5 Best UK Shares to Buy in July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

UK share markets have rebounded and the FTSE is up almost 7% for the year. With most COVID-19 restrictions lifted in the UK, what are the best UK shares to buy in July 2021?

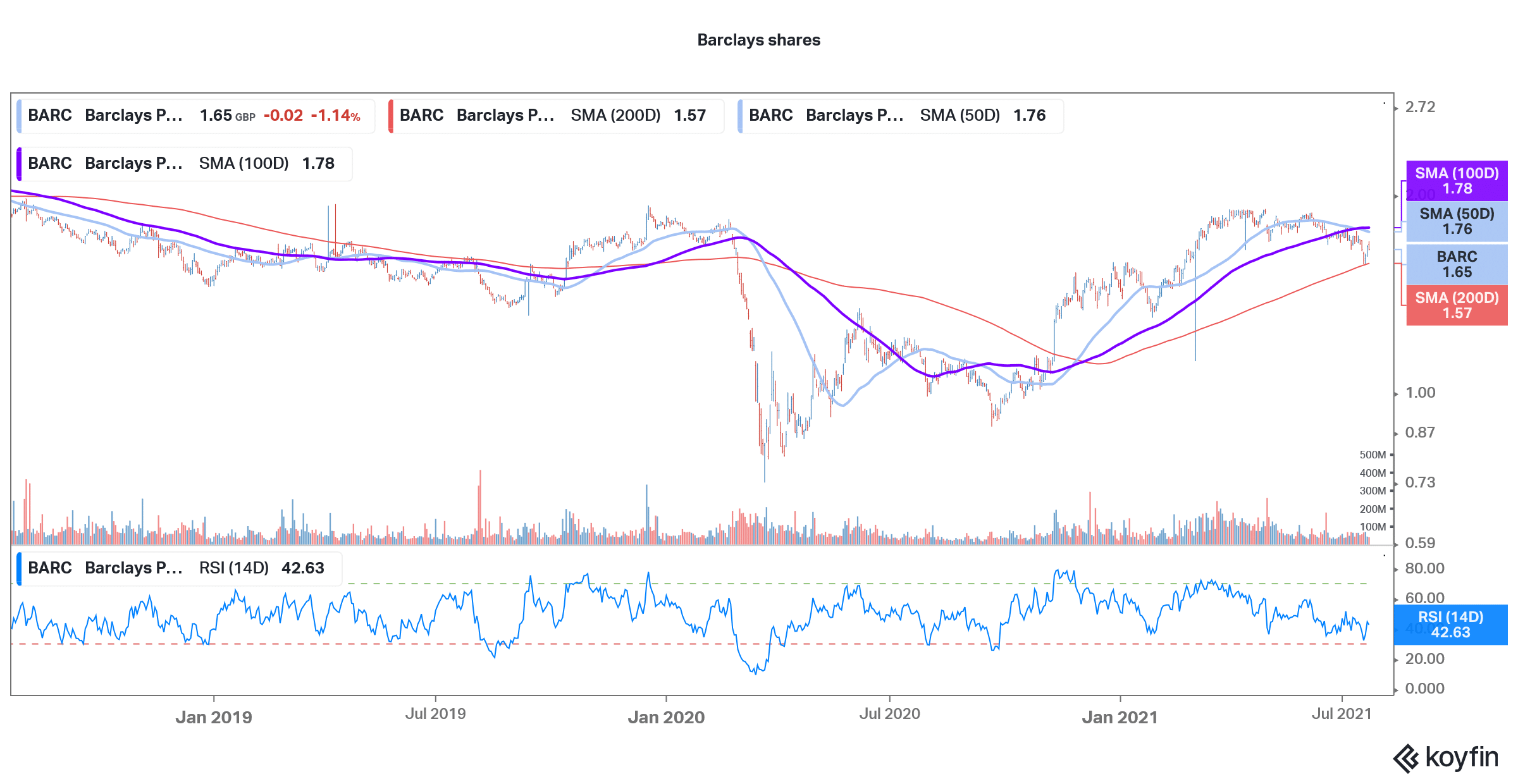

1. Barclays Plc. (BARC)

Barclays shares are up almost 17% so far in 2021. However, they have come off their 2021 highs and are currently trading at a discount of 12% to their 52-week highs. There has been a sell-off in banking shares amid the volatility in bond yields. Also, there have been concerns about the growth outlook amid the increase in new cases of coronavirus from the Delta variant.

