China: How Investors Can Profit in Xi’s ‘Common Prosperity’ Era

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

China’s President Xi Jinping is looking to be endorsed for a third term next year at the five-yearly party congress and he doesn’t want anything to upset his plans – for China and himself.

Investors in the west have watched with some anxiety the rollout of what looked like a plan to curb the power of big tech. Alarm grew as the reforms spread to other industries, most notably the private education sector, which was in effect band from making profits from tutoring and using foreign teachers, effectively killing their business models.

Since then the party policymakers have sought to rein in debt and make progress on weaning the economy off fossil fuels, notably coal which was continue to power three quarters of the economy.

After the initial forays to curtail monopoly practices and the economy’s voracious appetite for debt-fuelled property development, the guiding principle of the reforms was revealed – achieving the goal of ‘common prosperity’, as the party seeks to guard its legitimacy by arresting growing inequality and ultimately reversing the gap between rich and poor. The object is to grow the middle class, which is not a new aim, but it is the explicit targeting of worsening inequality that is new.

Getting rich is no longer seen as performing a national economic goal. Instead the planners want to see the development of an “olive income distribution”, with the bulging middle made up of a thriving middle class.

Are Xi’s reforms going too far too fast?

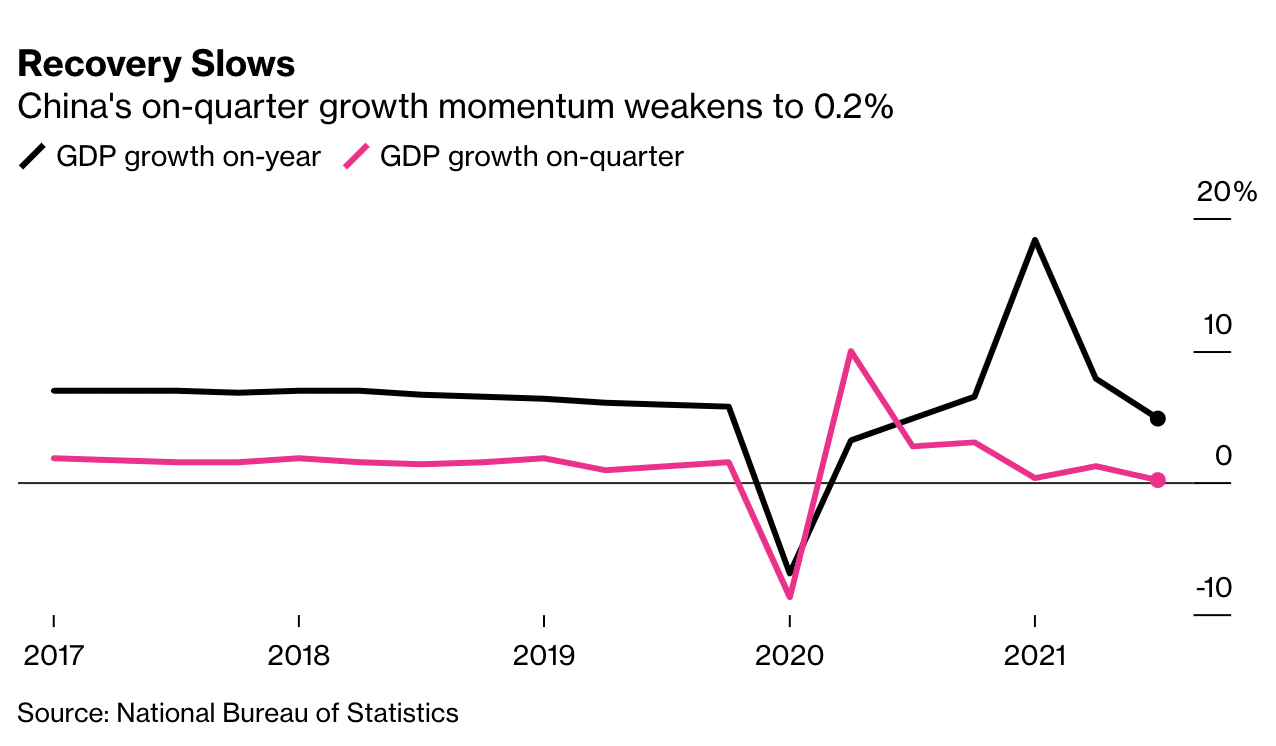

Yesterday’s headline GDP data shows the economy is decelerating, at 4.9% compared to 5.1% in the second quarter. Still, the economy since the start of the year has grown 9.8%, well ahead of the 6% target.

