Macy’s Stock Price Rises 18% – Time to Buy M Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

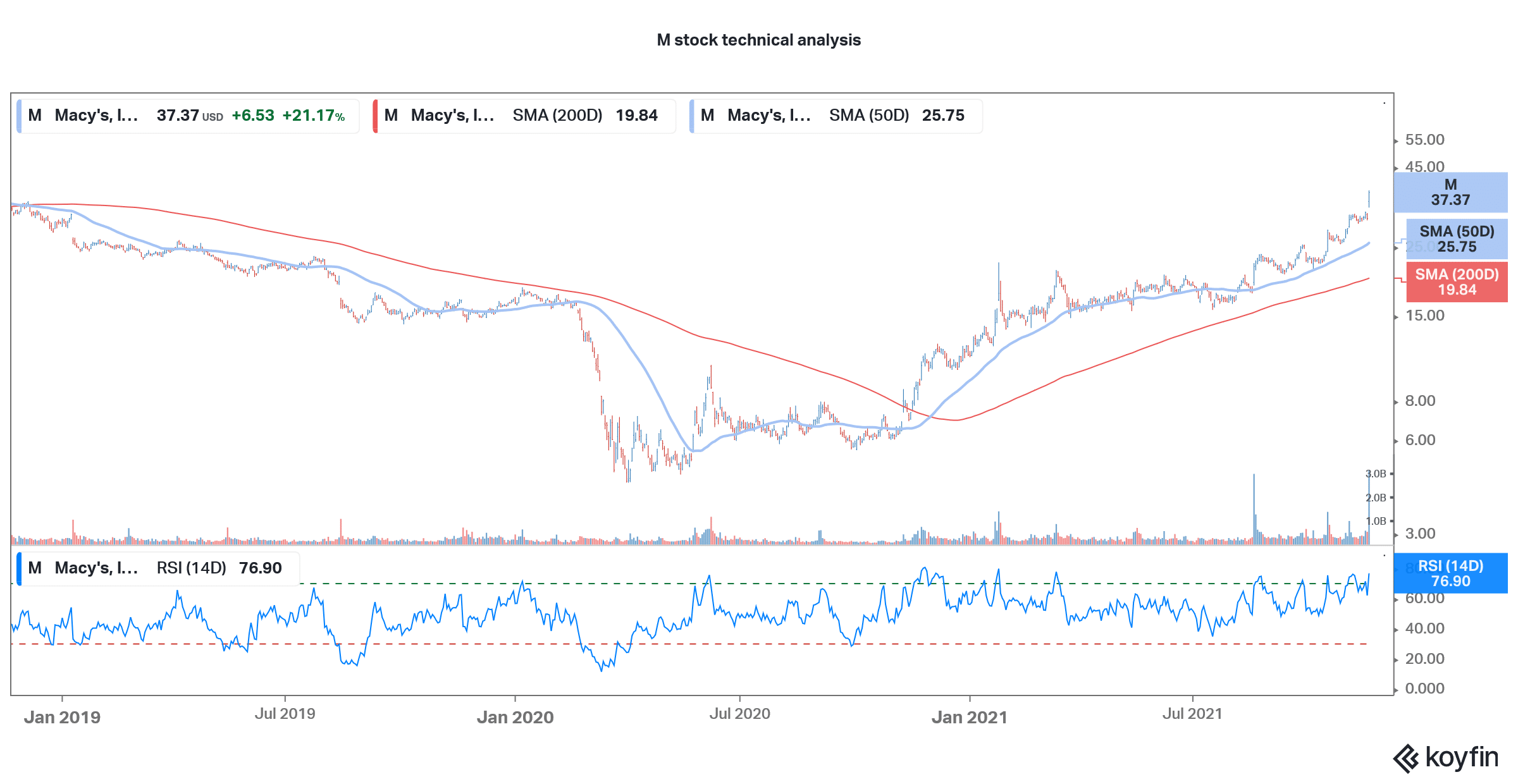

Macy’s Stock rose over 18% in yesterday’s price action which took its YTD gains to an impressive 232%. The stock is outperforming the markets as well as retail peers by a big margin this year.

What’s the forecast for M stock and is it still a good buy despite the massive gains this year?