BARC looks like a good UK share to buy

Barclays has a strong balance sheet and at the end of March, it had a tier 1 capital ratio of 14.6% which is higher than the 13-14% that the bank targets. Its payments business is also a long-term value driver. During the first quarter 2021 earnings call, Barclays said that “Taken as a whole, we believe our payments complex can generate an additional GBP900 million of income over the next three years.”

Should you buy Barclays shares?

Barclays’s shareholders might also be rewarded with a higher dividend payout as the Bank of England has removed the restrictions on pay-outs. However, the regulator expects banks to take a cautious approach. “We expect bank boards to be appropriately prudent in distributions they make both to their shareholders and to their staff, given the vital role that banks are going to play in supporting the recovery,” said Bank of England Deputy Governor Sam Woods.

While releasing its fiscal first quarter 2021 earnings, Barclays said that its tangible net asset value (TNAV) is 267p per share. The share currently trades at 167.6p which is a discount of almost 38% over the TNAV. The shares trade at an NTM (next-12 months) PE multiple of 6.5x which also looks attractive.

Barclays shares have found support

Barclays shares found strong support at the 200-day SMA (simple moving average) and rebounded sharply from the trendline. The shares now face resistance at the 50-day SMA. The 14-day RSI (relative strength index) of 42.6 is a neutral indicator. Overall, Barclays shares look a good buy given the strong economic outlook and the tepid valuations.

67% of all retail investor accounts lose money when trading CFDs with this provider.

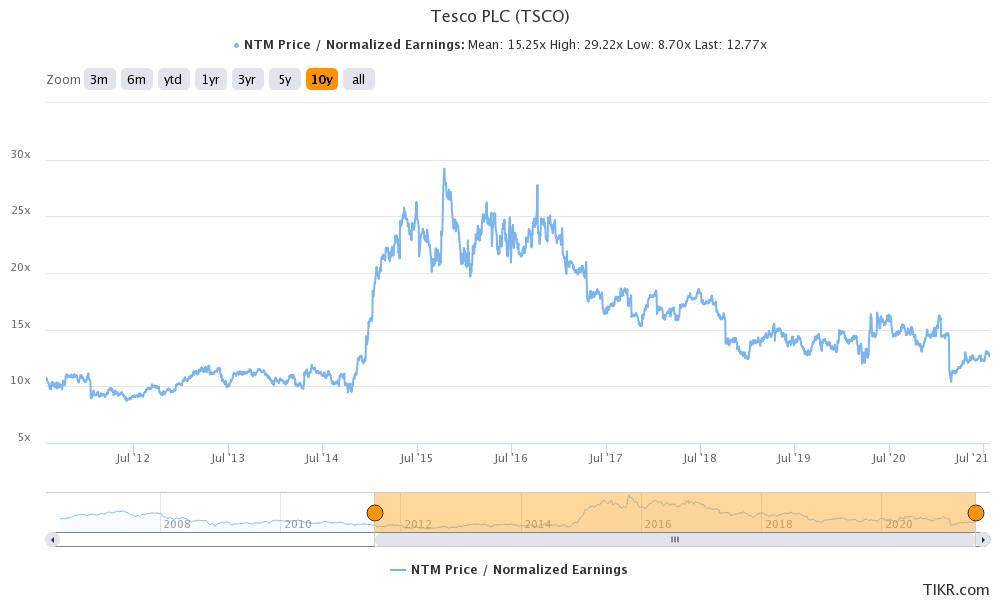

2. Tesco (TSCO)

While markets have rebounded in 2021, Tesco shares have sagged and are down almost 22%. It is not very far from its 52-week low price of 217.10p. Meanwhile, the fall in Tesco shares could be a good buying opportunity. Given the expected economic growth, Tesco should see a rebound. Analysts are also bullish on Tesco.

Of the 18 analysts polled by Financial Times, 14 rate Tesco shares as a buy or some equivalent while three rate them as a hold. Only one analyst has a sell rating on Tesco. Its median target price of 295p implies an upside of 27% over the next 12 months. The highest target price of 392.67p is a premium of almost 70% while the lowest target price of 220p is a discount of 5.1%.

Tesco shares look a good buy

Tesco shares trade at an NTM PE multiple of 12.7x. The multiples have averaged 16.11x and 15.25x over the last five years and ten years respectively. The valuation discount looks a bit too high and Tesco shares look attractive at these price levels.

67% of all retail investor accounts lose money when trading CFDs with this provider.

