Direct Line Insurance Group Share Price Forecast August 2021 – Time to Buy DLG?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Shares of British insurance company Direct Line Insurance Group are in the red today at the time of writing after the group released information on how the year has been impacting its financial results. With key figures like grow written premium taking a slight hit, many investors are questioning whether this is the right time to pick up DLG shares.

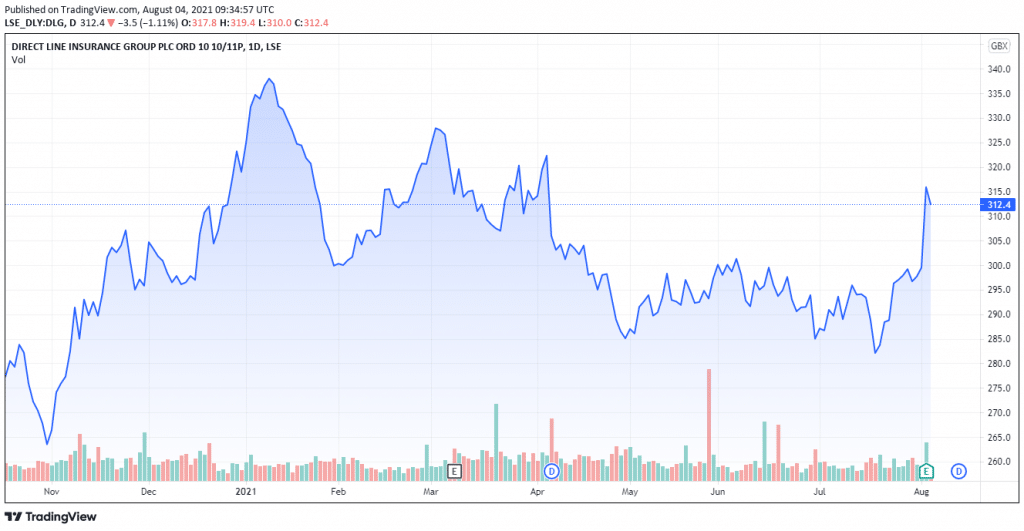

Direct Line Insurance Group – Technical Analysis

According to the financial statement released by Direct Line Insurance Group, the company’s market cap is at £4.001 billion with total assets worth £8.493 billion. Revenue for 2020 was at £3.32 billion with a profit margin of 10.57%. At the time of writing (August 4th 08:31 UTC+1), RMG shares are valued at £314.2 with a downtrend of -0.54%.

Oscillators for Direct Line Insurance Group such as Average Directional Index (14)(19.0), Awesome Oscillator(10.6), Relative Strength Index (14)(69.8) and Stochastic %K (14, 3, 3)(89) are pointing towards neutral. Moving averages such as Exponential Moving Average (100)(297.8), Simple Moving Average (100)(298.1), Exponential Moving Average (200)(299.2) and Simple Moving Average (200)(302.0) are pointing towards buying.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Recent Developments

There is quite an upheaval in the motor insurance market with the number of claims plummetting thanks to the Pandemic and the UK’s first lockdown in the spring of 2020. Other big motor insurers started offering a partial refund of premiums to customers. Prices across the industry were pushed lower for consumers as companies shared the benefit of lower claims. This drove the cost of motor insurance in the UK to a 5 year low.

The Bromley-headquartered Insurance company recently released financial figures that describe its 2021 financial situation. The company’s operating profit increased to £369.9 million in H1 2021, which is a 39.6% increase from H1 2020s £369.9 million. Profits before tax increased by 10.5% while the combined operating ratio dropped to 84.2%. The Gross written premium for the company has decreased by 1.5% to £1.556.5 million.

According to its CEO Penny James, these figures are a testament to the company’s diversified business model. Direct Line Insurance Group has made significant progress on its strategic transformation during the first half of 2021. The company’s commercial, rescue and home units have exceeded performance expectations.

Direct Line Insurance Group has also declared a 7.6 pence per share interim dividend which is a 2.7% increase from 2020. The second £50 million tranche which is part of the £100 million share buyback programme announced earlier will be launched by the company. Other factors such as reduction in new drivers, fewer new car sales and a decreasing claims frequency which were prominent during Q1 are starting to reverse in Q2.

Should You Buy DLG Shares?

Direct Line Insurance share price has experienced an absolute move of 12.5% over the past twelve months which is always a positive sign. Relatively, shares in the wider market have moved by -4.60% over the last 12 months and -13.8% over the last 6 months. For every share, it is critical for investors to examine the overall shareholder return and share price return. The TSR for Direct Line Insurance Group was 25% primarily driven by dividend payouts.

Over the last year, the company has been giving a TSR of only 17% which was below the market average. However, it is still better than the average return for the last five years which was 5%. Investors can thus look to buy this share at the moment, or at least add it to their wishlist.

Buy Direct Line Insurance Group at CedarFX, the World’s #1 trading platform!