DocuSign Stock Price Falls 30% – Time to Buy DOCU Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

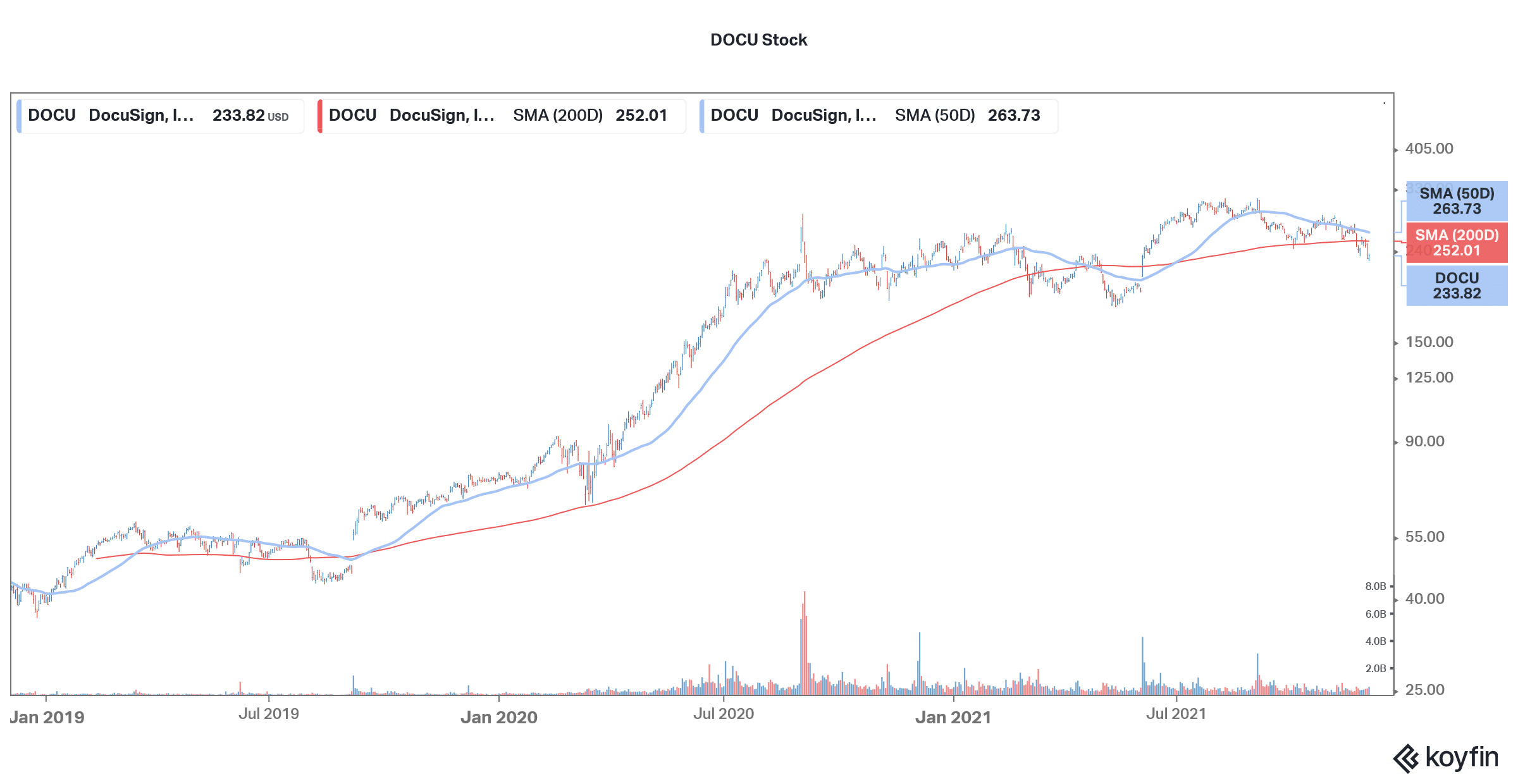

DocuSign (DOCU) stock was trading over 30% lower in US premarket price action today. The stock is up only about 5% for the year and looks set to plunge into the negative territory today.

DOCU is not the only so-called stay-at-home stock that is having a dismal run in 2021. The entire stay-at-home pack has looked weak this year amid slowing growth. Almost all the stay-at-home stocks which include Zoom Video Communications, Teladoc Health, Chegg, and Peloton are underperforming the markets by a wide margin this year. Amazon stock has also sagged and is underperforming the FAANG peers this year.

Stay-at-home stocks are underperforming

The basic thesis behind the underperformance of stay-at-home stocks is similar. These stocks saw a spike in revenues last year amid the lockdowns. As Zoom calls replaced physical travel and e-commerce replaced shopping at physical stores, there was a clear split in markets. While the stay-at-home plays did well, the old economy stocks underperformed. 2021 has meanwhile been a different story and cyclical and reopening plays have done well. That said, reopening stocks have come under pressure over the last week after the emergence of the Omicron variant.

68% of all retail investor accounts lose money when trading CFDs with this provider.

DocuSign earnings

Coming back to DocuSign, the company released its fiscal third-quarter 2022 earnings yesterday after the close of markets. It reported revenues of $545.5 million in the quarter which were ahead of the $531 million that analysts were expecting. Its adjusted EPS of $0.58 was also higher than the $0.46 that analysts were projecting. However, despite beating estimates for both the topline as well as bottomline, DOCU stock is trading sharply lower today and looks set to hit a new 52-week low in today’s regular price action.

