5 Best Ways How to Invest £1,000 In July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Are you wondering where you could put a spare £1,000 to avoid losing money as a result of the negative savings rates paid by your bank?

The following article analyzes five individual stocks that seem poised to deliver the kind of growth that may justify the risk taken.

These stocks operate in high-growth sectors of the economy, they have been growing their top-line results at remarkably elevated rates, and their balance sheet is fairly robust – a three-punch combination that increases the likelihood of further upside potential in a global economy that is flooded with cash looking for attractive places to be parked.

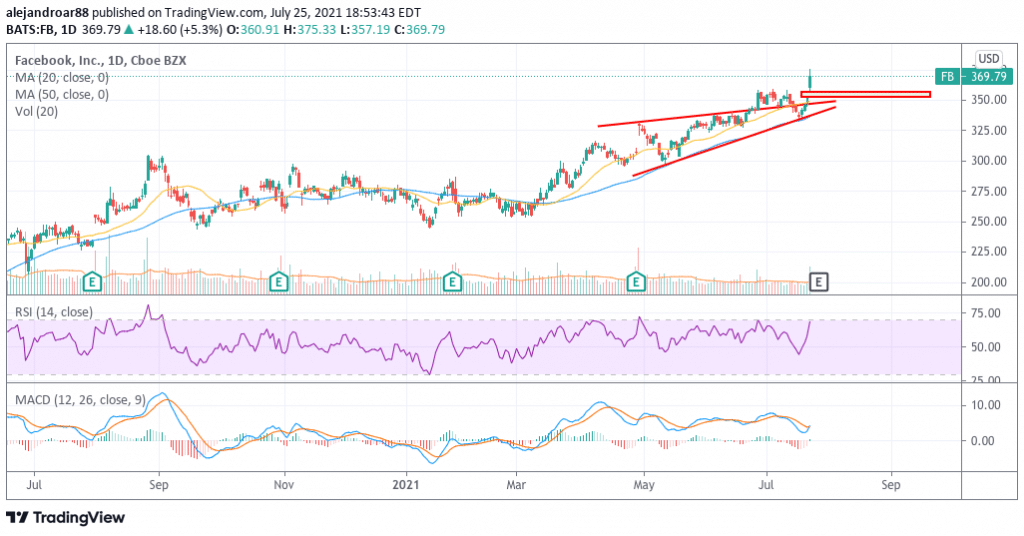

#1 – Facebook (FB)

Facebook shares are up 35% this year, already exceeding the gains the stock saw during 2020 ahead of this week’s Q2 earnings report.

Although the social media company has already surpassed the $1 trillion mark in market capitalization, valuation multiples appear to be somehow depressed considering Facebook’s outstanding track record of revenue and earnings growth.

In this regard, the market appears to be having an overly pessimistic opinion about the impact that upcoming legislation could have on the company’s future performance, primarily worrying about anti-trust lawsuits and increased government scrutiny.

Concerns aside, in the past 4 years, Facebook has managed to almost double its bottom-line profitability, with diluted earnings per share advancing from $5.4 in 2017 to $10 per share by the end of 2020.

Meanwhile, analysts are expecting to see a continuation of that growth in the following three years at least, with GAAP EPS expected to land at around $17.76 per share by the end of 2023. This results in a compounded annual growth rate of 21% for Facebook’s EPS and it makes the current forward earnings per share ratio of 28 granted to Facebook look pretty conservative.

Moreover, the company displays a robust balance sheet comprised of only $11 billion in long-term debt along as the firm has total cash and equivalents of $64 billion. Additionally, the company generates over $25 billion every year in cash flows, resulting in a price-to-cash flow multiple of 40.

Even if Facebook’s earnings growth decelerates a bit in the following years, the company should continue to enjoy positive valuation multiples while those multiples could expand if the air gets clearer in terms of regulatory pressure.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#2 – Square (SQ)

Square is on track to become the modern Visa and Mastercard of small businesses as the company is progressively advancing its reach when it comes to positioning itself as a multi-faceted financial technology business.

Last year, Square entered the cryptocurrency market by offering the possibility of buying and selling crypto tokens through its platform and only a few days ago it announced that it will start offering financing to small businesses within its ecosystem.

This solution, called Square banking, will open a whole new revenue stream for the firm and could accelerate its already fast-paced revenue growth. Additionally, the company has been entering other promising markets that could open further revenue streams by assisting small businesses with tasks including accounting, workforce management, and supply chain.

In the past four years, Square’s revenues have been growing at a fast pace while its operating income has been progressively expanding from $12.8 million in 2017 to $168.9 million by the end of last year.