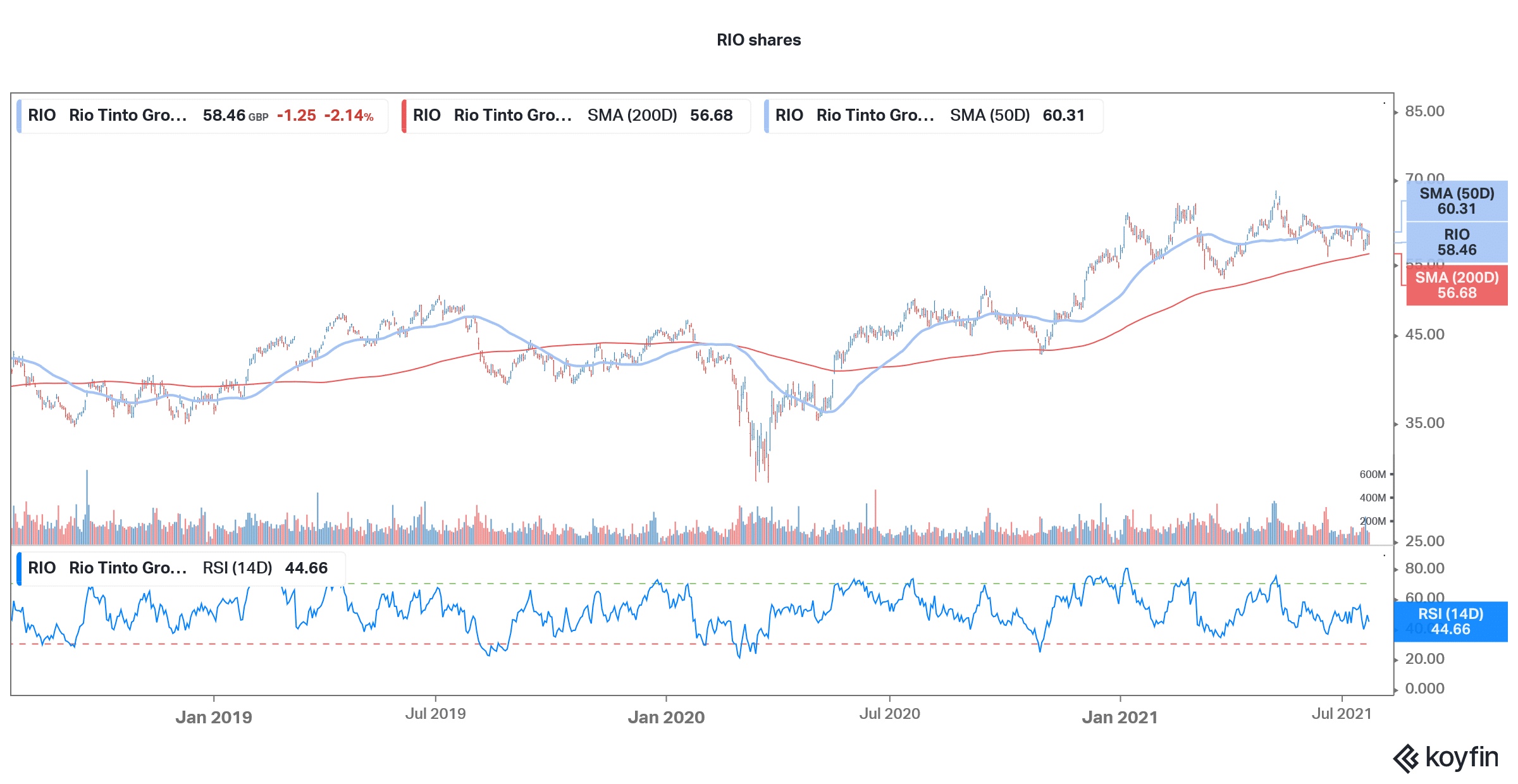

3. Rio Tinto Group (RIO)

Rio Tinto shares have pared their recent gains and are currently up only about 2.5% for the year. There has been a correction in all metals and mining shares and RIO is no exception. That said, the concerns over a crash in commodity prices look unfounded even as metals have come off their 2021 highs.

We are in a commodity supercycle that bodes well for RIO. The company produces metals like iron ore, copper, and aluminum but iron pre accounts for the bulk of its earnings. There are concerns over iron ore demand as the biggest consumer China is planning steel production cuts in the second half of the year. Almost all of the iron ore that’s mined goes into steel production and China accounts for over two-thirds of global seaborne iron ore demand.

Rio Tinto shares look a good buy

Rio Tinto looks like a good UK share to buy considering the positive outlook for iron ore prices. The company has a dividend yield of 5.79% and the yield might rise further as the company might increase the distributions. AJ Bell expects RIO’s dividend yield at 12%. However, it also issued a note of caution. “Often defending a high yield can be a burden for a firm, as it sucks cash away from vital investment in the underlying business, or can be a sign that the company is in trouble and investors are demanding such a high yield to compensate themselves for the (perceived) risks associated with owning the equity.”

