EQT Corporation Stock Up 21% in September – Time to Buy EQT Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of EQT Corporation stock is up more than 20% so far in September as natural gas prices have surged on the back of a supply-demand imbalance that could deepen during the winter season in both the United States and Europe.

In September alone, the price of natural gas has jumped more than 30% at $5.8 per mmBtu and EQT Corporation is positioned to benefit from this ongoing shortage as the company is considered the largest natural gas producer in the United States accounting for around 6% of the country’s total production.

However, the company announced yesterday that a group of shareholders will be selling a total of 25.93 million shares at $20 per share or 9% below yesterday’s closing price along with another 3.89 million shares that could be sold by underwriters via a 30-day option granted by the company.

This markdown in the price of EQT stock is prompted a 5.3% decline in the price so far this morning in pre-market stock trading action and may weigh in the performance of the issue moving forward.

Can shares of this Pittsburgh-based company continue to rise on the back of higher natural gas prices or is this uptrend poised to experience a reversal following the sale of these shares? In the following article, I’ll discuss some of the factors that are influencing the current jump in EQT Corporation stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

EQT Corporation Stock – Technical Analysis

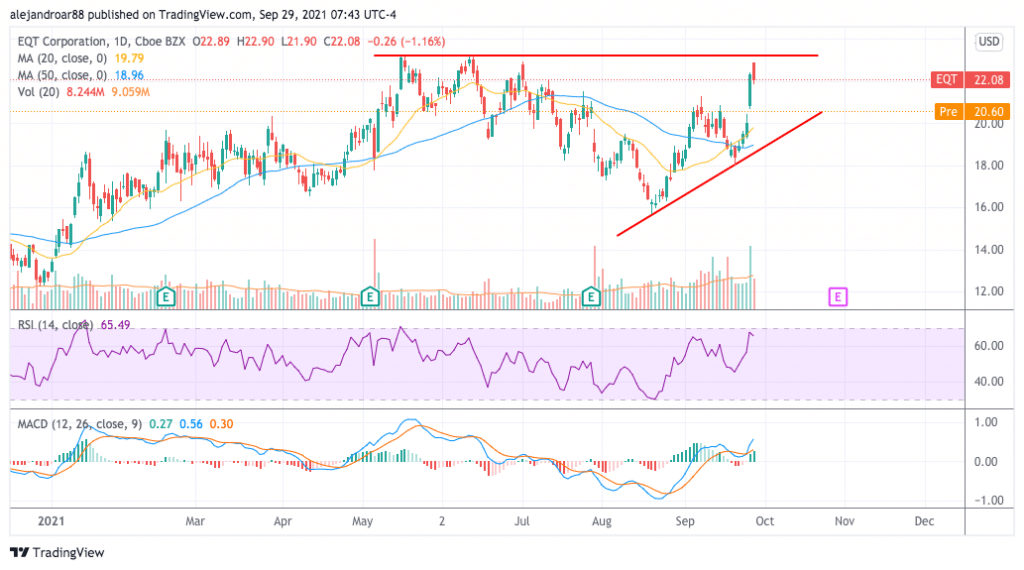

EQT stock experienced a pronounced four-day rally from 22 to 27 September that ended pushing the stock near its 52-week high of $23 per share. However, yesterday 1.2% downtick put an end to this short-term uptrend and this share offering announcement may have sealed the deal for what could a full-blown trend reversal for EQT.

To some extent, the price was climbing at an unsustainably accelerated rate as the stock traded 14% above its 20-day moving average on 27 September after going up almost 12% on that single day.

Therefore, yesterday decline was somehow expected although today’s sharp drop was probably not.

Trading volumes back in 27 September exceeded the average by more than two times and momentum oscillators remain positive and pointing to a bullish outlook as the Relative Strength Index (RSI) is rising near overbought levels while the MACD crossed above the signal line accompanied by steadily increasing histogram readings.

If this pre-market drop spills over to the live session as is, that could be a buying opportunity as the $20 price tag given to this share offering may act as a floor for EQT stock moving forward while higher natural gas prices in the future may continue to push the stock price higher.

EQT Corporation Stock – Fundamental Analysis

Data from the Energy Information Administration (EIA) shows how the imbalance in the supply and demand for natural gas in the United States is apparently resolving as demand has decelerated in the past few weeks amid lower demand from the electric power sector.

Meanwhile, supply volumes have increased lately as well as production in the Gulf of Mexico is coming back online after being almost completely shutdown amid the passing of Hurricane Ida.

Interestingly, natural gas prices have reacted negatively to these reports as they have declined 1.5% in the past two days.

However, supply of natural gas in the United States and overseas remain relatively constraint and higher demand in the winter may once again create an imbalance that would result in another spike in prices.

This favorable short-term headwind for the industry may result in higher top-line and bottom-line results for EQT, especially if gas producers manage to ramp up their output to a point that the imbalance remains but their revenues are benefitted by these higher volumes.

According to the company’s Q2 2021 earnings presentation, natural gas prices above $2.5 per MMBtu or so will allow it to produce free cash flows of $1.5 billion. Therefore, with prices standing at more than twice that level, EQT could produce over $2 billion in free cash flows during the next twelve months if this imbalance continues.

Currently, the company is being valued at $8.4 billion which results in a highly conservative price-to-FCF ratio of 2.8 using that forecasted 12-month FCF figure.

Meanwhile, the firm’s long-term debt seems manageable and the current tailwind may even allow it to pay off some of those commitments if the firm experiences a windfall on the back of this currently favorable environment.

All things considered, the outlook for EQT remains bullish and especially so if a supply/demand imbalance occurs in the United States again as a result of a spike in demand during winter season.

Buy EQT Stock at eToro with 0% Commission Now!