Chinese officials were putting a positive spin on the data.

“The Chinese economy has maintained recovery momentum in the first three quarters with progress in structural adjustment and high quality development,” said a spokesperson for the National Bureau of Statistics.

Nevertheless, there are signs of trouble ahead for the economy, so the question arise, will the reforms be slowed down so as not to hurt hurt consumers and small-time investors?

For sure, if inflation becomes embedded or the Evergrande debacle becomes uncontainable, then the political risks – not to mention the economic ones – start to rise considerably for Xi.

Investors got a clearer idea of how policy may proceed in a fuller version of a speech by Xi published in the premier theoretical journal of the party.

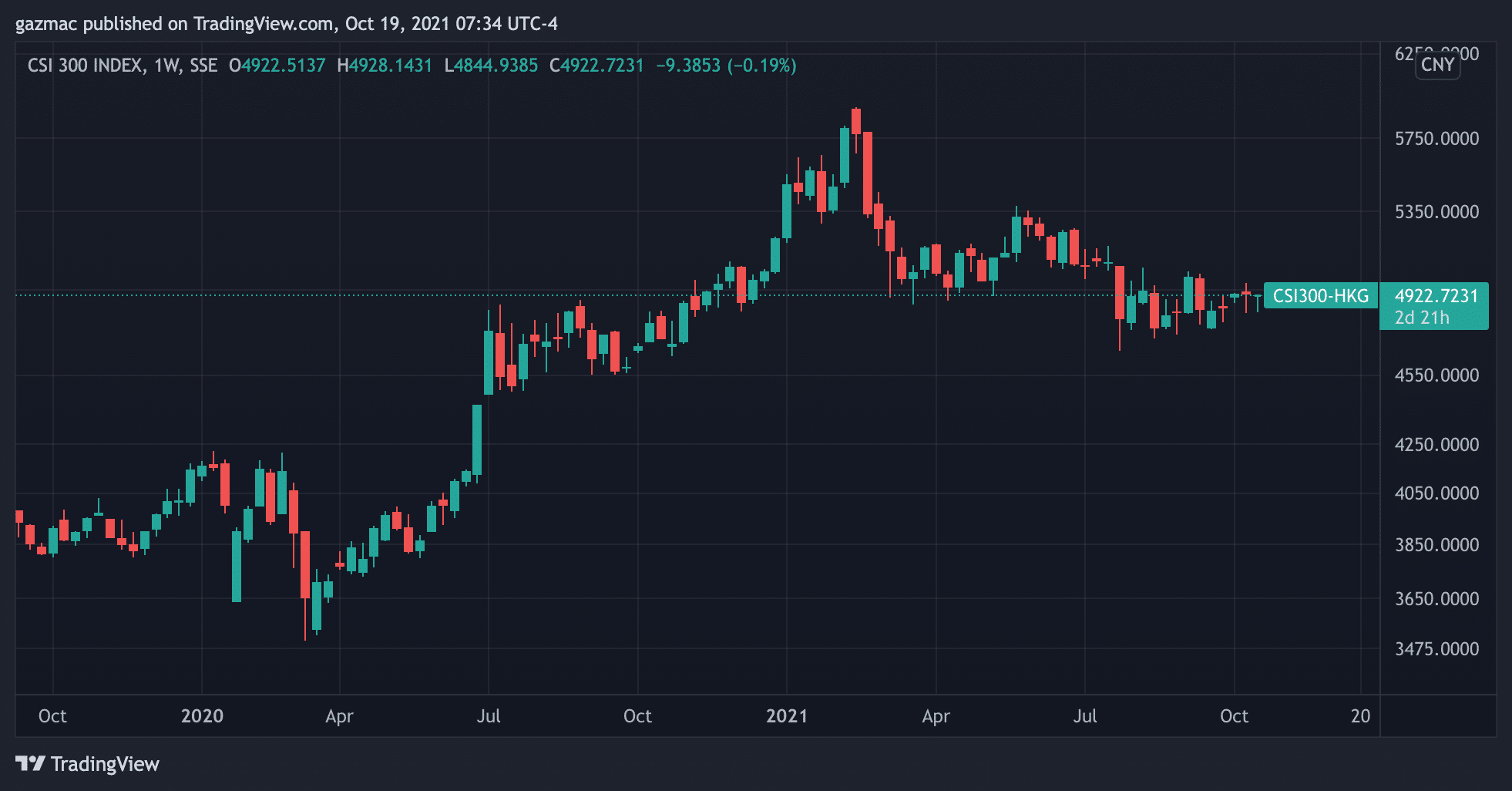

The CSI 300 index of the top 300 stocks weighted by capitalisation traded on the Shanghai Stock Exchange and the Shenzhen Stock Exchange, is the worst performing emerging markets index this year.