Macy’s released its fiscal third-quarter earnings

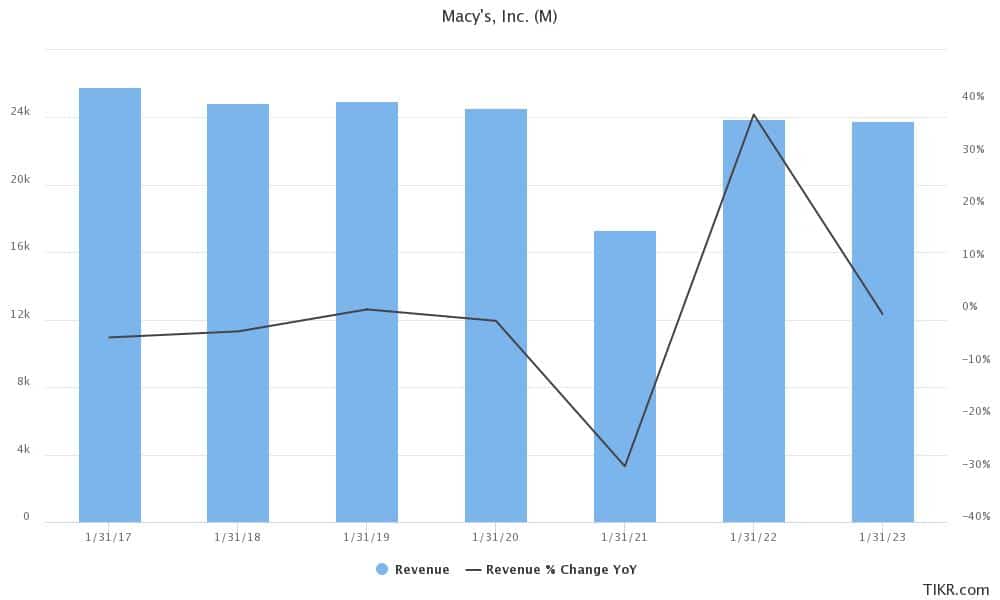

Macy’s reported revenues of $5.4 billion in the fiscal third quarter which were higher than the $5.2 billion that analysts were expecting. The company’s comparable sales increased 37.2% on an owned basis and 35.6% on owned plus licensed basis. Its comparable sales on an owned basis increased 8.9% as compared to 2019.

Notably, US retail sales have bounced back sharply from the pandemic lows. The October retail sales data showed sales rising 1.7% on a monthly basis in October, which was the highest pace of increase since March. The sales increased 16.3% on a YoY basis and were 21.4% higher as compared to the pre-pandemic levels in 2019.

This week, several retail giants like Walmart, Target, Lowe’s, and Home Depot have reported their fiscal third-quarter earnings. The earnings were generally good across the board even as the markets’ reaction was different. Target, for instance, tumbled despite posting earnings beat.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Key takeaways from M’s third-quarter earnings

Macy’s reported an adjusted EPS of $1.23 in the fiscal third quarter, which was far ahead of the $0.31 that analysts were expecting. During the quarter, it repurchased $300 million worth of its shares and also repaid $1.6 billion of debt ahead of maturity. It added 4.4 million new customers to the Macy’s brand, which is 28% higher than 2019.

Expressing optimism over the results, Jeff Gennette, Macy’s CEO said “Our company delivered another strong quarter and exceeded our expectations on both top and bottom lines. The results were driven by the effective execution of the Polaris strategy and an improved economic environment.”

M raised its guidance

Meanwhile, apart from the stellar earnings beat, Macy’s also raised its full-year guidance. It now expects to post revenues between $24.12-$24.28 billion in the fiscal year as compared to the previous guidance of $23.55-$23.95 billion. Incidentally, the company had posted earnings beat in the second quarter also. It had also raised its guidance back then which led to a steep rise in its stock.

Macy’s now expects to post an adjusted EPS between $4.57-$4.76 in the full year. The company is forecasting an adjusted EBITDA margin in excess of 12.5% in the year which is higher than the previous guidance of 11-11.5%.

Macy’s looking to spin off the e-commerce business

Meanwhile, another notable highlight of Macy’s earnings release was the announcement related to the e-commerce business. M has hired AlixPartners to study its business structure. Notably, activist investor Jana Partners has been pushing Macy’s to split its e-commerce business.

During the earnings call, Gennette said “We also recognize the significant value the market is assigning to pure e-commerce businesses.” He added, “And as we look at the landscape today, we are undertaking additional analysis that could help inform our long-term strategy to further unlock value for Macy’s.”

