Big Lots Stock Price Up 11% – Is it Time to Buy BIG stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Big Lots stock is up 11% so far this month as the company’s top-line and bottom-line performance has been aided by the pandemic, with shoppers apparently enjoying the firm’s value proposition which consists of offering discounted items for bulk purchases.

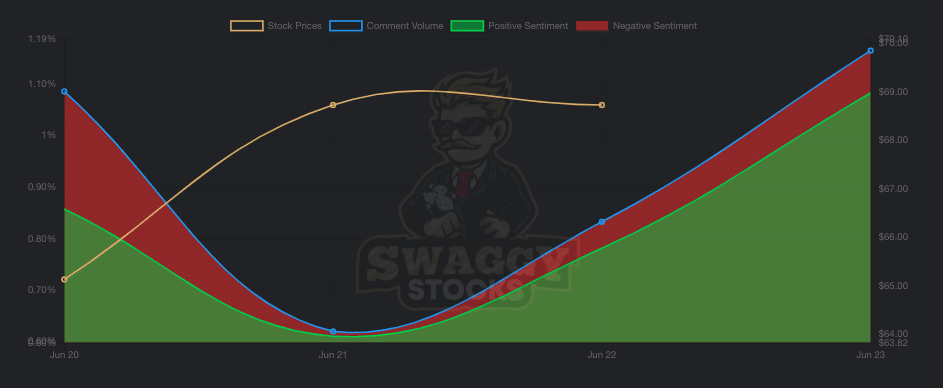

Meanwhile, the stock experienced a 5.7% uptick yesterday following a surge in comment volume about BIG on the popular Reddit messaging board WallStreetBets.

According to meme stock tracking website Swaggy Stocks, comment volume mentioning Big Lots stock surged to 0.8% of the forum’s total posts for 22 June while the percentage has moved higher today – currently standing at 1.2%.

Buy BIG Stock at eToro, the World’s #1 trading platform!

Apart from the possibility of BIG stock possibly becoming the “next pump” led by the WSB army, is this company an attractive one to buy based on its fundamentals and current technical setup?

The following article takes a closer look at BIG stock to see if there could be some upside potential for this big-box retailer even if WSB traders don’t come through.

Big Lots stock – fundamental analysis

Big Lots is an Ohio-based discount retailer with over 1,400 stores located in the United States that sells a wide range of products across multiple categories including food, furniture, electronics, and seasonal merchandise.

During the pandemic, the company experienced a significant jump in its top-line results amid increased online shopping volumes, with sales landing 16.5% higher by the end of the company’s 2021 fiscal year at $6.2 billion.

Before that, BIG’s top-line was barely growing, with sales hovering near the low $5 billion range for the past 8 years or so.

Meanwhile, gross margins for Big Lots have remained steady at around 40% while the firm’s EBITDA margin managed to climb from an average of 6.5% before the pandemic to 8.6% last year, possibly as the company benefitted from economies of scale.

Finally, Big Lots had already been progressively improving its bottom-line profitability before the pandemic stroked, with the firm’s net margin moving from 2.2% back in 2015 to 10.1% last year. Meanwhile, a year before the pandemic, the firm’s net margin stood at 4.6%.

Moreover, by the end of the first quarter of 2021, the company’s long-term debt was approximately $345 million on total assets of $2.4 billion excluding an item called “operating lease right-of-use-assets” which resulted from the sale and leaseback of some of the company’s distribution centers.

Net of cash, the current market capitalization of the firm stands at $1.66 billion, which results in a forward price-to-sales ratio of 0.27 and a forward P/E ratio of 6.4 for the company excluding cash based on analysts’ sales and EPS estimates for 2021, which currently stand at $6.13 billion and $6.65 per share respectively.

These valuation metrics seem awfully conservative for a business that displays a robust earning-generation capacity and a healthy balance sheet. Meanwhile, Big Lots offer a decent dividend yield of 1.78% that seems fairly sustainable upon taking a closer look at the company’s historical cash flow generation capacity.