The speech, entitled To Firmly Drive Common Prosperity, was made to the Central Financial and Economic Affairs Commission meeting on 17 August 2021.

It is worth reading the speech, as China watchers believe it is the most detailed exposition of what common prosperity means and how the socio-economic goals will be achieved.

Here are some of the key passages from XI’s speech:

“At present, income inequality is a prominent issue around the globe. The rich and the poor in some countries are polarised with the collapse of the middle class. This has led to social disintegration, political polarisation, and rampant populism — indeed, the lessons [for us] are profound! Our country must resolutely guard against polarisation, drive common prosperity, and maintain social harmony and stability.”

“We must study in-depth the objectives of the different stages [of the pursuit for common prosperity] and advance in phases. By the end of the 14th Five-Year Plan [2021-2025], common prosperity for the entire population will have taken a solid step forward, and the gap between the income and actual consumption levels of residents will have been gradually reduced. By 2035, common prosperity for the entire population will have made more visible and substantial progress, and [access to] basic public services will have been equalised. By the middle of this century, common prosperity for the entire population will be basically achieved, and the gap between income and consumption levels of residents will have been narrowed to a reasonable range.”

“We must prevent social stratification, open up channels for upward mobility, create opportunities for more people to become rich, form a development environment with participation from everyone, and avoid [the phenomena of] ‘involution’ and ‘lying flat’ [slang for turning your back on the hyper competitive education system and jobs market]

“While giving full play to the important role of the public sector economy in driving common prosperity, we must also promote the healthy development of the non-public sector economy and the healthy growth of its members. While we should allow some people to get rich first, it should be emphasised that those who become rich first [shall] lead and assist those who are not yet rich.”

“Even if we reach a higher level of development and acquire stronger financial resources in the future, we should not set aims that are excessively high, and/or provide excessive guarantees. We must resolutely prevent [ourselves] from falling into the trap of nurturing lazy people through ‘welfarism’.”

“Adhere to a gradual and orderly process. Common prosperity is a long-term goal that requires a process and cannot be achieved overnight. We must fully consider the long-term, arduous and complex nature of the enterprise. We must do it well; it can neither wait nor be rushed.”

Xi then moves on to explain how the broad principles of common prosperity will be implemented. He says there are six key levers to attain the goals he sets out in the first half of his speech.

Explainer: what Xi’s six areas of focus mean

First, we must improve the balance, coordination and inclusiveness of development.

The key word Xi repeats in this passage is ‘balance’ – with regional balance very much in mind, for example through the fuller economic integration of the Yangtzee river delta region and improve”transfer payments” to reduce regional differences

Second, we must focus efforts on expanding the size of the middle-income groups.

Here, Xi states the aim is to “push low-income earners into the middle-income bracket”. We see an emphasis on higher education, skills training and improving the business environment for small and medium-sized enterprises that have grown through entrepreneurialism. Importantly, he also speaks of reforming the migrant worker system to make it easier for workers from the countryside to move to the cities and stay there legally.

Third, we must promote the equalisation of basic public services.

Here Xi fleshes out the references in the first half of the speech to “high-quality” development, with an emphasis on improving human capital by “raising the education level” as well as improving the country’s less than generous basic income guarantees, and improving pensions and medical services. There is also a mention of the need for housing “for living in not for speculation”

Fourth, We must strengthen the regulation and adjustment of high incomes.

Notably Xi’s first point is to protect “income that is legitimately acquired” before moving on to the need to regulate “excessive income” and “improve the personal income tax system and regulate the management of income from capital”. Protection of property rights is offset by the need to “resolutely oppose the disorderly expansion of capital, draw up a negative list for market access for sensitive areas, and strengthen anti-monopoly regulation and supervision”.

Higher taxes are coming for those on higher incomes, owners of capital and property investors. Under the definition of “illegal incomes” falls “insider trading”, “stock market manipulation”, “financial fraud” and “tax evasion”.

Fifth, we must promote common prosperity in the spiritual [and moral] lives of the people.