RIO shares trade at an NTM EV-to-EBITDA multiple of only about 3.4x. While the multiples for mining companies bottom at the cyclical peaks, as we currently have, they nonetheless look attractive. Looking at the technicals, RIO shares are facing resistance at the 50-day SMA. It needs to break above the channel for the uptrend to resume. However, if you are looking at a mining share with a high dividend yield, RIO will fit the bill.

According to the data from CNN Business, RIO’s median target price implies an upside of over 41% over the next 12 months.

67% of all retail investor accounts lose money when trading CFDs with this provider.

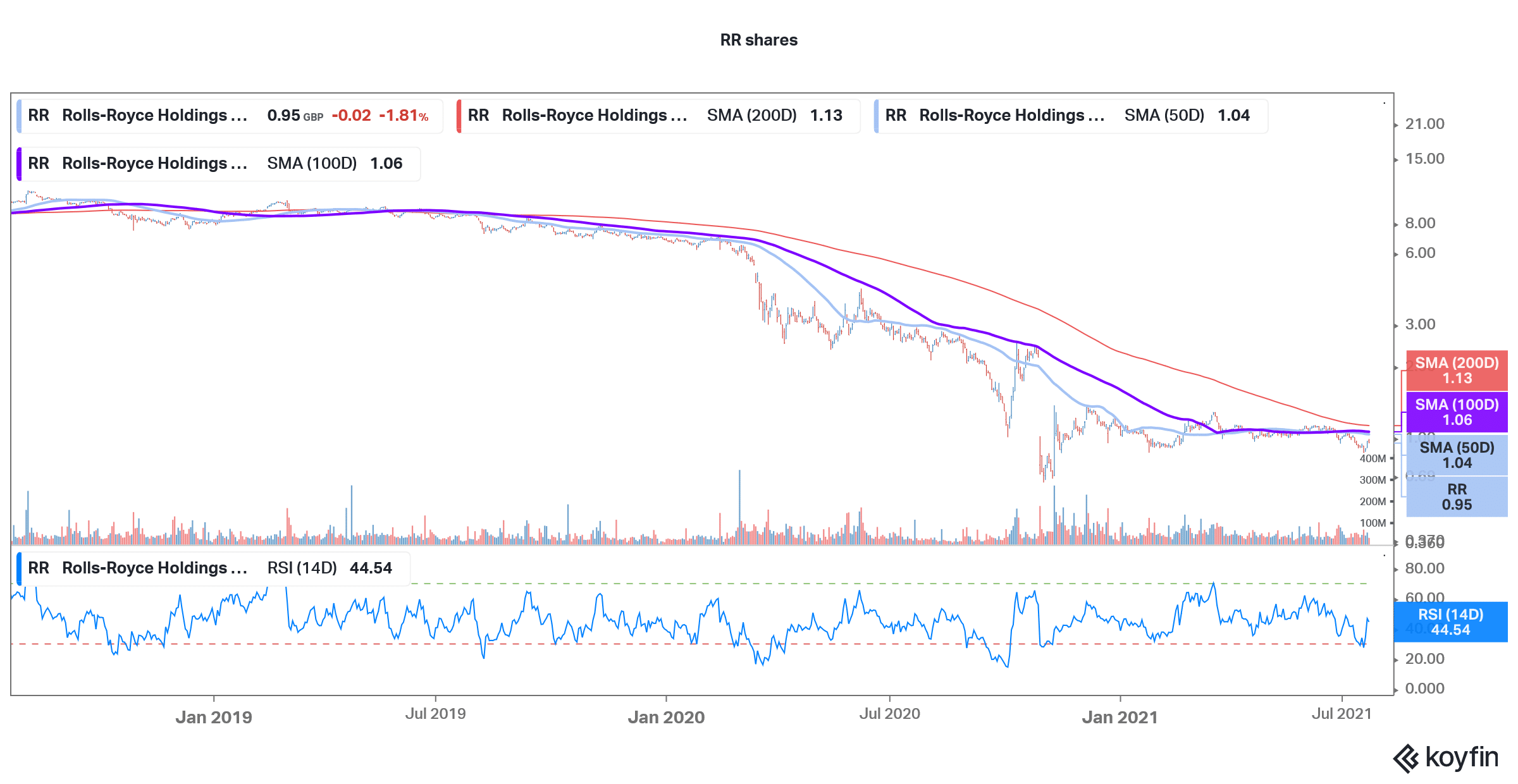

4. Rolls-Royce (RR)

Rolls-Royce shares have been battered as the lockdowns took a toll on the airline industry and hence its revenues as well. However, RR looks like a good buy now and bet on a revival in the industry. The company has taken several measures to control costs and is also looking at selling its non-core assets. While a lot of cyclical companies have rebounded, RR continues to sag.