Moreover, if the positive impact that the pandemic had on the business outlives the health crisis, chances are that the company will see its revenues grow in the following years – finally breaking a long-dated pattern of stalled top-line performance. This would present the possibility of multiple expansion for the stock.

Interestingly, from 2015 to 2019, Big Lots managed to grow its net income from $114 million to $242 million resulting in a 16.2% CAGR. If we assume that the company could be eventually valued at a price-to-earnings-to-growth ratio of one, Big Lots shares could jump to $106.4 per share based on this year’s forecasted EPS and a potentially higher P/E multiple of 16.

Big Lots stock – technical analysis

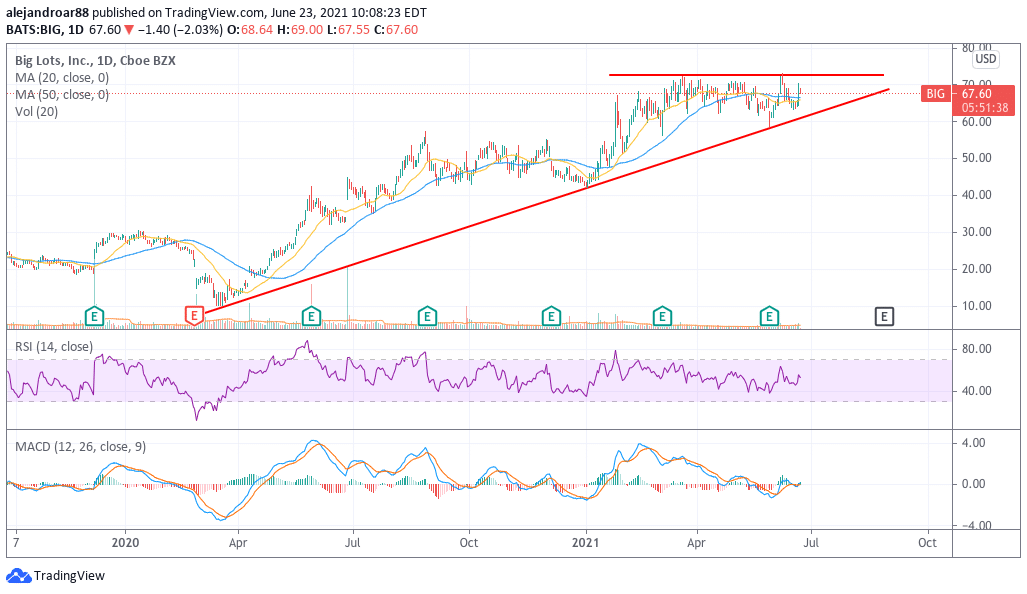

From a technical standpoint, the price of Big Lots stock has been posting a series of higher lows since the stock’s pandemic bottom seen in March last year, while the price action has encountered resistance at the $72.5 level two times in the past three months.

In my view, this would be a key level to watch for Big Lots and, with the firm’s next earnings release still months away, chances are that this threshold will be retested pretty soon as market participants will continue to push for higher valuations for the retailer.

A break above this level should result in the continuation of the current uptrend while a break below the $60 level might prompt a pullback in the stock price amid the loss of the long-dated lower trend line shown in the chart.

On the other hand, if the WSB army gets its hand on this stock, chances are that it could surge wildly amid the combination of low implied volatility – currently at the 9 percentile – while short interest for this stock is currently at 13.5% of BIG’s float – not bad for a short-squeeze.

Based on the stock’s average volume of 800,000 shares traded per day, it would take short sellers almost 5 days to fully cover their positions without affecting the price of the issue. Therefore, a short-squeeze of the likes seen by other issues such as GameStop (GME) and Blackberry (BB) is entirely feasible for BIG.

Buy BIG Stock at eToro, the World’s #1 trading platform!