Costco Share Price Forecast September 2021 – Time to Buy COST?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Department stores took a major hit due to the pandemic and its effect was visible in global financial markets. But as COVID-19 is getting under control in the US, retail trade is seeing a full-fledged recovery. Costco Wholesale Corporation is an ideal example of such a market opportunity. The 1983-founded company is showing positive gains for a long time and has been included in the portfolio of several market experts. Let us analyse and figure out why COST should be a part of your next investment strategy.

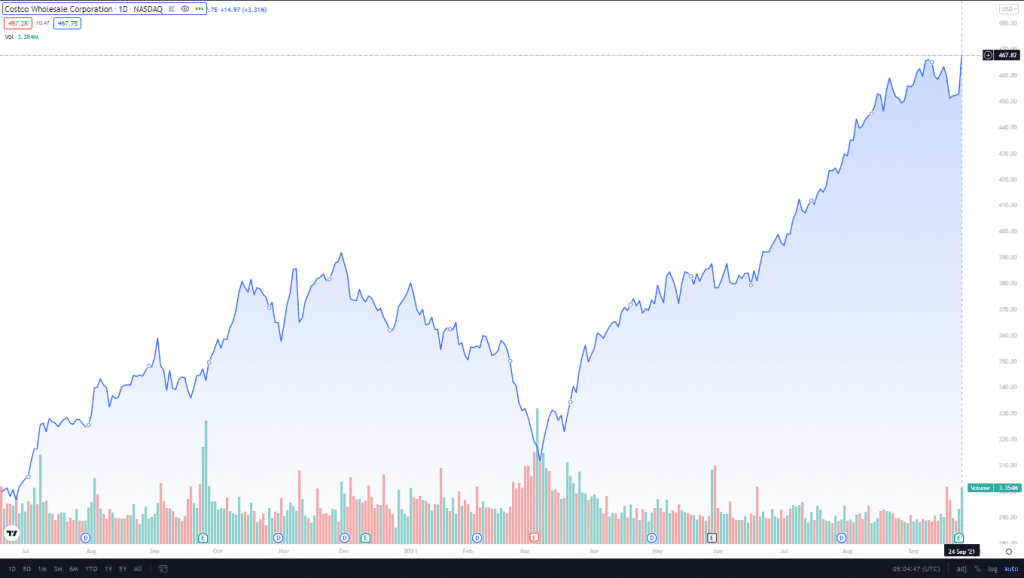

Costco Wholesale – Technical Analysis

The company managed to recover most of its losses from the time during the pandemic when Costco meant empty shelves and overflowing shopping carts. Costco was able to present strong e-commerce sales before its shareholders and investors alike. The company’s total market capitalisation is at $206.6 billion with a dividend yield of 0.68% and 11.30 EPS. The gross profit made last year by Costco comes close to $25.24 billion while the total revenue remains approximately $195.9 billion. The total debt of the company is $10.13 billion and the total assets $59.2 billion.

Yesterday, COST shares closed at $467.7 by adding 14.97 points with an uptick of 3.3%. This has brought many active investors’ attention to the company’s shares. Now it is in the strong buy zone as several moving averages and oscillators are predicting a profitable opportunity for COST. Expert’s favourite technical indicators like EMA (458.09), RSI (64.59), MACD (3.38), Average Directional Index (0.53), and SMA (457.77) is putting Costco shares in a suitable buying position for those who are interested in entering the market when it’s at its prime.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Recent Developments

Panic buying did a number on this company but the situation quickly stabilised given that COST’s Q4 fiscal results turned out to be greatly encouraging. Costco’s working model has always been a membership warehouses operator which allows it to maintain comparable sales run all year round. The only concern surrounding Costco’s performance in the days to come are increased freight and labour costs and supply chain restrictions.

According to Costco’s adjusted Q4 earnings release, COST is valued at $3.90 individually that has beaten many market experts’ expectations from the company. For this quarter, the total revenue including net sales and membership fees accumulated by Costco increased by 17.4%. Costco has managed to beat the market due to growth strategies, appropriate membership trends, positive feedback for its e-commerce business, and enhanced price management.

The warehouses’ membership operator company has seen a tremendous improvement in its overall sales and growth due to the penetration of the e-commerce business in its traditional business model. About an 11.2% increase in sales was recorded for the reported quarter due to e-commerce.

Should You Buy COST Shares?

The trend of digital transformation in the case of retail markets is far from over. Every day, a lot of recognisable retail outlets like Dollar Tree, Target, etc., are aligning their business with e-commerce to successfully adopt an Omni-channel, convenient, and popular mode of shopping for their consumers.

Costco is well-known for its capability to attract and keep paying members. It’s an age-old name within the retail sector that held its ground during the worst of the pandemic. The renewal rate for Costco members is still at 90% in the US and Canada. It’s clear as day that buying COST could not be a bad idea given the present circumstances.

Buy COST Stock at eToro for just $50 Now!