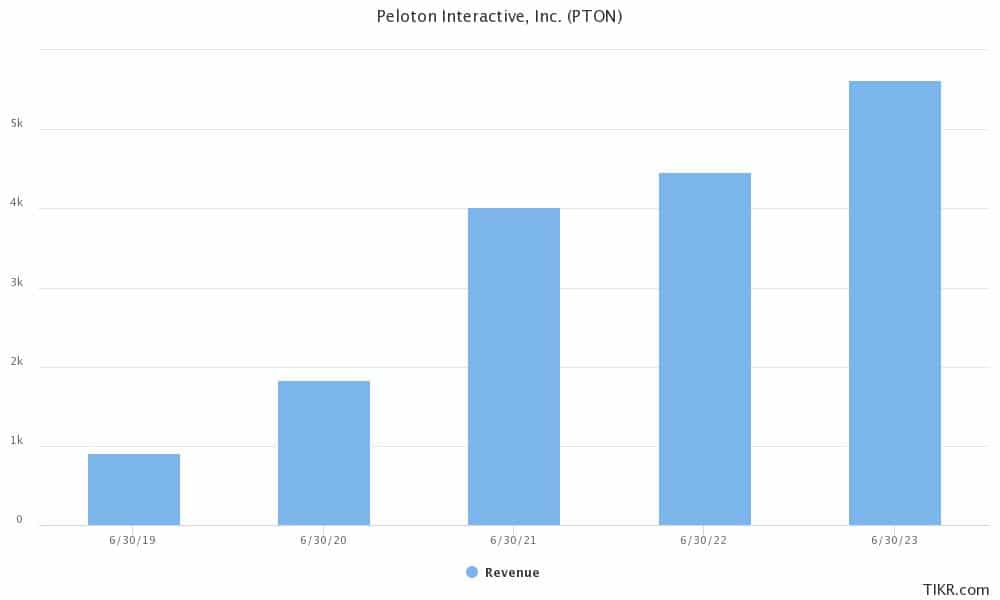

To be sure, the hiring spree made sense for Peloton as it was witnessing super high growth. However, the company’s growth has slowed down as was evident in the recent earnings. Peloton also lowered its guidance for the fiscal year during the earnings call in November. It said that its revenues would be between $4.4-$4.8 billion in the full fiscal year, which was way below the previous guidance of $5.4 billion. The company expects to post gross margins of 32% in the year. PTON expects to have between 3.35-3.45 million connected subscribers by the end of the year. It, however, expects to post an EBITDA loss between $425-$475 million in the year.

During the September quarter, it added 161,000 connected subscribers which were the lowest in two years. The topline growth for stay-at-home winners has come off as consumer behavior is reverting back towards pre-pandemic times.

Beachbody, which went public through a SPAC reverse merger last year, and expected to capitalize on the strong demand for stay-at-home health equipment companies, is also trading at a fraction of its highs.

Peloton is looking to raise prices

Meanwhile, amid the cost pressures, Peloton has announced that buyers would have to pay an additional fee for equipment delivery and set up. Last year, the company had to lower the equipment prices amid sagging demand. However, like many other companies, PTON is also facing higher costs amid the supply chain issues and labor shortage.

Commenting on the increased costs, a PTON spokesperson told CNBC, “Like many other businesses, Peloton is being impacted by global economic and supply chain challenges that are affecting the majority, if not all, businesses worldwide.”

The spokesperson added, “Even with these increases, we believe we still offer the best value in connected fitness, and offer consumers various financing options that make Peloton accessible to a wide audience.”

PTON stock target price

Wall Street analysts have a mixed opinion on PTON stock. JPMorgan believes that the stock might come down further and it would be prudent to wait on the sidelines for now before buying. Raymond James analyst Aaron Kessler expects Peloton to slash its guidance for the full year yet again when it reports the fiscal second-quarter earnings.

