Amazon Stock Soars to Record Highs After Q3 Earnings Beat

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Amazon stock (NYSE: AMZN) is up over 10% in early price action today and soared to a record high after the company beat Q3 2025 earnings estimates and provided upbeat guidance. Here we’ll analyze the e-commerce giant’s quarterly earnings and analysts’ reaction to the report.

Amazon Reported Better-Than-Expected Q3 Earnings

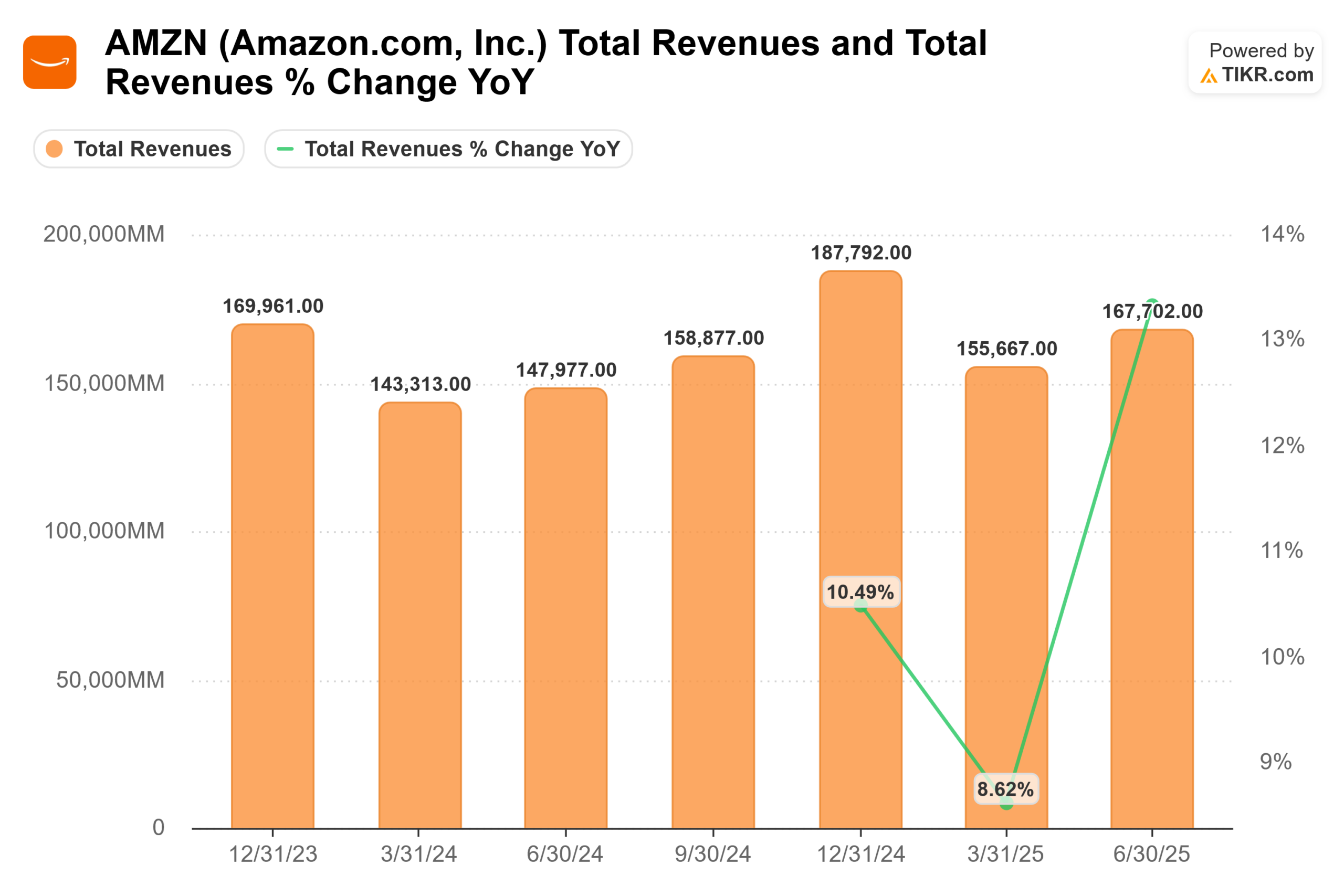

Amazon’s Q3 sales rose 13% year-over-year to $180.2 billion, marking a 13% increase year-over-year, or 12% excluding the favorable impact of foreign exchange rates. This figure surpassed the consensus forecast of $177.8 billion from Wall Street analysts.