RR is a good UK share to buy

Analysts also see upside in RR shares and its median target price of 113p is a premium of 18.6%. Of the 21 analysts covering RR, five rate them as a buy while nine rate them as a hold. The remaining seven analysts have a hold rating on Rolls-Royce.

How do RR shares look on the charts?

RR has been in a downtrend and is not looking too bullish on the charts. The shares trade below the 50-day, 100-day, and 200-day SMA. The first major resistance for RR would be the 50-day SMA. RR needs to rise above the level to signal a technical uptrend.

Looking at the valuations, RR trades at an NTM EV-to-revenues multiples of around 1x which looks attractive. Overall, if you are looking to play the reopening story with an attractively priced name, RR would fit the bill.

67% of all retail investor accounts lose money when trading CFDs with this provider.

5. Asos (ASC)

Asos shares tumbled recently after the company warned of uncertainties due to the COVID-19 pandemic. Earlier this month, the online fashion retailer released its trading update that spooked markets. While it reported strong revenue growth in the four months ended 30 June, it cautioned on a slowdown.

“Trading in the last three weeks of the period was more muted, as continued COVID uncertainty and inclement weather, particularly in the UK, impacted market demand. We anticipate a measure of volatility to continue in the near term, given the rapidly evolving COVID situation worldwide,” it said in the release. The company added, “As a result, we expect our underlying P4 growth rate to be broadly in line with the prior year comparable period. We expect overall full year adjusted PBT to be in line with our expectations.”

Asos CEO Nick Beighton said “Uncertainty, particularly around changes to travel rules and hence the ability of people to book holidays, means that customers are finding it difficult to plan their lives and wardrobe choices,”

The dip in Asos shares look like a buying opportunity

Asos is down sharply from its highs and the dip looks like a good buying opportunity. According to the data from Financial Times, Asos has a median target price of 6,025p which is a premium of 43% over current prices. It has 14 buys, seven holds, and two sell ratings.

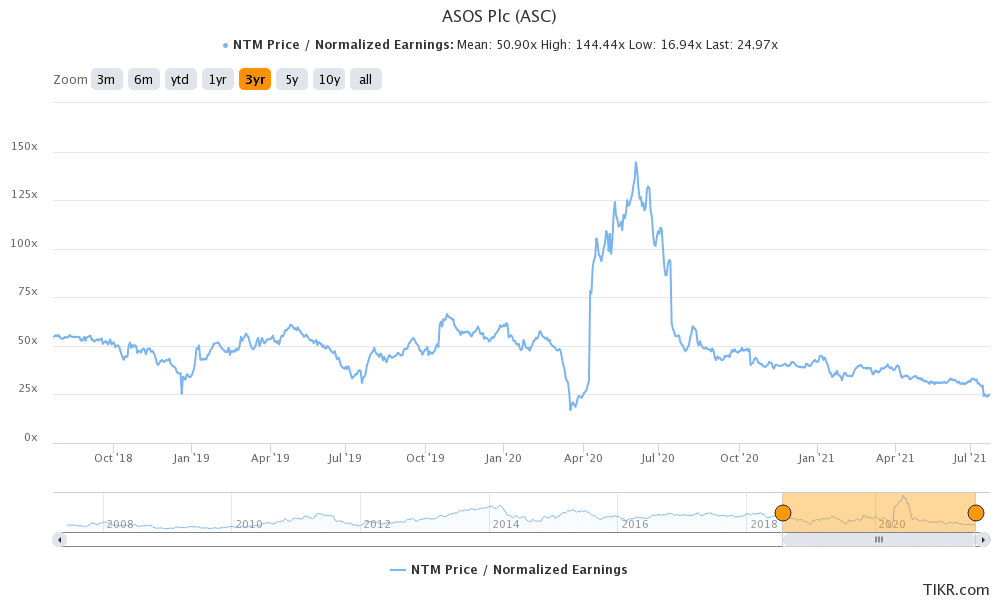

Asos shares now trade at an NTM PE multiple of 25x which is below what it traded historically. For instance, the average PE multiple over the last three years has been 50x. The valuation discount and the recent dip make Asos shares a good buy.

67% of all retail investor accounts lose money when trading CFDs with this provider.