However, Loop is bullish on the stock and reiterated its buy rating while lowering the target price from $110 to $90. The target price implies an upside of almost 200% from these levels.

In its note Loop said, “However, there are reasons to be bullish, or at least, reasons to be less bearish than PTON’s underperforming share price might otherwise suggest, including: 1) recent app store rankings and social media trends have been encouraging; 2) potential ‘short squeeze’ given PTON’s high short interest; and 3) valuation, in our view, implies a ‘free call option’ on new category and product launches.”

Peloton stock forecast

Wall Street analysts have a split rating on PTON stock and 15 of the 31 analysts covering the stock rate it as a buy. 14 analysts have a hold rating while the remaining two rate it as a sell. The stock’s median target price of $70 is a 131% premium over current prices. Since the company’s earnings release in November, analysts have been slashing their target price and the current consensus target price is almost half of what it was prior to the earnings.

PTON stock long term forecast

The long-term outlook for home fitness equipment companies like Peloton looks positive. While the growth rates of 2020 might not be sustainable, the industry should see secular growth over the long term. PTON is also building a factory in the US to support the demand.

From the home fitness market, Peloton is now also diversifying into the commercial market. Earlier this year, it had acquired Precor and is now integrating the two businesses to target the hospitality sector. International expansion would also drive value for Peloton.

We could see a hybrid model in workout also and both gyms and home fitness equipment companies can flourish.

Should you buy Peloton stock now?

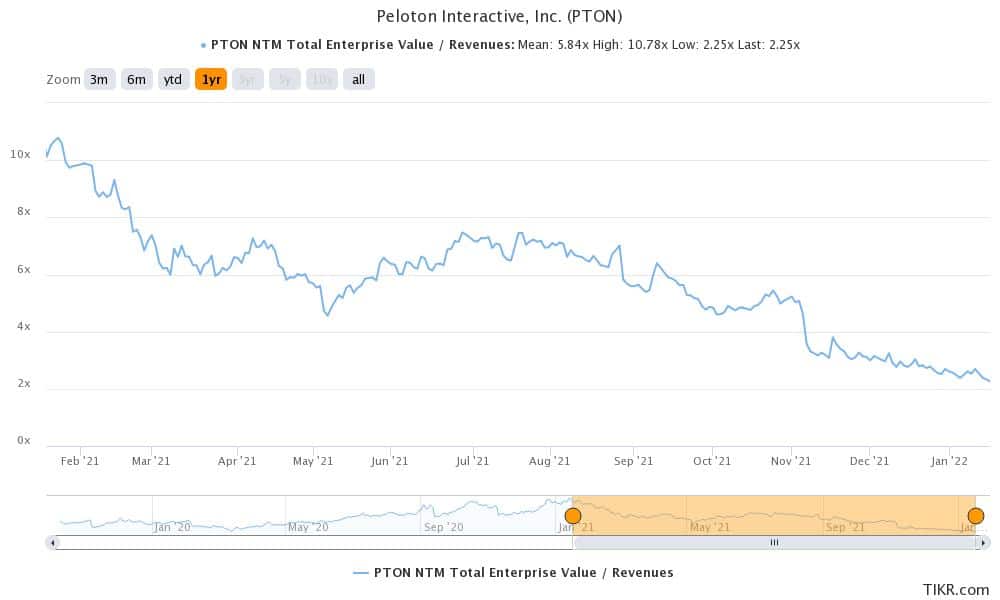

Peloton stock now trades at an NTM (next-12 months) EV-to-sales multiple of 2.25x which has started to look attractive. However, the company has to address the margin issues. The expected rate hikes by the Fed are also negative for PTON stock.

The rate hikes are especially negative for growth names that have their earnings skewed towards the future. These cash flows get discounted at higher rates thereby reducing their present value and by extension the fair value of the stock. However, if you are willing to take the extra risk, PTON could be a multibagger stock.

Buy TRAD Stock at eToro from just $50 Now!