Boeing Share Price Forecast July 2021 – Good Time to Buy?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The performance of Boeing stock so far in July has been muted as the issue has managed to trim some of the losses it saw earlier this month following the appointment of a new Chief Financial Officer (CFO) and some other developments.

Meanwhile, the aircraft manufacturer has announced that it will be publishing its financial results covering the second quarter of 2021 on 28 July, which makes this a good opportunity to take a closer look at what the market is expecting from Boeing for this quarterly report.

As the world progressively steps out of the pandemic, could this be a good opportunity to buy Boeing? Or is this company poised to underperform the market for longer amid the significant deterioration of its fundamentals? Join me in the following Boeing share price forecast to possibly answer these questions.

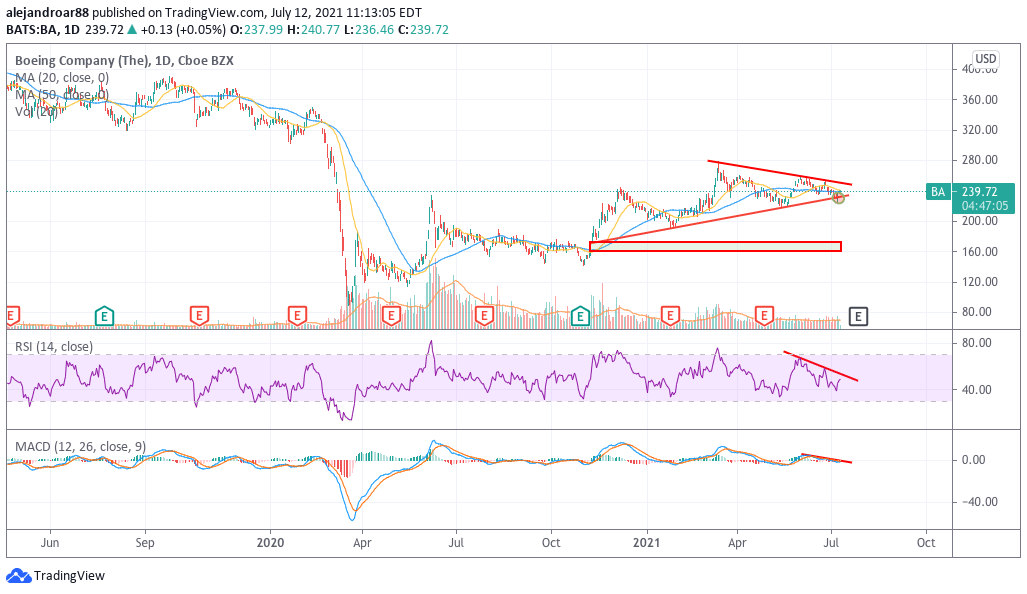

Boeing (BA) stock – technical analysis

Boeing’s momentum has been fairly stalled lately, with the stock apparently undergoing a phase of consolidation as investors await more data that clarifies where the business might be heading now that the virus crisis seems to be coming to an end.

On 8 July, the price unexpectedly broke below the lower trend line shown in the chart but bulls showed up during intraday action and managed to overturn those early losses to push the stock 2.2% higher during what was a high-volume trading session.

Volumes might be serving as a tell that this long-dated trend line is one that market participants are watching closely and that could indicate the potential for further upside for Boeing ahead of its earnings report.

However, before this bounce starts to become a promising one, momentum readings must overturn their current downtrends. Until that happens the outlook for Boeing shares remains neutral as the stock could continue to trade range-bound until the company releases its quarterly report.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Boeing (BA) stock – fundamental analysis

According to data from Seeking Alpha, revenues for Boeing’s Q2 2021 are expected to land at $18 billion or 52.4% higher than top-line results during the same period a year ago. That said, the range of estimates is fairly ample for the aircraft manufacturer, going from $16 to $19.5 billion as per the 13 analysts who have currently provided their forecasts.

Meanwhile, the consensus estimate for Boeing’s earnings per share stands at minus $0.60, with the lowest forecast putting the firm’s bottom-line profitability at minus $1.25 and the highest at positive $0.13.

These fairly ample ranges for both the firm’s revenues and profitability result from the uncertainty caused by the virus situation, which has prompted the management to abstain from providing any sort of guidance for the business until future prospects become clearer.

Before the pandemic stroked, Boeing sales were a bit erratic, moving from $94 billion in 2017 to $101.1 billion in 2018 to then drop to $76.6 billion by the end of 2019. Meanwhile, sales dropped 24% last year at $58.16 billion as carriers withheld new orders due to concerns about a prolonged downturn in passenger volumes amid the pandemic.

Analysts appear to be fairly optimistic about the firm’s top-line results this year, as they are anticipating that they could climb near to where they were before the health crisis. However, Boeing will emerge as a more indebted company, with long-term debt currently standing at around $59 billion by the end of the first quarter of 2021 compared to the $27.5 billion the firm had by the end of 2019.

As a result, the company reported interest expenditures during this first quarter of this year that were almost three times higher than those it paid a year ago. These higher financial expenditures will likely depress the company’s earning generation capacity in the near future while solvency remains a concerning factor.

In this regard, even though the company held nearly $22 billion in cash and equivalents by the end of the first three months of 2021, Boeing burned almost $3.7 billion during that period.

For the time being, it seems that the firm has more than enough to withstand the blow that the pandemic has dealt to its business. However, the future is not too bright for Boeing shareholders as it could take years for the firm to emerge from its current high levels of indebtedness.

Boeing’s ability to produce positive bottom-line results from 2022 and forward could help it in securing the funding it will need two to three years from now to refinance its debt commitments and the market seems to be counting on that possibility as reflected by earnings estimates for 2022, which see Boeing’s earnings per share rising to $5.54 – around 31% what the firm brought in by the end of 2019.

These forecasted earnings result in a forward P/E ratio of 43 for Boeing, a multiple that seems heavily stretched based on the business’ deteriorated financial condition and the significant uncertainty and risk that the virus situation still presents to its recovery.

Based on these numbers, the upside potential for Boeing seems fairly capped and the stock remains unattractive both from a technical and fundamental standpoint. That said, it would be interesting to see how the price reacts to the upcoming earnings report as a post-earnings drop could result in a swift correction for BA stock, which would present an opportunity for short sellers.

Buy Stocks at eToro, the World’s #1 trading platform!