Lululemon Stock Down 11% in January – Time to Buy LULU Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Lululemon stock is down 11% since the month started following a couple of negative news concerning the company’s performance and legal situation.

On 6 January, Nike filed a lawsuit against the athletic apparel seller alleging that the company infringed multiple patents as a result of the commercialization of its Mirror Home Gym devices and mobile app.

The devices are commercialized by the company following the acquisition of Mirror back in July 2020.

In a statement concerning the matter, Lululemon said that “the patents in question are overly broad and invalid” and that they looked forward to defending their case in court.

The market reacted negatively to the news as LULU stock declined nearly 5% on the day that the lawsuit was filed.

Meanwhile, Lululemon announced on 10 January that it was expecting to see its revenues landing closer to the low end of the firm’s estimates for the fourth quarter of the 2021 fiscal year as the company experienced “several consequences of the Omicron variant”.

LULU estimated that sales for the quarter would be in a range between $2.13 and $2.17 billion. The company also said that adjusted earnings per share may also land near the low end of the firm’s forecasts at $3.24 per share.

What could be expected from this stock in light of these recent developments? In this article, I’ll be assessing the price action and fundamentals of LULU stock to outline plausible scenarios for the future.

68% of all retail investor accounts lose money when trading CFDs with this provider.

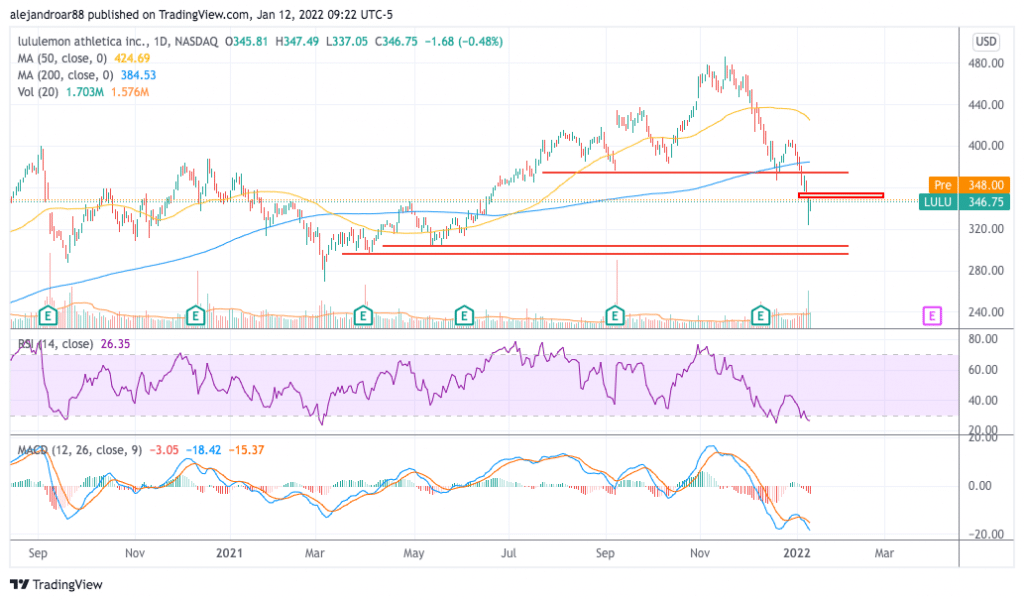

Lululemon Stock – Technical Analysis

The technical situation for Lululemon stock seems quite concerning as the price has broken below a crucial area of support found at the $375 level while the decline that the share price experienced after the firm’s downbeat comments regarding its Q4 2021 guidance left behind a small bearish price gap.

The price has also broken below all of its short and mid-term moving averages and trading volumes on the day that the guidance revision announcement came out spiked to nearly three times the 10-day average.

Momentum indicators are also quite bearish as the Relative Strength Index (RSI) is dropping to oversold levels for the second time in a month while the MACD remains neck-deep into negative territory and below the signal line. Additionally, negative histogram readings have been steadily increasing.

All things considered, the outlook for Lululemon stock is bearish as these recent news along with the firm’s Omicron-prompted decline – which seems to have started in November – have created the perfect storm to depress the company’s short-term prospects.

Lululemon Stock – Fundamental Analysis

Sales of Lululemon have been growing at a fast pace in the past five years at least moving from $2.3 billion back in 2017 to $5.9 billion in the past 12 months.

During that same period, gross margins have been improving moving from the low 50s to the high 50s while operating margins have fluctuated between 18% and 21%. The firm has a solid earnings generation capacity with net margins averaging around 15% during this same period.

From 2017 to 2020, diluted GAAP earnings per share have more than doubled from $2.21 to $4.5 per share resulting in a compounded annual growth rate of 19.5%.

Meanwhile, the firm has no long-term debt and reported total assets of $4.57 billion including $1 billion in cash by the end of the third quarter of 2021.

Lululemon has also been growing its free cash flows per share rapidly, moving from $1.73 to $4.41 in the same period mentioned above at a 26.4% CAGR. Meanwhile, its free cash flow margin has stood above 10% in all of these years.

Based on yesterday’s closing price of $347 per share, the company is trading at 37 times the market’s forecasted earnings for the 2023 fiscal year – which ends in January next year.

Additionally, using a conservative 12% FCF margin, the company will be generating around $900 million in free cash flows by then. At its current market cap, this figure results in a P/FCF ratio of 50x and gives the company enough money to keep buying back shares at the same pace it has in the past twelve months.

All things considered, even though LULU’s trading multiples might seem a bit high, the firm’s robust balance sheet, strong brand, and incredible track record of sales, earnings, and FCF growth are quite attractive and justify this elevated multiple.

If the price continues to decline, that would only make the stock more attractive for a long-term investor.

Buy LULU Stock at eToro with 0% Commission Now!