Coinbase Stock Down 10% in January – Time to Buy COIN Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Coinbase is down 10% so far this month as weakness in the cryptocurrency market has spilled over to 2022 with the price of Bitcoin remaining almost 38% below its 52-week high as of this morning.

According to data from CoinMarketCap, the market capitalization of cryptocurrencies as a whole has declined nearly 9% since the year started as macroeconomic conditions are expected to tighten.

During the same period, for example, US Treasury yields have climbed to their highest level since the pandemic started with 10-year yields finishing last week at 1.792%.

For Coinbase, weakness in the price of cryptocurrencies typically results in a deterioration of its top-line performance as the company generates most of its revenues via transaction-based income.

On 12 January, the company announced the acquisition of FairX, a US-based crypto derivatives platform to gain access to the growing market for options and futures of the most popular crypto assets.

According to the company, the acquisition will allow it to offer these products to US traders and investors. The financial terms of the deal or its prospects were not disclosed. The deal is expected to be settled within the first fiscal quarter of 2022.

What could be expected from this crypto stock for what remains of the year? In this article, I’ll be assessing the price action and fundamentals of COIN stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

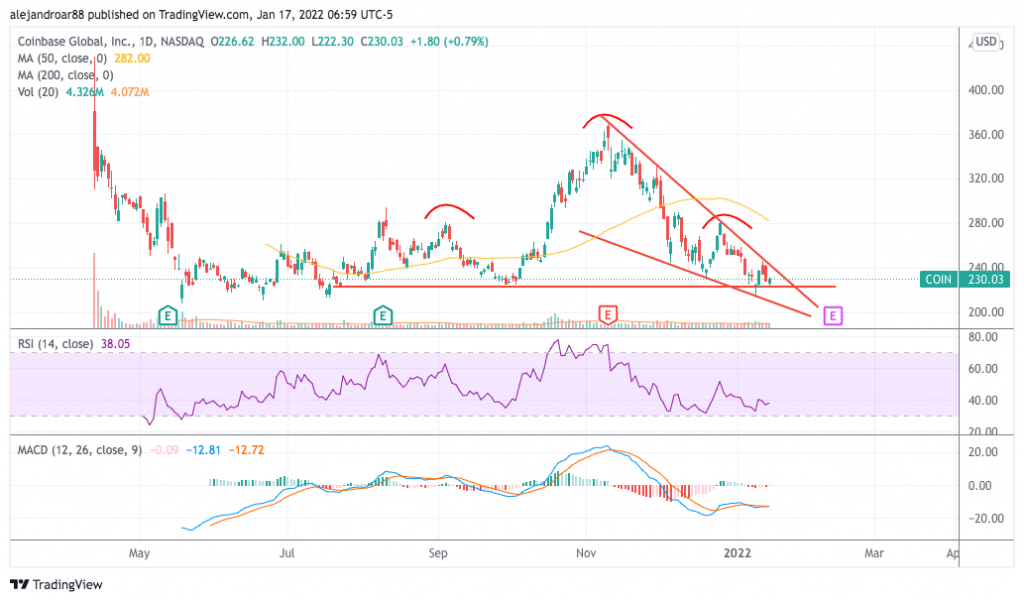

Coinbase Stock – Technical Analysis

The price of Coinbase stock has been on a steady downtrend since early November last year back when the price of Bitcoin (BTC) was surging to all-time highs. However, the subsequent weakness in the crypto market deteriorated the valuation of the cryptocurrency exchange and has pushed its price to its lowest level since September-October 2021.

As a result of this decline, a falling wedge pattern has been formed. This pattern is typically considered bullish as long as the price breaks above the upper bound of the setup.

However, there could be another pattern in play. The chart above shows that a head and shoulders pattern may have formed following the stock’s price action since mid-2021 with the neckline standing at $224 per share.

Moving forward, two scenarios could play out for Coinbase stock:

- A break above the upper trend line of the falling wedge occurs that prompts a sustained uptrend. In that case, the first target for Coinbase could be set at around $280 per share – the stock’s 50-day simple moving average.

- A break below the H&S’s neckline occurs and the stock declines to the low 200s for a total downside risk of approximately 10% to 15%.

Momentum oscillators are currently favoring a bearish outlook as the Relative Strength Index (RSI) is standing at 38 (bearish) while the MACD is neck-deep into negative territory.

Coinbase Stock – Fundamental Analysis

Coinbase’s revenues have been rising at an incredibly fast pace in the past couple of years moving from $483 million in 2019 to $5.4 billion in the past twelve months as the market capitalization of crypto assets surged during the pandemic.

The accommodative monetary policy adopted by the largest central banks across the world to contain the impact of the health crisis on the financial markets has contributed to pushing the valuation of these assets higher as investors anticipated – accurately – that inflation would surge as a result of these measures.

The company’s net income has also jumped. Back in 2019, Coinbase reported GAAP net losses of $30 million while the company produced $3 billion in net earnings in the past 12 months resulting in a net margin of 56%.

Meanwhile, free cash flows in the past twelve months more than tripled compared to 2020 at $9.9 billion.

The company has a strong balance sheet comprised of $6.3 billion in cash reserves and zero long-term debt.

For 2022, analysts are expecting to see sales landing at $7.25 billion resulting in an expected 2.5% drop compared to the figure the firm is expected to report for the full 2021 fiscal year.

Based on the company’s most recent profit and cash flow margins, Coinbase could produce $11 billion in free cash flows this year and around $3.6 billion in profits.

This results in a forward P/E ratio of around 14x and a forward P/FCF ratio of 5x. These multiples are fairly conservative and seem to be reflecting the market’s expectations for the firm and for the crypto market as a whole.

It appears that some sort of decline in the valuation of cryptocurrencies is expected to occur in 2022. If this is not the case and the price of Bitcoin and other tokens surges during the year, chances are that Coinbase’s valuation will experience a significant jump as the market’s pessimistic outlook will be invalidated.

Buy COIN Stock at eToro with 0% Commission Now!