DOCU gave tepid guidance

DocuSign’s revenues have increased by more than 40% YoY for the last six consecutive quarters. The company was among the biggest beneficiaries of “work-from-home.” However, DOCU expects sales to slow down as more workers return to the office and the pandemic boost does down for stay-at-home companies. DocuSign witnessed a slowing growth in the fiscal third quarter only and total billings increased 28% which is below what we’ve been seeing over the last year.

DocuSign gave a lower guidance

DOCU expects to post revenues between $557-$563 million in the current quarter which would mean annual growth of only about 30%. DOCU joins the long list of companies that are now seeing their growth rates taper down. To be sure, markets don’t really expect these companies to repeat last year’s splendid growth. However, it’s the pace of slowdown that has been worrying.

Even for DocuSign, the management acknowledged that the slowdown is faster than they were expecting. “While we had expected an eventual step down from the peak levels of growth achieved during the height of the pandemic, the environment shifted more quickly than we anticipated,” said DOCU CEO Dan Springer during the earnings release.

DOCU stock forecast

Before DocuSign’s earnings release, Wall Street analysts had a consensus buy rating on the stock. Of the 22 analysts covering the stock, 17 had a buy rating while the remaining five had a hold rating. It had a median target price of $330 which is a premium of almost 41%. Its street high target price of $389 is a premium of 66.1%. Meanwhile, after the projected slowdown in growth, Wall Street analysts might revise down their ratings and target prices for the stock.

Incidentally, after DocuSign’s fiscal second-quarter earnings release in September, several brokerages including Evercore ISI, Morgan Stanley, Bank of America, and Needham had raised their target price on the stock.

In the short-term, stay-at-home stocks have been under visible pressure. Danielle Shay, director of options at Simpler Trading expressed his views on names like Zoom, Peloton, and DocuSign that plunged last month. She said, “The worst part about it is there’s still more pain to be had and there’s really no meaningful support, specifically in Peloton and Zoom.” She added, “While I like DocuSign here, I just can’t see a meaningful support level. And for those reasons, I think Zoom and Peloton still have some more downside.”

DocuSign stock long-term forecast

Meanwhile, DocuSign stock still looks a good long-term play and has a TAM (total addressable market) of $50 billion. It has over a billion users globally and 1.11 million of these are paying customers. All top 15 fortune 500 financial companies are its customers while 14 of the top 15 Fortune 500 healthcare companies are its customers.

DOCU is certainly seeing a growth slowdown, most of which was expected. However, the stock still looks like a good long-term buy and bet on the digitization theme.

Should you buy DOCU stock?

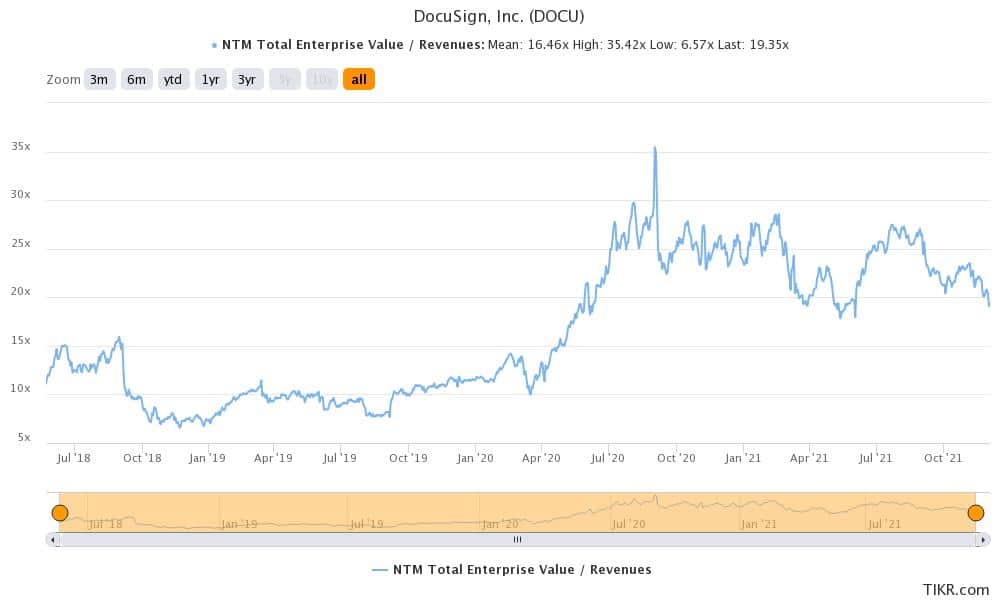

Looking at the valuations, DocuSign stock trades at an NTM (next-12 months) EV-to-sales multiple of 19.4x. The multiples are below the last year’s average but still way above the average multiples that the stock traded before the pandemic. For instance, at the beginning of 2020, DOCU stock traded at an NTM EV-to-sales multiple of only about 11x. The multiples peaked at 35.4x in August 2020 and have since gradually come down.

After the fall today, DOCU’s trading multiples would get more closer to the pre-pandemic levels. Today’s crash in DocuSign stock looks like a good opportunity to own this digitization play at reasonable prices.

Meanwhile, DocuSign stock is not looking too bullish on the charts. It has fallen 25% from the peaks and is in a bear market territory. With today’s price action, it looks set to plunge into an even deeper bear market. It also trades below key moving averages like the 50-day and 200-day SMA (simple moving average). However, from a fundamental perspective, the stock seems to offer good value now.

Buy DOCU Stock at eToro from just $50 Now!