JD.com Stock Down 17% in July – Time to Buy JD Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The stock of JD.com, China’s largest e-commerce retail company, is down 17% so far in July while it is dropping as much as 6% during today’s early stock trading action as the latest wave of regulatory crackdowns from Chinese authorities continues to spook investors.

Meanwhile, the stock has also plunged almost 40% from its 52-week high of $108.3 per share and that is a good reason to take a second look at the business to see if this might be a good opportunity to take up some shares at what could be a bargain price.

Do you think there is an opportunity as well to buy this Chinese stock at a point when sentiment has turned negative? Join me in this article as I take a look at the company’s fundamentals to see if it is cheap enough to justify the risk.

67% of all retail investor accounts lose money when trading CFDs with this provider.

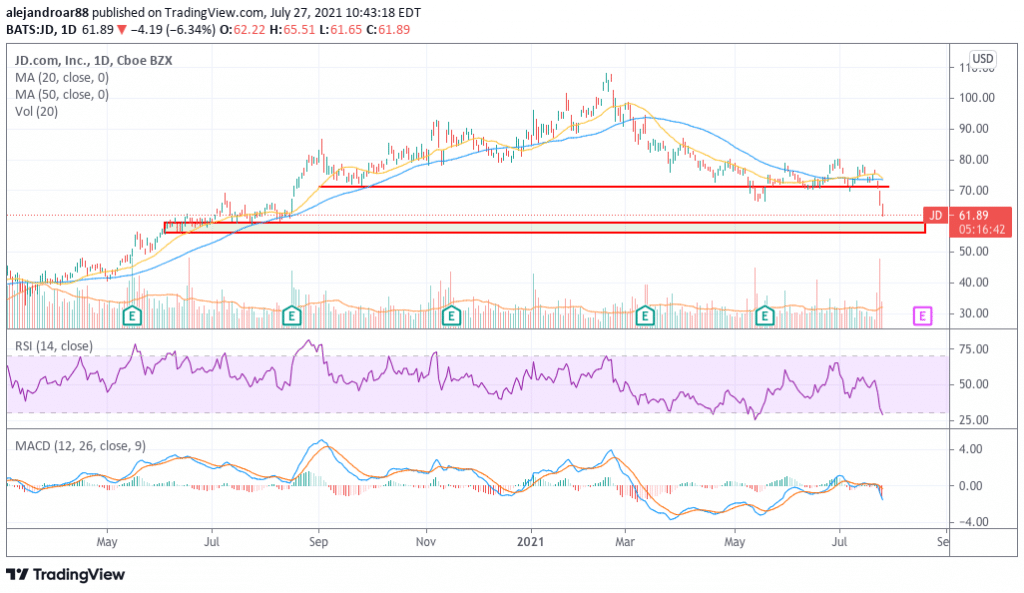

JD.com Stock – technical analysis

The latest price action seen by JD stock shows that the price is approaching an important area of support dating back to June last year at around $55 per share. However, momentum oscillators are just starting to move to negative territory which reinforces the view that the meltdown could just be getting started.

In this regard, the MACD has just posted its third consecutive negative momentum reading while the Relative Strength Index (RSI) is approaching oversold levels for the first time since May.

There is still a fair share of downside risk if the stock is to land at the lower bound of that support area as that could result in losses of around 15%. Meanwhile, trading volumes in the past two days have been quite high, which illustrates the extent of the sell-off.

Only yesterday, nearly 40 million shares exchanged hands, a number that was almost 4 times the 10-day average. It seems that investors are playing hot potato with the stock and that could lead to further losses, especially if the government reveals further regulatory guidelines for the tech sector specifically.

Based on these readings, JD’s stock price has all the characteristics of a falling knife and it is commonly not a good idea to try to catch one before it hits the floor. For now, long-term investors should wait until the dust settles a bit and the market finds a place to rest its overly pessimistic outlook for Chinese equities.

From that point forward, based on a diagnosis of the fundamentals, there might be some upside potential ahead. However, for now, falling knives can be quite hurtful for a portfolio.

JD.com Stock – fundamental analysis

JD’s sales have been growing at a fast pace for years as they have doubled from 2017 to 2020 as a result of a jump in online shopping volumes – especially during the pandemic. On average, revenues have been growing at a rate of 25% per year while gross margins have progressively improved from 7% to 8%.

The same can be said of operating margins as JD.com has managed to turn a profit since 2019, swinging from a $362 million loss back in 2018 to $7.6 billion in net income by the end of 2020 resulting in $2.43 in GAAP diluted earnings per share for its common stock and $4.86 per share for its ADS.

That said, the firm’s non-GAAP net income is perhaps a better measure of its profitability. In this regard, last year the company managed to generate $0.81 in diluted non-GAAP earnings per share, nearly the same figure it brought back in 2019 but 44% more than it reported in 2018.

Moving forward, analysts are expecting to see JD’s revenues jumping almost 30% this year and 23% the year after while non-GAAP diluted EPS are expected to land at $1.3 in 2021 for a 68% advance and $2.23 the year after for a 63% jump.

Based on these optimistic earnings forecasts, the current forward P/E multiple for JD – currently standing at 48 – seems fairly attractive. However, these estimates are not necessarily reflecting the risks that the company is facing as a result of the government’s latest hostile actions against businesses within the tech space.

For now, no actions have been taken by the government that have a material effect on JD’s operations or financial performance. If we compare JD.com with Amazon, its US-based peer, the company’s market capitalization accounts for only 6% of that of the US retail giant even though JD brings 25% of the sales volume than Amazon does.

Meanwhile, JD also generated a third of the earnings seen by Amazon during 2020 and it is expected to keep growing its bottom-line results significantly moving forward.

All things considered, from a fundamental perspective, the margin of safety displayed by JD.com shares at the moment is high enough to justify a long position. However, it could be a while before the stock reverses its current downtrend as fears about more hostile actions toward the Chinese tech sector would have to dissipate first before that happens.

If you have the stomach to tolerate some more losses along the way, this Chinese stock might be a good value pick for the long run if, and only if, the government doesn’t bar it from turning a profit.

Buy Stocks at Cedar FX, the World’s #1 trading platform!