Carnival Stock Down 8% in October – Time to Buy CCL Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

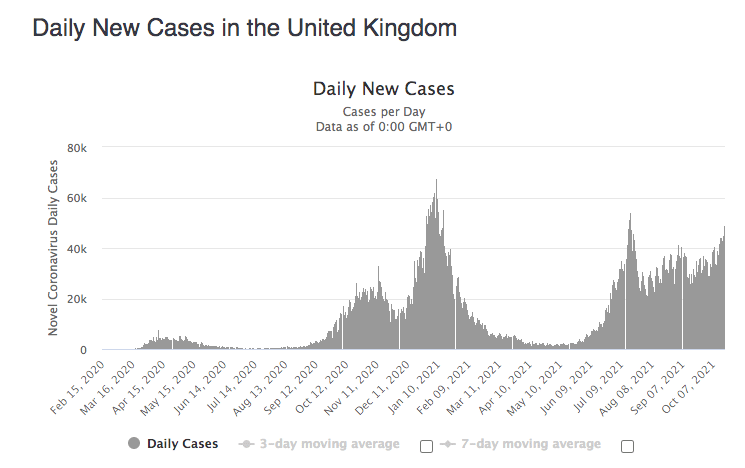

The price of Carnival stock is down 8% so far in October following news about an unexpected increase in the number of COVID-19 cases in countries such as the United Kingdom – which has vaccinated a large percentage of its population.

According to experts, multiple causes could explain this sudden uptick in the number of daily infections including weaker protection from vaccines months after they were administered and the potential appearance of a descendent of the Delta variant.

Other reasons would include the United Kingdom’s hesitation to vaccinate its youngest cohort and more flexibility in preventive protocols by vaccinated individuals such as wearing masks and practicing safe distancing.

For companies within the travel sector like Carnival Corp (CCL), these kinds of developments are considered dangerous by investors as they could prolong the firm’s pains in the scenario that countries reintroduce travel restrictions.

What is the outlook for Carnival stock following this monthly downtick? In the following article, I’ll be assessing the price action and fundamentals of the business to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Carnival Stock – Technical Analysis

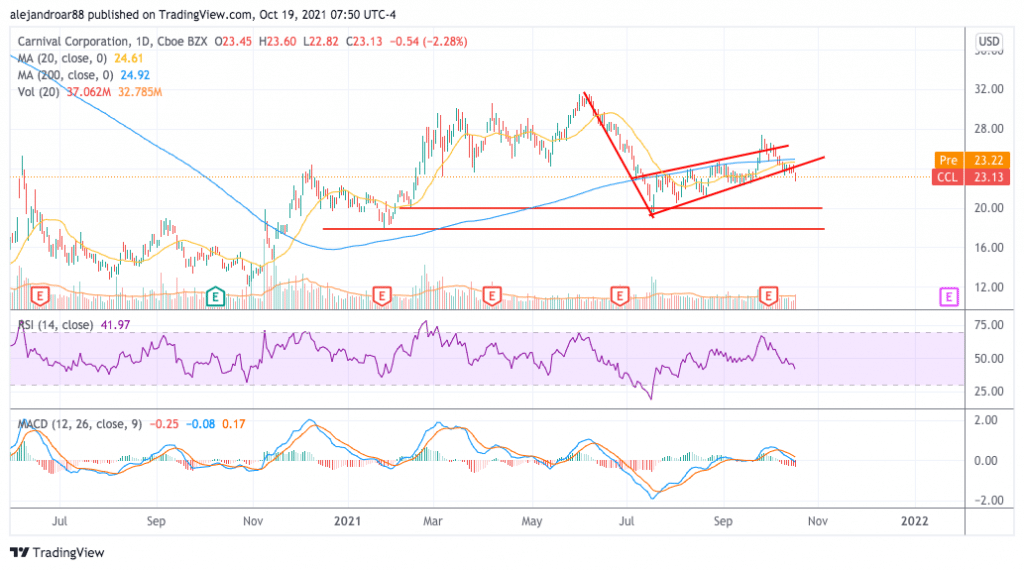

Last month, we highlighted the existence of a bull flag pattern that supported a bullish outlook for Carnival stock as long as the price broke above this formation. Even though a break did occur on 27 September, bulls failed to hold their ground and bears took over the price action on the days that followed as reflected this October decline.

It seems that concerns about the situation in the United Kingdom and the possibility that this scenario can be replicated in other latitudes are weighing on investors’ sentiment toward travel stocks.

As a result, the price of CCL stock has now broken below the flag – a move that has effectively invalidated the pattern. This break occurred just yesterday during a session that saw above-average trading volumes.

Momentum oscillators are now pointing to a bearish outlook for Carnival as the Relative Strength Index (RSI) just dipped below the 50 mark – currently standing at 42 – while the MACD has crossed below the signal line – typically a sell signal – and this move is being accompanied by steadily increasing negative histogram readings.

Moreover, Carnival stock has broken below its short-term moving averages and it is now trading 7% below its 200-day moving average – a sign of mid-term weakness.

All things considered, the outlook for Carnival stock has turned bearish amid the impact that another spike in the number of daily cases of COVID in different corners of the world could have on the firm’s recovery.

Carnival Stock – Fundamental Analysis

Carnival announced only a few days ago that its Princess unit now plans to operate at 79% of its capacity by the end of 2021 upon resuming operations for multiple vessels including the Crown Princess, Island Princess, and Royal Princess.

Earlier this month, the company said that it should also be able to ramp up its operating capacity to 90% for its US-based vessels by February 2022 while the management stated that the company should be able to return to pre-pandemic levels in terms of bookings during the first semester of 2022.

These announcements did not take into account the possibility of prolonged restrictions from multiple countries resulting from subsequent virus waves and market participants may have decided to adjust their forecasts for the firm as a result of what is happening in the United Kingdom.

That said, this month the company managed to secure a $2.3 billion term loan facility in an operation that will effectively save the business over $135 million in interest expenditures. The savings would come as a result of the repayment of senior secured notes expiring in 2023 that carried an 11.5% interest rate.

Carnival’s debt burden has been a major concern among analysts as higher interest expenditures are expected to weigh on the firm’s profit-generation capacity once its top-line results jump back to pre-pandemic levels.

Last year, interest expenses climbed to $895 million – up from $206 million paid by the firm the year before – while Carnival paid $1.25 billion in interest expenditures during the nine months ended on 31 August 2021.

Using a run rate of these first nine months, we could anticipate that Carnival may pay around $1.6 billion in interest this year. If we deduct the $135 million it will save as a result of this recent refinancing operation, total disbursements would be approximately $1.45 billion for 2022.

In the scenario that sales climb back to pre-pandemic levels, such a burden would depress the firm’s net earnings from around $3 billion reported in 2019 to approximately $1.8 billion.

Using that estimate and CCL’s 1.08 billion total diluted outstanding shares, this results in a forward post-pandemic P/E ratio of 14 or so. Considering the risks that the company continues to face and the elevated debt burden that it still has, this multiple seems rather elevated.

With that in mind, further declines in the price of Carnival stock may be justified if market participants believe that the firm will experience further woes as a result of situations such as the one seen in the United Kingdom.

Buy CCL Stock at eToro with 0% Commission Now!