Carnival stock is down 27% in July – Time to buy CCL stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The stock of cruise line operator Carnival Corporation (CCL) is down 27% so far in July including this morning sharp 7.6% downtick, with the stock currently trading at $19.35 per share.

A surge in cases in the United Kingdom, the United States, and other corners of the developed world are instilling fear among market participants about a potential prolongation of no-sail orders – a situation that could threaten to derail the prospect of a recovery for cruise lines in 2021.

However, now that vaccines are increasingly available and being progressively rolled out across the world, could this be an opportunity to buy CCL stock at a relatively cheap price? In the following article, I take a look at the stock’s fundamentals to see if that might be true while also analyzing the latest price action to outline potential areas of support for a short-term bounce.

67% of all retail investor accounts lose money when trading CFDs with this provider.

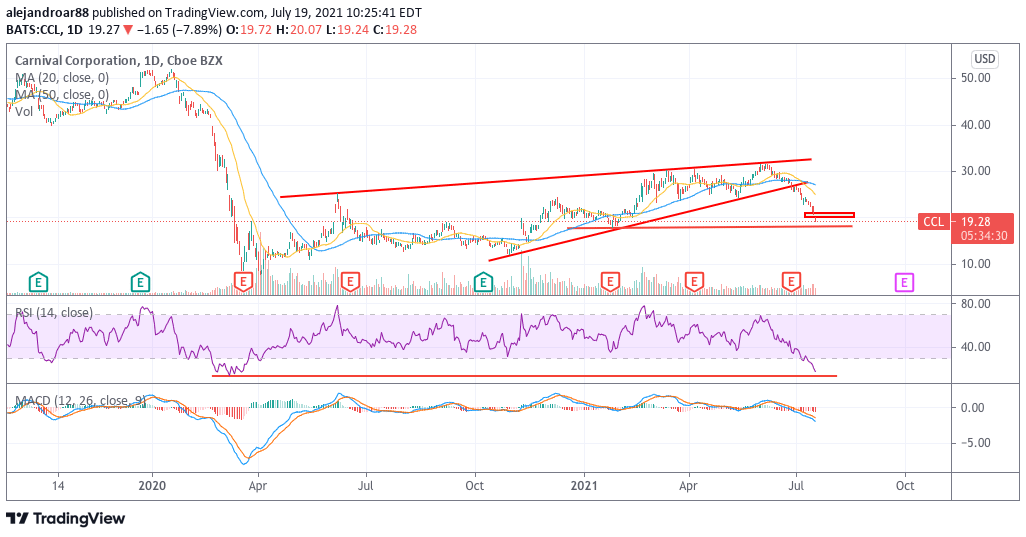

Carnival stock – technical analysis

The chart above shows the severity of the decline that Carnival stock has experienced in the past month and a half, with the stock losing nearly 40% of its value since its late June peak of $31.5 per share.

Such a decline has been the result of increasing concerns about the impact that prolonged no-sail orders could have on Carnival’s cash burn while the company has been conducting a series of stock repurchases that could prove to be inconvenient for its liquidity position if the pandemic-prompted revenue downturn endures for longer than expected.

As indicated by the chart, Carnival stock has already broken below a long-dated trend line support while the next support area is found at the $18 level for a 7.2% downside risk.

Notably, the Relative Strength Index (RSI) is currently posting its worst oversold reading since the February-March pandemic crash, which shows the degree of concern that market participants are exhibiting about the firm’s outlook.

In this regard, even though this selling spree could already be approaching a bottom at that $18 level, the strong reversal in the stock’s momentum indicated by such a low reading in the RSI could point to sustained weakness in the stock price moving forward unless the current negative backdrop changes.

Carnival stock – fundamental analysis

By the end of the second quarter of its 2021 fiscal year, Carnival reported a net loss of $2.1 billion along with a better-than-expected cash burn during the first semester of the year.

The average monthly cash burn during the first semester was $500 million and, based on the current situation, it could be expected that Carnival will continue to burn cash at that rate or worst, resulting in $6 billion in cash possibly being disposed of during the second semester of the year.

Even though the company ended this first semester of 2021 with $9.3 billion in cash and equivalents, it is important to note that Carnival has recently launched a tender offer to repurchase $2 billion of its 11.5% 2023 Senior Secured Notes while soliciting a modification in the terms of the loan.

Such an offer, which will be expiring on 2 August, could drain the company’s reserves at a critical juncture as the pandemic could prompt governments to maintain their current restrictions for longer than expected.

Based on these developments, the outlook for Carnival is fairly uncertain and market participants seem to be acknowledging the risks that the company is facing in case it is unable to trim its cash burn significantly in the following months as it would be facing the downturn with lower cash reserves.

It is important to note that analysts’ estimates point to a full-blown recovery in Carnival’s sales by the end of 2022, with sales projected to land at $17.8 billion then along with forecasted annual earnings per share of $0.36 in 2022 and $1.77 by 2023.

At its current price, the stock would be trading at around one time its forecasted sales for 2022 and 49 times its 2022 forecasted EPS, which is an overly optimistic multiple based on the risks the company is currently facing. Meanwhile, Carnival is currently holding around $27 billion in debt on assets of $46 billion excluding cash and $44 billion excluding intangibles and goodwill.

Moreover, according to the firm’s 2020 annual report, a total of around $6.6 billion in debt is expected to mature this year including multiple bank loans and export credit facilities. All in all, the tangible book value of Carnival is between $6 to $7 per share upon deducting cash and intangibles. That leaves plenty of room for further downside if conditions continue to deteriorate for the firm.

Buy Stocks at Vindax FX, the World’s #1 trading platform!