Net Income saw a significant surge to $21.2 billion, translating to $1.95 per diluted share, handily beating estimates of $1.57. However, this figure was substantially boosted by a $9.5 billion pre-tax gain from Amazon’s investment in artificial intelligence (AI) startup, Anthropic, which is categorized as non-operating income.

Amazon’s operating income came in at $17.4 billion. This figure was weighed down by two substantial special charges totaling $4.3 billion. These include a $2.5 billion legal settlement with the Federal Trade Commission (FTC) and $1.8 billion in estimated severance costs primarily related to planned role eliminations. Excluding these one-time charges, operating income would have been a stronger $21.7 billion.

Amazon Raises Capex Guidance

CEO Andy Jassy emphasized the impact of AI, stating that it is “driving meaningful improvements in every corner of our business,” particularly in Amazon Web Services (AWS). The company is aggressively investing in AI infrastructure, including its custom Trainium chips, and expanding its data center capacity. This investment focus contributed to a sharp decline in trailing twelve-month free cash flow to $14.8 billion, primarily due to a substantial increase in capital expenditures.

How AMZN’s Business Segments Performed in Q3?

Amazon saw broad-based growth in Q3. Here is how the different segments performed in Q3.

- North America Segment sales grew by 11% year-over-year to $106.3 billion. Operating income for the segment was $4.8 billion, but excluding the $2.5 billion FTC settlement charge, it would have been $7.3 billion, highlighting underlying profitability in the core retail business.

- International Segment sales rose 14% to $40.9 billion (or 10% in constant currency), with operating income of $1.2 billion.

- Advertising revenue continued its impressive momentum, growing 22% year-over-year to approximately $17.7 billion, underscoring its role as a high-margin growth engine for the company.

- AWS recorded $33.0 billion in net sales for Q3 2025, marking an impressive 20% year-over-year growth. This acceleration was a key highlight of Amazon’s earnings, surpassing analyst expectations and representing the fastest growth rate for the cloud segment since 2022. This performance solidified AWS’s position as a powerhouse, with its annualized revenue run rate now reaching $132 billion.

AWS Saw Acceleration in Growth

AWS’s operating income also saw a healthy increase, reaching $11.4 billion, up from $10.4 billion in the third quarter of 2024. This growth came despite significant, ongoing capital expenditures directed primarily toward building out the necessary infrastructure to meet booming demand, especially for AI-related workloads.

The re-acceleration was overwhelmingly attributed to surging customer interest and spending on AI. Customers continued to increase their consumption of cloud services, and the shift toward generative AI applications is beginning to translate into substantial revenue.

Commenting on AWS performance, Jassy said that the business is “growing at a pace we haven’t seen since 2022” while adding “We continue to see strong demand in AI and core infrastructure, and we’ve been focused on accelerating capacity — adding more than 3.8 gigawatts in the past 12 months.”

Amazon Provided Better-Than-Expected Guidance

For the crucial fourth quarter, which includes the holiday shopping season, Amazon provided an optimistic outlook. It expects Net Sales to be in the range of $206 billion to $213 billion, whose midpoint was ahead of Street estimates. The company expects Q4 operating Income to be between $21 billion and $26 billion, versus the consensus estimate of $23.8 billion.

Amazon Might Announce More Layoffs

Amazon recently announced 14,000 layoffs, which Jassy said were not “AI-driven” or “financially driven” at least for now, and attributed them to the company “culture.” He added, “If you grow as fast as we did for several years, you know, the size of the businesses, the number of people, the number of locations, the types of businesses you’re in, you end up with a lot more people than what you had before, and you end up with a lot more layers.”

He also alluded to more layoffs and said, “I don’t know if there’s ever been a time in the history of Amazon or maybe business in general with the technology transformation happening right now, where it’s important to be lean, it’s important to be flat, and it’s important to move fast, and that’s what we’re going to do.”

Analysts Raise AMZN’s Target Price

After Amazon’s Q3 release, several brokerages raised the stock’s target price. For instance, Cantor Fitzgerald raised its target price from $280 to $315 while DA Davidson raised its from $265 to $300. Evercore ISI analyst Mark Mahaney raised his target price to a Street-high of $335.

Wedbush raised Amazon’s target price to $330 and, in its note, said, “AWS accounts for just ~45% of the implied value of the overall business in our sum-of-the-parts (SOTP) analysis, and there is considerable value in the other core segments of the company that we believe has been overlooked in recent periods.”

The note added, “We are encouraged by the implied level of demand in the coming quarters, given the pace of backlog growth and a higher capex guide for 2025.”