Coinbase Stock Price Down 27% Today– Time to Buy COIN Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

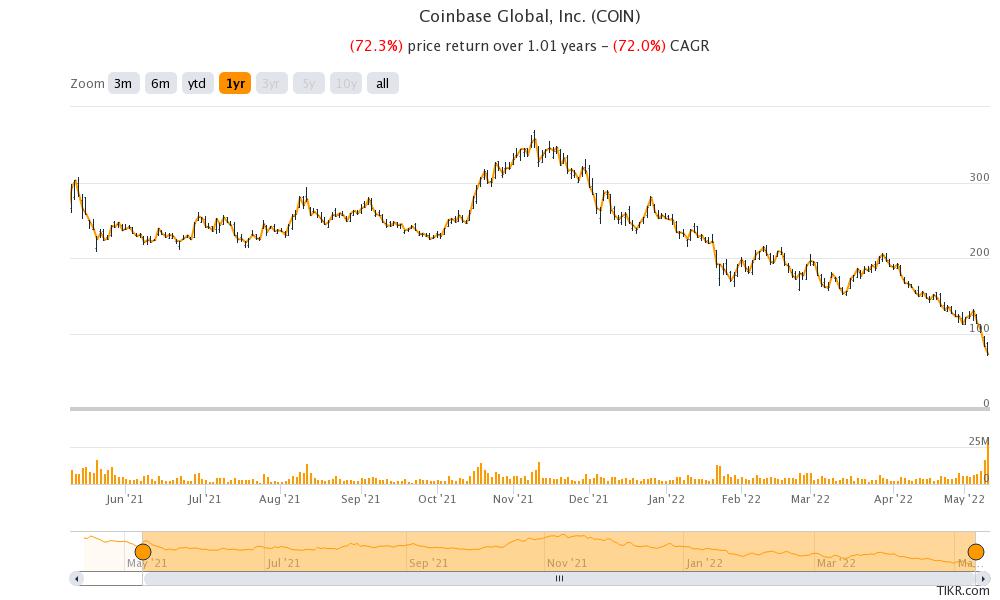

Coinbase (COIN) stock, which was anyways having a terrible year, is down almost 27% in today’s price action. The stock has been frequently hitting new 52-week lows and is down to a new low today.

Last year, COIN went public through a direct listing and kept the reference price at $250. The stock had a bumper listing and went on to hit a 52-week high of $429.54. However, it has since looked weak and while there has been brief upwards price action, the overall trend has been down. While fintech stocks, in general, have been weak, COIN stock has been particularly under pressure. What’s the forecast for Coinbase stock and is it a good buy in May 2022?

Coinbase stock recent developments

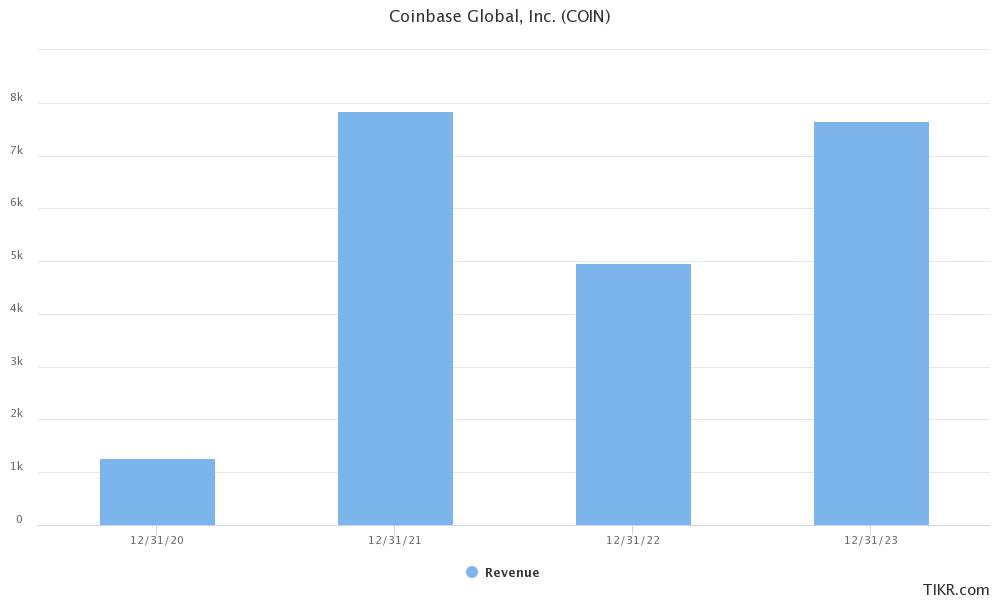

Coinbase released its first-quarter earnings yesterday. It posted revenues of $1.17 billion which was way below the $1.48 billion that analysts were expecting. The revenues were lower than what it had posted in the first quarter of 2021 and were less than half of its fourth-quarter 2021 revenues. While Coinbase had warned that its revenues would be sequentially lower in the quarter, the slowdown turned out to be far worse than markets were expecting.

68% of all retail investor accounts lose money when trading CFDs with this provider.

COIN’s earnings spooked markets

COIN reported MTUs (monthly transacting users) of 9.2 million in the quarter which was way below the 11.2 million it reported in the previous quarter. The total trading volumes plummeted to $309 billion in the quarter which was again way below the $547 billion that it reported in the previous quarter. It is the lowest trading volume for the company since it went public last year. The total assets on the platform also fell to $256 billion as compared to $278 billion at the end of December.

