Disney Stock Down 8% in 2022 – Time to Buy DIS Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

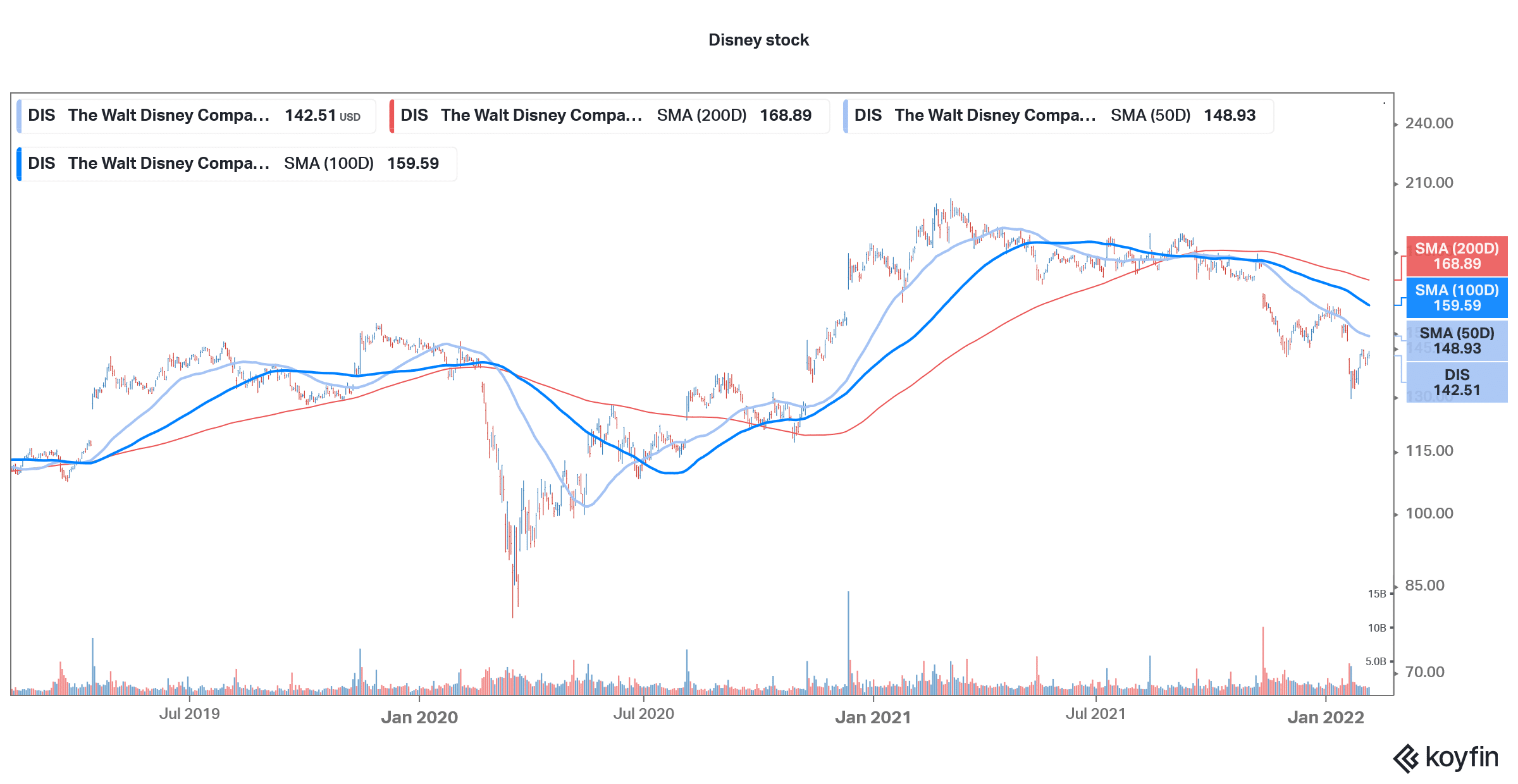

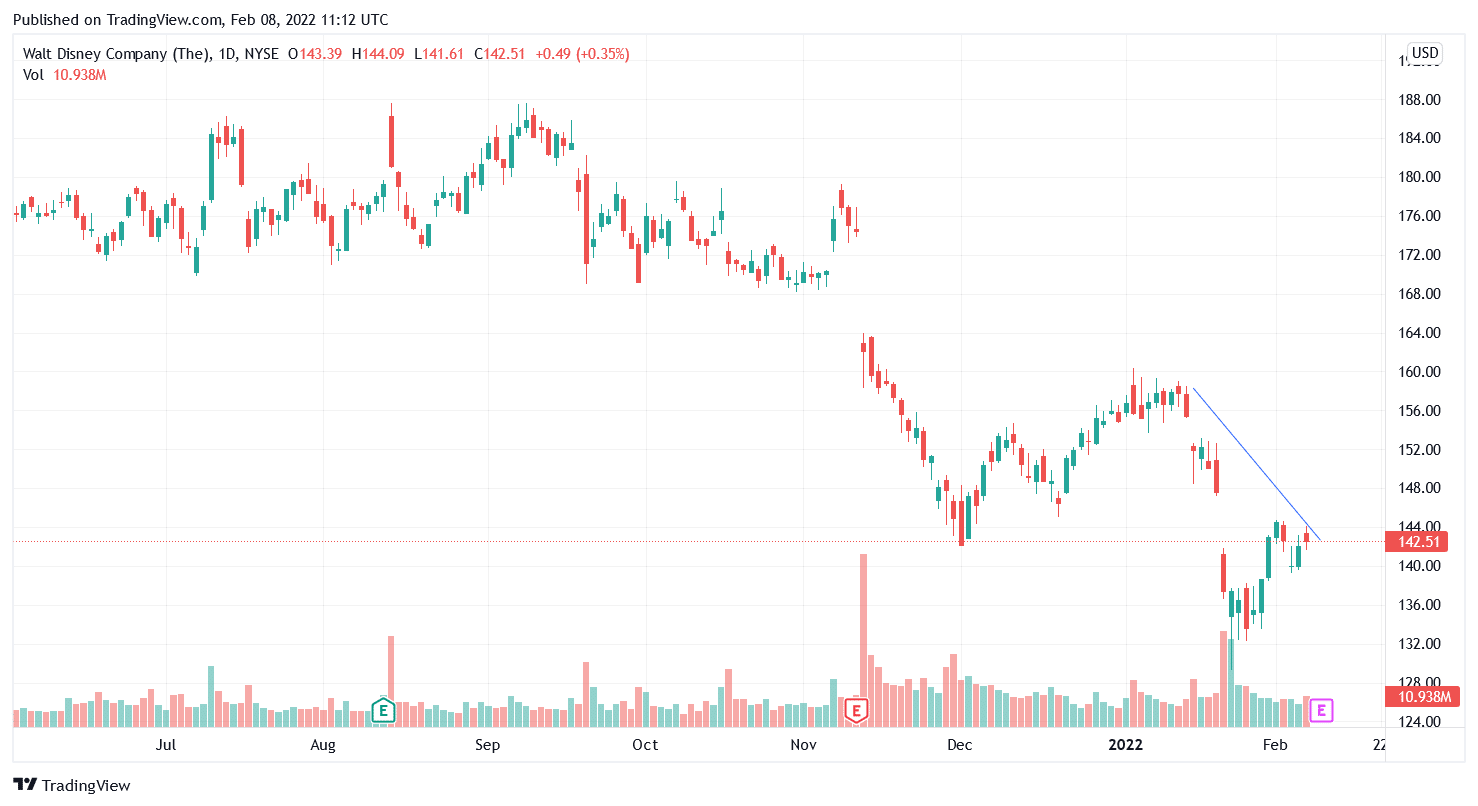

US stock markets have looked weak in 2022 and Disney (DIS) stock is no exception. The stock is down 8% in 2022. While the stock has recovered from the 52-week lows that it hit towards the end of January, it is still down almost 30% from the 52-week highs.

DIS stock is in a deep bear market territory having fallen more than 20% from its recent highs. The drawdown in DIS stock is much bigger than what we’ve seen in the broader markets. What’s the forecast for Disney and should you buy the stock now?

Disney earnings

Disney would release its fiscal first-quarter 2022 earnings tomorrow after the close of US markets. Analysts polled by Koyfin expect the company to report revenues of $20.96 billion in the quarter as compared to $16.25 billion in the corresponding period last year. However, the steep rise is coming from a low base effect as the company’s revenues were weak last year due to the COVID-19 related restrictions. Analysts expect Disney’s revenues to rise sharply in all quarters in this fiscal year. In the full fiscal year, its sales are expected to rise 23.8%. However, the growth is expected to cool down to 11.3% in the next fiscal year.

In the fiscal first quarter, analysts expect Disney’s adjusted EPS to more than double to $0.63. In the full fiscal year, the company’s adjusted EPS is expected to rise 74.5% to $4.06.