The shortest section, Xi is talking about maintaining social control and guarding against instability. “We must strengthen public opinion guidance on driving common prosperity to provide a favourable public opinion environment,” says Xi.

Sixth, we must drive common prosperity among farmers and in rural areas.

Much of China’s poverty is hidden away in the countryside. The gap between rural and urban areas has long worried policymakers. Around 40% of China’s 1.4 billion population have an average income of just $155 (1,000 yuan) a month. The goals of common prosperity “should be expedited” says XI, but at the same time says no quantitative targets should be set, as was done in the “poverty eradication battle”.

But of course a main locus of poverty in China is in fact in the countryside, so the thinking here is muddle to say the least. This contradiction is surely a part of the “primary contraction” Xi refers to at the start of his speech, which is presumably a reference to the divide between rich and poor. The apparent muddle here, reflects the intractable nature of the rural development problem.

Real estate debt clampdown to continue – but is Evergrande contained?

At this stage of the common prosperity implementation plan property speculation is in the eye of the storm. There is no reason to expect regulators and policymakers to step back from curtailing debt issuance to the real estate sector.

Zou Lan, head of the People Bank of China’s financial markets department believes the Evergrande fallout is containable: “[Evergrande] had poor management, failed to run its businesses cautiously according to changes in market conditions and expanded blindly. Evergrande’s creditors are scattered and individual banks’ exposure is small — the risk of spillover to the financial industry is controllable.”

We can assume that the reforms in the property sector will continue. New loans to the sector had in any case been falling since 2016, from 50% to about 15% now. The government has provided some stimulus to the economy, but has done this by loosening capital ratios for banks, while attempting to direct new investment into the “real economy” and way from speculative property development.

The danger zone for Xi is the energy sector, where rolling blackouts have become the norm in some regions as the global energy crisis hits the country, further exacerbated by by price caps and, in retrospect, overzealous reductions in fossil fuel power generation.

Energy-intensive industries have had to cut production, power stations have stopped generating as price caps made generation unprofitable, and consumers faced cuts in supply. The last thing Xi will want to see is people not being able to heat their homes this winter, so the authorities have now ordered coal power stations to maximise production. However, floods in the coal regions of Inner Mongolia and Shanxi are not helping to effect this about-turn.

China has ordered state bodies to secure energy imports “at all costs”, so liquified natural gas tankers will be adding to the queues at the country’s congested ports.

Premier Li Keqiang signalled a softening in the carbon neutral targets in a sign of the flexibility the authorities are willing to apply to the rollout of new policies.

“Energy security should be the premise on which a modern energy system is built, and the capacity for energy self-supply should be enhanced,” he said. The target of carbon neutrality by 2060 should be approached in a “sound and well-paced” emphasised Li.

Similar flexibility will be in evidence as far as the overall common prosperity reforms are concerned and the imperative of keeping economic growth on track.

Where to invest for profits in China’s common prosperity period

Investors fears about the threat to private property in the country are overblown. After all Goldman Sachs was recently allowed to take 100% ownership of its joint venture in the country.

Reading between the lines of the reforms reveals a cognisance of the need to tread carefully and in a “gradual and orderly” fashion, with the flexibility to slow down when required so as not to scare off entrepreneurship or foreign investment.

Common prosperity is not going to be a sprint but its target of expanding the middle class holds out the possibility of increasing consumption as the driver of the economy as opposed to primarily exports as is the case today. That means sectors investors should be looking for exposure in will be areas such as health and medical services, domestic-focused consumer goods and financial services.

Education spending is set to rise but investors may find this a difficult arena for foreign capital given the recent clampdown on tutoring and the stated aim of driving down the cost of education services which might pressure margins.

China wants to weaken monopolies in big tech, and that will at some point lead to a favourable entry point for investors in the relevant stocks such as Alibaba and Tencent, but probably by investing in the Hong Kong-listed H shares of companies incorporated in mainland China, as opposed to the ADRs trading on the New York Stock Exchange.

However, in its overarching aim of maintaining the legitimacy of the Chinese Communist Party there are still clear and present dangers that investors will need to keep in mind.

Matthew Gertken, geopolitical strategist at BCA Research, summaries the issues Xi must contend with.

“On the current trajectory there is a clear and present danger of widening illiquidity, collapsing property prices, credit crunch, financial and economic crisis, and sociopolitical problems. These outcomes may ultimately be unavoidable, but first the regime will moderate policy to try to avoid them,” he explained.