Meanwhile, the firm has swung to profitability already, delivering $210 million in net income for investors last year resulting in diluted earnings per share of $0.4. Moreover, analysts are expecting to see those results multiply by 3 times by the end of 2023 at $1.4 per share.

That results in a seemingly elevated forward P/E ratio of 188 but the company’s future earnings growth resulting from significant leaps in revenue – most of which are not being priced in – should justify those multiples.

As per its balance sheet, Square had long-term debt of $3.4 billion by the end of the first quarter of 2021 and a total cash position of almost $4 billion. Additionally, the company has been using some of its positive free cash flows to buy hundreds of millions in stock in the past three years, with a total of $314 million in buybacks made last year alone.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#3 – FuboTV (FUBO)

FuboTV is considered by many the Netflix of sports streaming. The company is relatively young but, in a seemingly short period, it has delivered the kind of results that makes it qualify as a promising long-term growth pick.

During the first quarter of 2021, FuboTV delivered total revenues of $120 million resulting in a significant leap compared to the $7.3 million it reported during the first quarter of 2020 as a result of higher subscriber additions while the advertising revenue stream has started to pick up some steam.

Meanwhile, the company forecasted total revenues of $525 million for 2021 – more than twice what it brought in 2020 – while total subscribers are expected to land at 840,000 – up 53% compared to the previous year.

Additionally, FuboTV recently announced another important partnership that should open a whole new revenue stream in the future for the firm through a sports betting feature that will accompany its streamed content.

In terms of valuation, Fubo is being valued at only 6 times its forecasted sales for 2021 – a multiple that seems fairly low for a business that has been able to duplicate its revenues in a year and that is expected to achieve a similar undertaking in subsequent periods.

Meanwhile, the company held a total long-term debt of $310 million on assets of $1.2 billion including $459 million in cash that should be progressively deployed in the next quarters in the form of acquisitions and the purchase of broadcasting rights for top sports events.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#4 – Fiverr (FVRR)

Fiverr is the largest marketplace for the “gig economy” in the United States, with a total of 3.81 million active buyers by the end of the first quarter of 2021 and more than 1 million active sellers.

By the end of 2020, the company processed nearly $1 billion in transactions through its platform and it is expected to keep growing those volumes in the future as more and more employers rely on freelancers to perform key assignments for their companies.

Revenues for the company have been growing steadily in the past few years, landing at $190 million by the end of 2020 – almost doubling the figure compared to 2019’s results. Meanwhile, gross margins have improved from 79% to as much as 83% lately and net losses have been trimmed during that same period

At the moment, the company is being valued at 17.5 times its forecasted sales for 2023. However, market participants appear to be expecting a slowdown in the company’s top-line growth rate – a situation that seems highly unlikely as more and more employers are expected to turn to Fiverr’s marketplace to find independent contractors.

Even though multiples are a bit stretched at the moment, this is a company that could shape the future of the labor market. If one thinks of Fiverr as the Amazon of the gig economy, the valuation doesn’t seem that stretched and could actually present a once-in-a-lifetime-opportunity to buy at a $9 billion valuation.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#5 – D.R. Horton Inc. (DHI)

The housing market in the United States is booming on the back of historically low interest rates and nothing indicates that this overly favorable environment for home builders will change soon as central banks are expected to maintain their highly accommodative policies for two more years at least.

In this landscape, D.R. Horton is particularly well-positioned to generate solid bottom-line growth despite the current supply-side constraints – which seems to be a fairly temporary phenomenon.

Before rates and demand were this attractive, this home builder was already reporting strong revenue growth rates, with top-line results moving from $14 billion in 2017 to $20.3 billion from 2017 to 2020 at a compounded annual growth rate of 13.2%.

Meanwhile, bottom-line profitability more than doubled during that same period, moving from $1 billion to $2.4 billion, while diluted earnings per share advanced from $2.8 to $6.5 at a 32% CAGR.

For this year, analysts are expecting an explosion in revenues as they are estimating an annual 37% jump in the firm’s top-line results to $27.8 billion while GAAP earnings per share are expected to double. The best part is that this company is trading at only 8 times its forward earnings per share despite these overly positive forecasts.

Moreover, its long-term debt is fairly small, currently standing at $4.4 billion on total assets of $22 billion and cash and equivalents of $1.8 billion by the end of 2021.

Under these favorable market conditions, it seems highly likely that the firm will exceed the market’s expectations and even though inventories have been building up as a result of the latest COVID-related disruptions, turnover rates should pick up once the US fully comes out of the health contingency and supply-side bottlenecks are solved.

Buy Stocks at Vindax FX, the World’s #1 trading platform!