Ocado Stock Down 4% in August – Time to Buy Ocado Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Ocado shares are down almost 4% since the month started while the price action has broken multiple support areas – a situation that could result in further downside for the stock in the following weeks.

Meanwhile, since 2021 started, Ocado shares have gone down almost 22% as investors believe that the pandemic tailwind that lifted the firm’s results during 2020 will eventually fade as vaccines in the United Kingdom continue to be rolled out at a fast pace.

With Ocado stock trading around 39% below its 52-week high, could this be an opportunity to buy shares of this successful online grocery store at a significant discount? In the following article, I’ll take a look at the firm’s fundamentals and growth prospects while analyzing the latest price action to possibly answer that question.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Ocado Stock – Technical Analysis

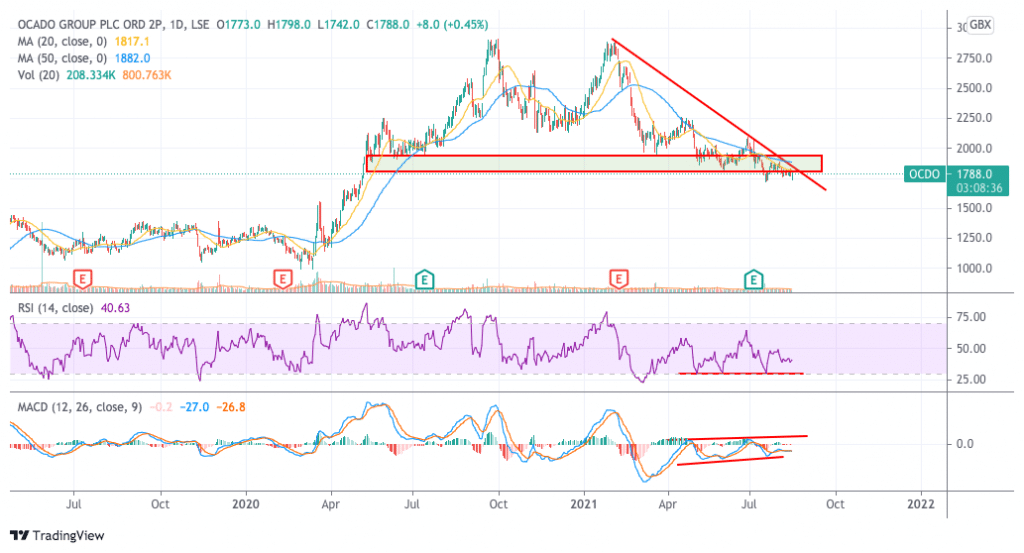

Ocado stock has been on a downtrend since February this year following a rejection of the 2,900 level that resulted in the formation of a double-top pattern. Since then, the price action has been posting a series of lower highs and has not shown any signs of finding a bottom just yet.

In fact, the latest downticks in the stock price have effectively broken an important area of support for Ocado and this situation could indicate that the downtrend could prolong for longer than expected.

In this regard, trading volumes during the 19-20 July session were particularly high as the stock price posted a fresh 52-week low and they were also fairly elevated in the past few days as the stock has moved near that level.

Currently trading at 1,787.5p the stock is standing only 4% above that 52-week low and this shows the extent of this latest weakness.

That said, it is important to note that momentum readings are signaling that Ocado shares may have already hit a short-term bottom as the Relative Strength Index (RSI) has not posted a lower low despite the price plunging to lower levels.

Moreover, the MACD appears to be on an uptrend despite the price remaining on a downtrend, which results in a bullish divergence.

Moving forward, if the price action manages to reverse the downtrend by breaking above the trend line shown in the chart above, chances are that Ocado shares could recover some of their lost territory.

Ocado Stock – Fundamental Analysis

Ocado sales have doubled in the past four years as they have moved from $1.58 billion back in 2016 to $3.1 billion by the end of 2020. However, most of that positive performance came on the back of a strong pandemic tailwind as the company managed to push its sales 36.4% higher in 2020 compared to the previous year as online shopping volumes increased dramatically during lockdowns.

Meanwhile, from 2015 to 2020, the company has been progressively increasing the average number of orders received per week from 195,000 to 334,000 while the average order size has also climbed 55.6% during that period from £111.5 to £137.

Gross profit margins for the firm have been steadily climbing from an average of 34% in the past few years as well to around 36% and 37% in the past four quarters while the company has swung to positive EBITDA since the first quarter of 2021.

However, bottom-line profitability continues to be elusive for the firm while net losses appear to be expanding as the company continues to spend important amounts to keep growing its top-line results.

Moving forward, analysts are expecting to see the firm’s sales growing at an average rate of 17% per year while the company is expected to keep losing money for the next three years at least.

At its current valuation of $18.3 billion, the firm is trading at nearly 5 times its forecasted sales for 2021. Even though this multiple seems attractive for a company in such a promising sector, market participants seem to be expecting that revenue growth rates will decelerate moving forward as the pandemic may have moved the firm’s volumes close to their peak.

However, if the pandemic tailwind proves to endure even after the virus crisis is over, chances are that this valuation will expand on the back of higher revenue estimates for the firm moving forward.

As per its solvency, Ocado had nearly $2 billion in long-term debt by the end of the second quarter of 2021 on total assets of $5.9 billion including $2.4 billion in cash and equivalents and around $685 million in intangibles and goodwill.

This amount of debt seems fairly elevated and could be one of the reasons why the company’s valuation has been declining lately as Ocado significantly expanded its debt load since the third quarter of 2020.

The management’s decisions on how to deploy this sizable war chest will possibly influence the price of the stock depending on whether those moves contribute to improving the firm’s fundamentals or not as per the market’s perception.

Buy Stocks at Cedar FX, the World’s #1 trading platform!