68% of all retail investor accounts lose money when trading CFDs with this provider.

DIS stock had fallen after fiscal fourth-quarter earnings

Disney reported its fiscal fourth-quarter 2021 earnings in November which disappointed on almost all the metrics. Disney’s streaming subscriber growth slowed down in the quarter and it added only 4.1 million paying subscribers. However, the company had forewarned about the slowdown well in advance, blaming lower content production. Also, in the quarter, the average monthly revenue per subscriber for Disney+ fell to $4.12, which was 9% below the corresponding period last year. The company said that the metric fell amid an unfavorable product mix as it had a higher percentage of Disney+ Hotstar customers in the quarter.

DIS also missed both the topline as well as bottomline estimates in the quarter which led to a crash in its stock price.

What to watch out for in Disney’s first-quarter earnings?

During Disney’s first-quarter earnings, markets would watch out for the trajectory of streaming subscriber growth. Also, the commentary on the near-term outlook for subscriber growth would be keenly awaited. Streaming giant Netflix gave a tepid subscriber growth outlook for the March quarter. While Netflix has been spending aggressively on new content and as a result does not expect its margins to expand in 2022, higher spending is not leading to a commensurate increase in subscriber numbers.

Also, for perhaps the first time the company talked about competition in the streaming industry. So far, it maintained that increasing competition is not really a worry but a sign that other industry players also see a massive opportunity in streaming.

DIS might also provide more color on the outlook for its Parks segment. The segment is expected to lead the near-term revival in the company’s earnings after the slump of the last two years.

DIS stock forecast

Disney’s forecast depends on the success of both its Parks and streaming divisions. The company’s streaming business is also facing growth issues in the short term. Wall Street analysts also have a bullish forecast for DIS stock and it has received a buy rating from 20 out of the 29 analysts polled by CNN Business. Nine analysts have a hold rating. None of the analysts rate the stock as a sell. Disney has a median target price of $196 which is a 37.6% premium over current prices. The street high target price of $220 is a premium of 54.4% over current prices.

Analysts revised Disney’s target price

After Disney’s fiscal fourth-quarter earnings, several analysts downwardly revised the stock’s target price. Barclays and Atlantic Equities also downgraded the stock after the earnings miss. Looking at the recent analyst action, yesterday, Credit Suisse reiterated DIS stock as overweight ahead of the company’s upcoming earnings release.

It said, “Structural streaming concerns also remain top of mind, including whether Disney+ can develop content to broaden out beyond its Disney/Marvel/Star Wars fan base and if Netflix’s slow growth patch suggests a corollary lesser streaming TAM/margin outlook for its competitors, like Disney+.”

Wells Fargo sees Disney stock as a top pick for 2022

Last month, Wells Fargo listed DIS stock as a top pick for 2022. The brokerage said, “The past few months have shown that DIS will likely face some serious content obstacles if it is to meet its FY24 subscriber guidance. Thus, the backdrop for DIS into 2022 is a proper execution story, in our view. Given DIS’s history in delivering the content goods, we think it’s an attractive set-up, so it’s our favorite large-cap growth idea for 2022.”

DIS stock long term forecast

Wells Fargo was talking about the ambitious 2024 streaming numbers that Disney is aiming for. Disney+ subscriber numbers to between 230-260 million by the fiscal year 2024. After adding the subscribers for Hulu and ESPN+, it expects to have been 300-350 million subscribers by then.

Disney stock technical analysis

Disney stock has been in a short-term uptrend after bottoming out last month. The stock has been facing stiff resistance at the 50-day SMA (simple moving average) which currently stands at $148.65. It also trades below the 30-day, 100-day, and 200-day SMA. The 14-day RSI (relative strength index) is 44.02 which is a neutral indicator while 12, 26 MACD (moving average convergence divergence) gives a buy signal.

Should you buy DIS stock?

DIS stock trades at an NTM (next-12 months) PE multiple of 35x which is above its historical averages. The stock has seen a valuation multiple rerating amid the aggressive pivot towards streaming. While the business has been posting losses and is not expected to post profits anytime soon, it would drive the profits in the long term.

That said, the market sentiments towards streaming companies have changed amid the rising competition and escalating costs. During their upcoming earnings call, Disney management might have to allay fears related to the slowdown in streaming growth. If the company can convince markets that its long-term subscriber growth outlook is intact, we could see some upwards price action after the earnings release.

Buy DIS Stock at eToro from just $50 Now!