Meta Stock is a Top Performer in 2023 and Wall Street Sees More Gains Ahead

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Meta Platforms (NYSE: META) stock is up over 73% in 2023 and is the second-best-performing S&P 500 stock. Wall Street analysts see the stock continuing its good run in the coming months.

Meta’s fortunes have whipsawed over the last couple of years. In 2021, its market cap surpassed $1 trillion amid euphoria over its metaverse business. However, the stock plunged over 65% in 2022 and was the worst-performing FAANG stock.

This year, it is not only the best-performing FAANG stock by a fairly wide margin but is also outperforming the wider markets.

Why is Meta stock outperforming in 2023?

Amid slowing growth, Meta has embarked on a massive cost-cutting exercise, and in two rounds it has announced 21,000 layoffs. Additionally, the company said that it won’t hire for around 5,000 open positions.

It has reduced its 2023 operating expense guidance to $86 billion-$92 billion which is $8 billion lower than what it provided originally.

The company’s CEO Mark Zuckerburg has touted 2023 as the “year of efficiency” which comes after a dismal 2022.

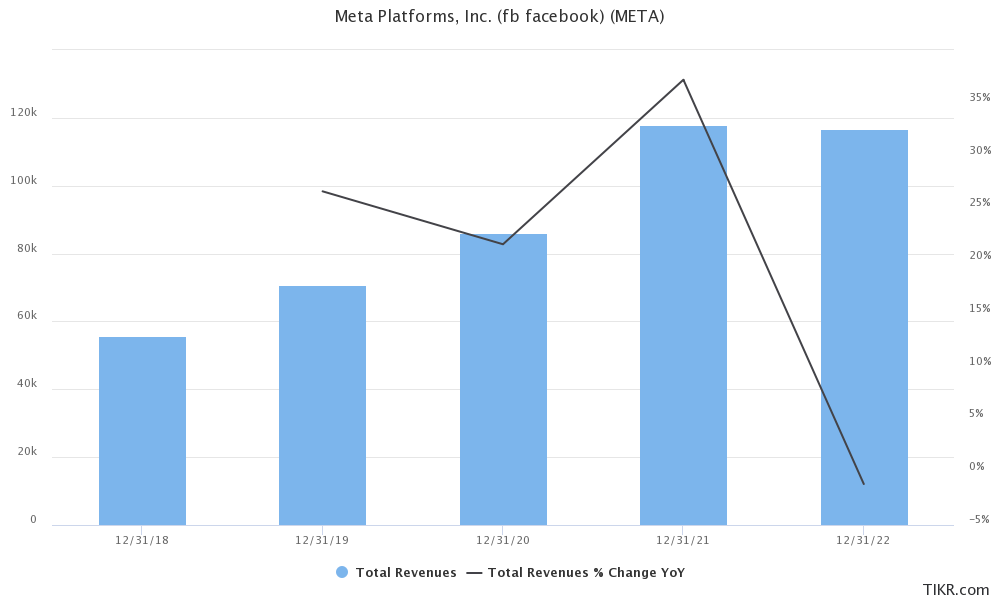

Meta’s revenues fell in 2022

Meta Platforms reported revenues of $32.17 billion in Q4 2022 which was ahead of the $31.53 billion that analysts were expecting. The actual results were towards the upper end of the $30 billion-$32.5 billion guidance that the company provided in the Q3 2022 earnings call.

The revenues however fell 4% YoY. The social media giant’s revenues have fallen YoY for three consecutive quarters and in the full year its revenues fell 1% to $116.6 billion. It was the first time in the company’s history that its revenues fell YoY in a year.

During the earnings call, Zuckerburg said, “But my main focus is on increasing the efficiency of how we execute our top priorities. So, I think that there’s going to be some more that we can do to improve our productivity, speed and cost structure. And by working on this over a sustained period, I think we’ll both build a stronger technology company and become more profitable.”

Zuckerburg said that in the short term, AI is the company’s priority. In the long term, however, he sees the metaverse as the company’s key driver.

Analysts see Meta as an AI play

Morgan Stanley and Barclays see Meta as among the top AI plays. In their note, Morgan Stanley said, “The leading platforms (GOOGL/AMZN/META) headline this list, and we show how AI-based advances (incremental revenue and opex efficiencies) could drive ~10%+ upside to our current price targets.”

JPMorgan’s Dough Anmuth sees more upside in Meta stock and raised his target price to $270 from $225. In his note, Anmuth said, “While Meta shares have more than doubled off the early November lows, we still think there’s meaningful upside ahead driven by accelerating revenue growth, continued cost efficiencies, and still attractive valuation.”

Zuckerburg sees a revival in growth

While’s Meta’s growth has sagged, Zuckerburg sees a revival. During the Q4 2022 earnings call, he said, “The first 18 years I think we grew it 20%, 30% compound or a lot more every year.” He added, “And then obviously that changed very dramatically in 2022, where our revenue was negative for growth, for the first time in the company’s history.”

Commenting on the slowdown, Zuckerburg stated that “We don’t anticipate that that’s going to continue.” He, however, added that the company’s growth rates would not rise to what it has witnessed in the past.

For Q1 2023, Meta Platforms forecast revenues between $26 billion to $28.5 billion. The company posted revenues of $27.9 billion in the first quarter of 2022. Its guidance implies a YoY rise in revenues if the actual sales come at the upper end of the guidance.

Meta to scale up stock buybacks

During the Q4 2022 earnings call, Meta Platforms announced a $40 billion stock buyback program. Last year, the company repurchased almost $28 billion worth of its shares and had another nearly $11 billion available for authorized buybacks. It ended 2022 with cash and cash equivalents of $40.74 billion while the long-term debt is just under $10 billion.

What’s Meta doing to revive growth?

Meta has started offering paid verification like Twitter. It would charge $11.99 monthly if the subscription is taken on the web but the service would cost $14.99 on the Google and Apple app stores.

Incidentally, Twitter also charges a higher amount on the app stores in an apparent bid to make up for the app store fees.

Meta also wants to use generative AI to create ads.

Metaverse could be a long-term growth driver

Meta Platforms’ investments in the nascent metaverse business have irked many investors. The business posted a loss of $13.7 billion in 2022. In the past, Zuckerburg has defended the investments and said that they are crucial for the company’s long-term success.

While Wall Street has a mixed outlook for Meta’s metaverse business, most analysts are constructive on the company’s AI plans which could be a near-term driver.

Tech companies have scaled up their AI bets amid the growing euphoria. Not only US, but Chinese companies have also outlined massive AI investments.

After ChatGPT and Google, Baidu, and Alibaba have also unveiled their AI chatbots.

Coming back to Meta, we’ll next hear from the company when it reports its Q1 2023 earnings later this month. Among others, the company might provide color on its AI plans