Notably, there has been a series of such splits and breakups and recently General Electric and Johnson & Johnson announced a breakup. GlaxoSmithKline is also on track to split the consumer business from the pharma business. The idea behind these splits is to unlock the value of different assets.

For instance, the e-commerce business attracts a higher valuation multiple as compared to brick-and-mortar retail business. Luxury chain Saks Fifth Avenue also split the e-commerce operations earlier this year. Meanwhile, Macy’s has clarified that no definitive decision on the spin-off of the e-commerce business has yet been taken.

Macy’s stock forecast

Wall Street analysts have a bearish forecast for M stock. While analysts have been raising their target price, Macy’s continues to trade well above the target price. It currently trades 27% above its median target price of $27. However, its street high target price of $50 is a 33.8% upside over current prices. Of the 17 analysts covering the stock, only three rate them as a buy while eight have a hold rating. The remaining six analysts have a sell rating on M stock.

Meanwhile, some of the analysts are bullish on M stock. Cowen senior retail analyst Oliver Chen is among those who are bullish on M stock. He believes that the e-commerce business could be worth $40 per share. Jim Cramer is also bullish on the stock and says that it is on a strong growth path, pointing to the user growth numbers in the quarter.

M stock long-term forecast

The long-term forecast for M stock looks positive and it is a good turnaround story. Macy’s also announced that it has partnered with WHP Global to bring back Toys”R”Us to the US market. Macy’s customers would be able to shop these online as well through its 400 stores in 2022. The potential spin-off of the e-commerce business could be another driver for the stock.

Should you buy Macy’s stock?

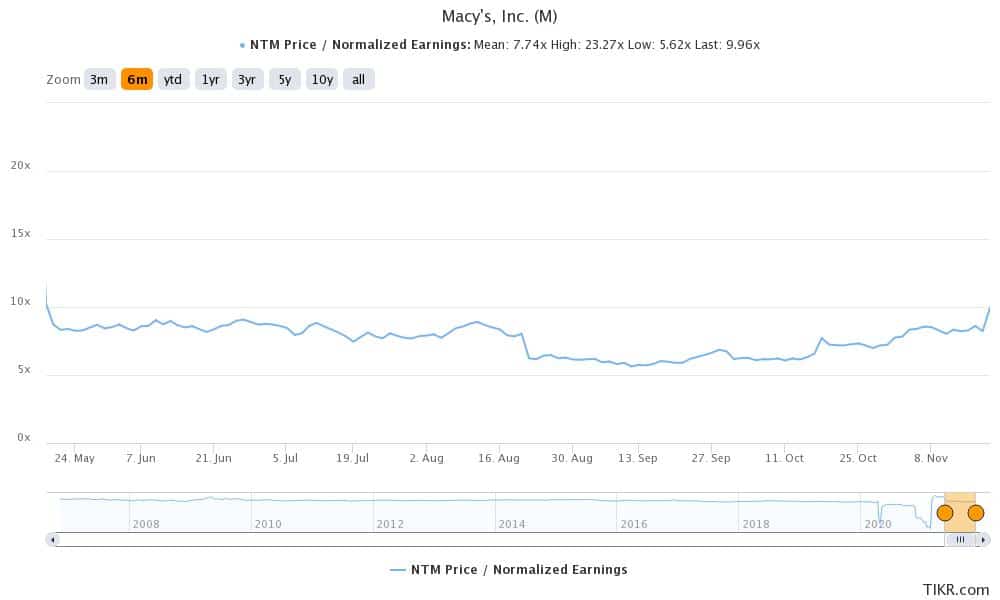

Macy’s stock trades at an NTM (next-12 months) PE multiple of only about 9.9x which is way below other retail peers. The company has been taking steps to lower its leverage which should help support the valuation. Also, the strong growth in the core business coupled with the expected spin-off of the e-commerce business makes M a good retail stock to buy.

Macy’s is also looking bullish on the charts and has been hitting new highs. Its trades above all key moving averages. However, after the recent surge, the stock has started to appear overbought with a 14-day RSI of 76.9. RSI values above 70 signal overbought positions.

That said, given its tepid valuations multiples and ongoing turnaround, M is one retail stock that should be on your radar despite it having more than tripled in 2021.

Buy M Stock at eToro from just $50 Now!