DocuSign Stock Down 10% in November – Time to Buy DOCU Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of DocuSign stock is down 10% so far in November as the downtrend that started after the company released its latest quarterly report has accelerated until tagging a key area of support.

Back in September the document processing company reported better than expected sales and earnings for the second quarter of its 2021 fiscal year but a downtrend started only days after as sequential growth started to slow down.

Now, only a few days ahead of the firm’s Q3 2021 earnings release, the stock could be preparing to make a comeback upon taking a key support and aided by the possibility that businesses will continue to rely heavily on digital solutions if the Omicron variant of the virus turns out to be as transmissible and dangerous as some seem to believe.

In this context, what could be expected from DocuSign? In this article, I’ll be assessing the price action and fundamentals of this tech stock to outline plausible scenarios for what remains of the year.

67% of all retail investor accounts lose money when trading CFDs with this provider.

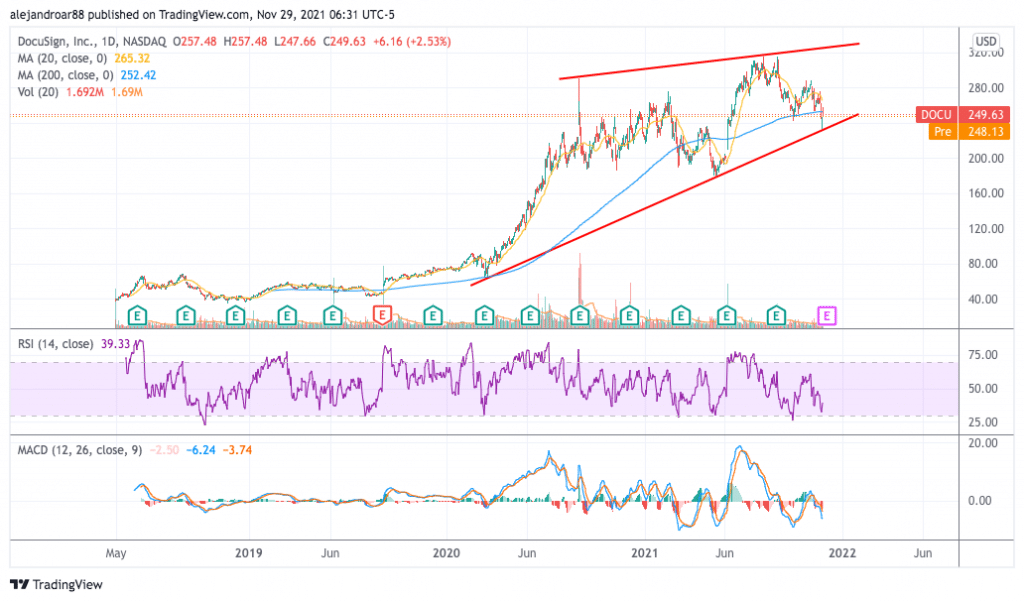

DocuSign Stock – Technical Analysis

The chart above shows that the price has tagged the lower bound of a long-dated rising wedge that started since the February-March pandemic crash as market participants jumped on DOCU stock amid the tailwind that the health crisis provided to its business.

Last Friday, the stock bounced off this relevant threshold in a session that saw the price rise by 2.5% at $249.6 per share on the back of the Omicron news. However, the intraday action kept the price of DOCU stock below its 200-day simple moving average and that is signaling weakness in investors’ interest for the stock despite this positive catalyst.

Moving forward, the 200-day SMA remains the most relevant resistance to overcome if bulls would like to take over the price action. Meanwhile, momentum indicators are still pointing to a bearish outlook as the Relative Strength Index (RSI) is standing at 39 – bearish – while the MACD remains below the signal line and has been steadily decreasing in the past couple of weeks.

DocuSign is scheduled to report its earnings for the third quarter of the 2021 fiscal year on 2 December and options prices are pointing to a 9% post-earnings fluctuation in the price of the stock.

DocuSign Stock – Fundamental Analysis

DocuSign sales have been growing at a fast pace even before the pandemic started as the firm’s top-line results advanced at an average of 35% per year from 2018 to 2020. However, growth during the pandemic accelerated as the company experienced a 49% increase in its revenues as businesses were forced to rely on digital solutions to keep operating while workers remained confined within their homes.

This year, the company expects to see its sales land at around $2.09 billion resulting in a 44% jump compared to a year ago. However, in the years to follow, Wall Street seems to be expecting slower top-line growth of less than 30% per year for the firm and that could be one of the reasons why DOCU stock has dropped following its Q2 2021 earnings release.

Currently, the company is being valued at $49.1 billion resulting in a forward P/S ratio of 27.4x and a forward EV/Sales ratio of 20.7x. Meanwhile, the firm’s operating and net income has remained negative but they have been progressively trimmed when measured as a percentage of revenue.

By the end of the last quarter, the firm had cash reserves of $823 million while DocuSign generated positive free cash flows of around $300 million during the first semester of the year. If one expects that free cash flows will end the year at around $600 million, the current valuation would result in a P/FCF ratio of 82x.

Overall, DocuSign’s valuation seems fairly stretched. This increases its downside risk and could justify further weakness in the stock price following the release of this upcoming earnings report.

With this in mind, if the trend line support is broken, chances are that the downtrend the stock has experienced lately could accelerate, possibly aiming for the $180 horizontal support as a short-term target.

On the other hand, if the appearance of the Omicron variant of the virus forces countries to reintroduce some restrictions concerning office work and other similar activities chances are that the stock price will recover to some extent. In that scenario, the stock’s short-term and long-term moving averages would be the most relevant resistances to overcome to favor the beginning of a fresh uptrend.

Buy DOCU Stock at eToro with 0% Commission Now!