Coinbase asks investors to take a long-term approach

In its release, Coinbase said, “You can expect volatility in our financials, given the price cycles of the cryptocurrency industry. This doesn’t faze us, because we’ve always taken a long-term perspective on crypto adoption. We may earn a profit when revenues are high, and we may lose money when revenues are low, but our goal is to roughly operate the company at break even, smoothed out over time, for the time being. We are looking for long-term investors who believe in our mission and will hold through price cycles.”

COIN posted a net loss in the quarter

Coinbase posted a net loss of $430 million in the quarter which is its first loss since it went public. Its per-share loss of $1.98 was far worse than what analysts were expecting. The company’s CFO Alesia Hass said that COIN has been prioritizing growth and has been investing in new products.

The company said, “While we continue to invest and enhance our core investment platform, the application era of crypto is upon us, led by NFDs and decentralized finance, and we are increasingly focusing our efforts on these market opportunities.”

Coinbase expects things to get worse in the second quarter

Coinbase said that both trading volumes and MTUs to decline sequentially in the second quarter which would invariably lead to fewer revenues. The company expects subscriptions and services revenues to be similar or slightly lower in the second quarter.

For the full year 2022, COIN expects to limit its adjusted EBITDA loss to $500 million. It expects to have annual average MTUs between 5-15 million, which is similar to its previous guidance. It expects the average transaction revenues in the year to fall below pre-2021 levels.

The company said, “Year-to-date, ATRPU is trending towards 2019 levels. These lower levels reflect (1) softer crypto market conditions and (2) growth in users engaging in non-invest products (notably staking) that generate Subscription and Services revenue.”

COIN stock forecast

While COIN stock is plummeting today, many analysts see the crash as an excellent buying opportunity. Bank of America reiterated the stock as a buy despite the disappointing earnings.

MoffettNathanson’s Lisa Ellis also finds the stock attractive while warning of near-term headwinds. “Certainly, during these next couple of quarters where they’re going through a downturn in the crypto market, they’re actively investing to diversify their business away from the volatile trading business,” said Ellis. She added, “And in our view, that’s essential both for the stability and the stock but also just for diversification of the business more broadly that we see that going forward.”

Analysts advise buying Coinbase stock after the crash

JMP analyst Devin Ryan also sees the stock as an attractive long-term buy. He said, “while the market backdrop has presented a challenge to start the year, we remain bullish on the long-term outlook for Coinbase given our ongoing expectation that the crypto economy will continue to develop at a rapid pace (driving the addressable market higher), adoption trends will remain healthy across customer segments, and Coinbase can remain an intermediary around access, product, and service for each.”

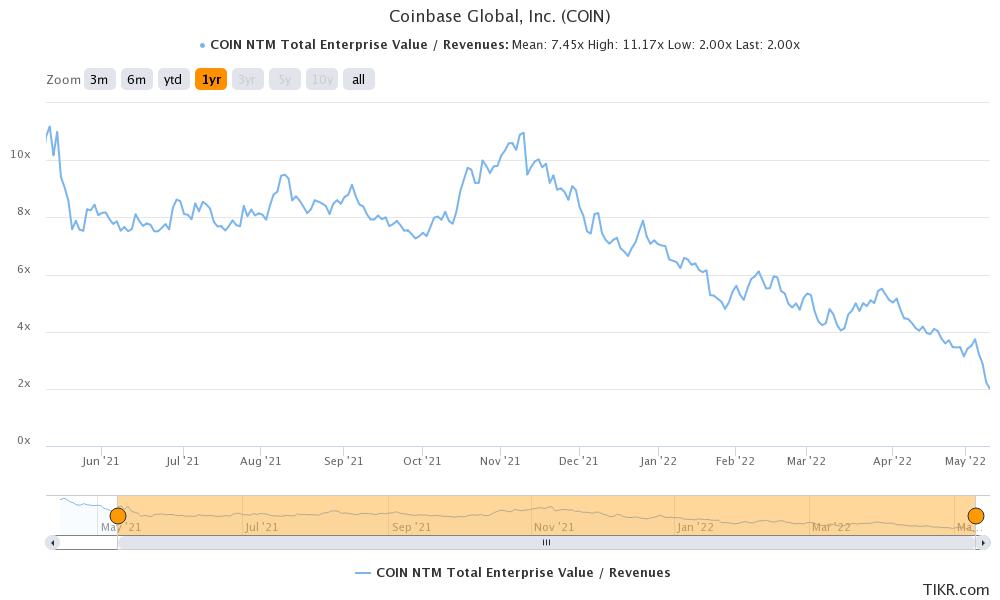

Ryan added, “With $6B in cash, shares are currently trading at ~2.1x our 2023 revenue estimate, which we believe represents a particularly compelling value if our thesis plays out around market expansion.” BTIG also said that concerns over COIN’s solvency are overblown.

Concerns over COIN’s bankruptcy

In its SEC filing, Coinbase said that its users could risk losing their assets on the platform in case the company went bankrupt. It said, “Because custodially held crypto assets may be considered to be the property of a bankruptcy estate, in the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors.”

However, COIN’s CEO Brian Armstrong said that the new disclosure is due to an SEC rule. He added, “This disclosure makes sense in that these legal protections have not been tested in court for crypto assets specifically, and it is possible, however unlikely, that a court would decide to consider customer assets as part of the company in bankruptcy proceedings even if it harmed consumers.”

Should you buy Coinbase stock

COIN stock is getting punished for the dismal earnings but the sell-off looks a bit stretched. Coinbase stock is looking quite cheap at these levels. While there are short-term headwinds on both the topline and bottomline, COIN is among the best ways to play digital assets.

Buy COIN Stock at eToro from just $50 Now!