DocuSign Share Price Forecast March 2022 – Time to Buy DOCU?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

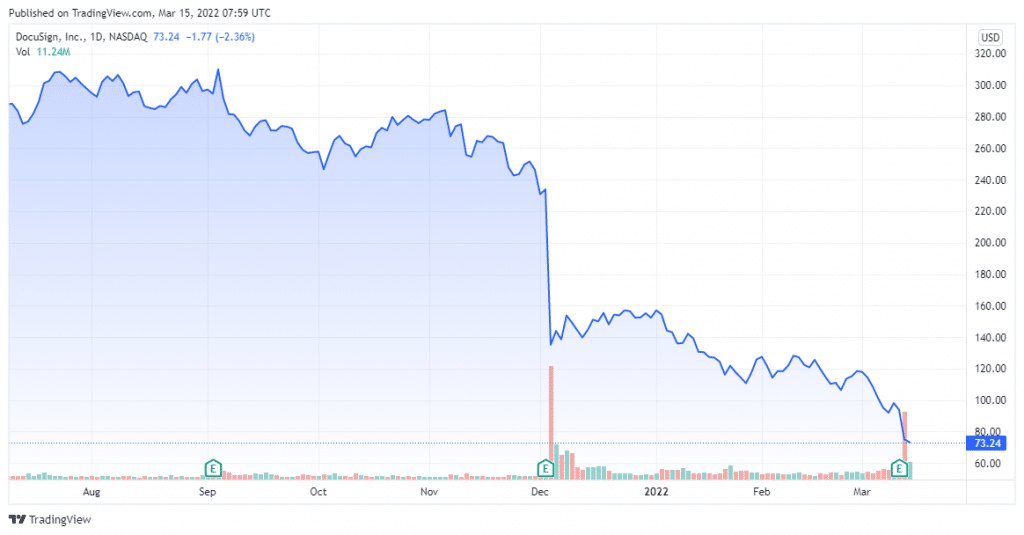

Shares of e-signature and electronic document company DocuSign (NASDAQ: DOCU) are in the red today, after closing at $73.24 as of March 14th (19:59 EST). DocuSign shares fell by more than 20% on Friday after the company released its fiscal fourth-quarter earnings report. As a result, DocuSign shares shed 75% of their 52 weeks high of $314.16. The company has virtually lost all of the gains it experienced due to remote work and collaboration during the pandemic.

DocuSign – Technical Analysis

DocuSign’s financial statement indicates a market cap of $14.492 billion with total assets worth $ 2.541 billion. Revenue for 2021 was at $2.11 billion with a profit margin of -3.32% compared to $1.45 billion in 2020. According to the fourth-quarter results, DocuSign’s total revenue was $580.8 million, an increase of 35% year-over-year, while subscription revenue was $564.0 million, an increase of 37% year-over-year.

Moving averages such as Exponential Moving Average (10)(93.14), Simple Moving Average (10)(96.96), Exponential Moving Average (20)(102.64), Simple Moving Average (20)(106.29) and Exponential Moving Average (30)(109.59) are indicating a sell action. Oscillators such as Stochastic RSI Fast (3, 3, 14, 14)(8.64), Williams Percent Range (14)(−95.73) and Bull Bear Power(−45.76) are neutral.

67% of all retail investor accounts lose money when trading CFDs with this provider

Recent Developments

DocuSign held its first IPO with shareholders such as Sigma Partners, Ignition Partners, Frazier Technology Ventures, and former CEO Keith Krach, back in 2018. It introduced the DocuSign Agreement Cloud, a suite of products and integrations for automating and connecting the entire agreement process digitally in March 2019. The company then went on to acquire Seal Software for $188 million.

DocuSign’s fiscal fourth-quarter results were impressive, with revenue increased by 35% year over year during the period, reaching $561 million. Other metrics include non-GAAP (adjusted) earnings per share of $0.48 increased from $0.37 in the year-ago period. The company’s free cash flow increased from $44 million in the year-ago quarter to $70.3 million.DocuSign announced a partnership with Zoom Communications on February 15th 2022.

While there isn’t any direct cause for the share price decline, many investors point towards the management’s guidance. The company’s management expects revenue for fiscal 2023 to be between $2.47 billion and $2.48 billion, compared to analyst expectations of $2.61 billion. However, this implies that there will only be 18% top-line growth for the current fiscal year.

Should You Buy DOCU Shares?

DocuSign has all the signs that point towards its business and its growth prospects remaining healthy. Management has made optimistic comments in its earnings release and has announced plans to roll out a share repurchase program. The company’s board of directors have authorised almost $200 million to be used for repurchasing its stock.

The share repurchase program will allow the company to flexibly leverage their balance sheet to efficiently deliver returns to its shareholders. Repurchase programs like this are a sign of the company’s confidence in its long-term potential.

Investors may want to look at DocuSign while it is down sharply, especially given the management’s confidence, the stock’s lower price, and the company’s strong fundamentals. They may have to re-evaluate their position if DocuSign’s revenue growth deceleration worsens beyond what management expects.

However, management blamed the growth deceleration on the lingering effects of the tapering of heightened demand from unprecedented lockdowns. There will be less degree of risk of deceleration of the anomaly period fades further into the past. Based on this, investors can go for Docu shares for the time being.

Buy DOCU Stock at eToro from just $50 Now!