5 Best Stocks to Invest in During August 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

With thousands of companies already reporting their earnings for the second quarter of 2021, the outlook for multiple firms is now clearer as the world progressively steps out of the pandemic on the back of en-masse vaccinations.

Companies in traditional sectors like oil & gas and finance have emerged as likely winners of the progressive economic recovery that should come after the virus crisis is over while some pandemic winners have taken a hit amid an ongoing sector rotation.

In this particular environment, investors must focus on the fundamentals of the underlying business to see if opportunities have emerged either as a result of short-term earnings-related downticks or amid tailwinds that could now push certain virus-battered companies to the spotlight.

In the following article, I’ll share five names that display the kind of robust fundamentals, attractive valuations, and positive past performance that make them qualify as top picks at their current prices.

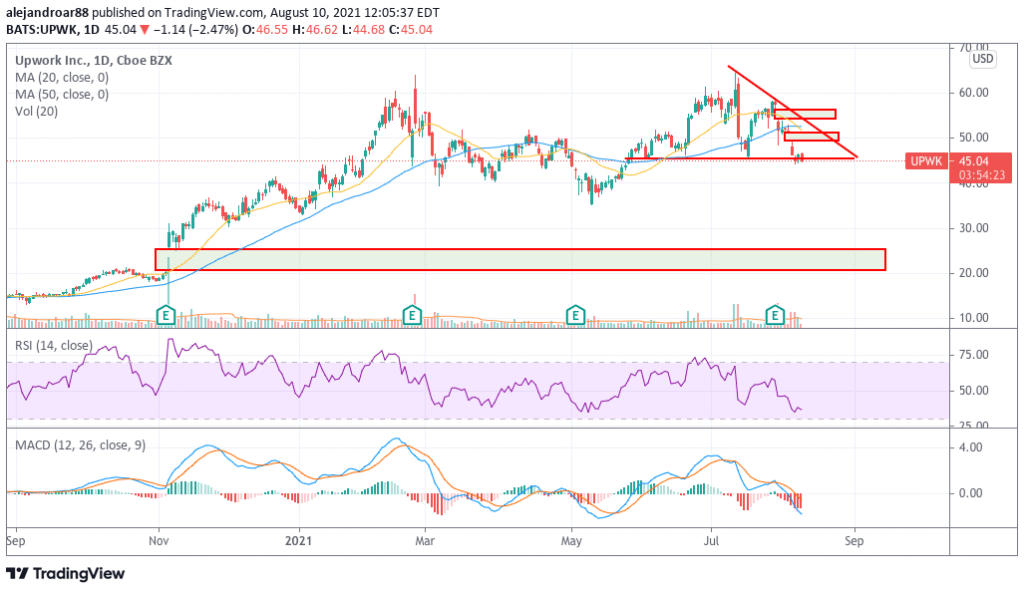

#1 – Upwork (UPWK)

Upwork is a marketplace where companies can hire professional talent. The company has emerged as one of the strongest players in the so-called “gig economy” and the latest weakness in its share price may be opening up the opportunity to buy the stock of this promising up-and-coming business at a more decent valuation as UPWK is currently trading 30% below its 52-week high.

In the past four years, the company has been managing to grow its revenues from $164 million (2016) to 373.6 million (2020) at a compounded annual growth rate (CAGR) of 23%. Moving forward, Upwork is expected to grow its sales at an average rate of 25% while the company is displaying a positive trend of improving top-line and bottom-line profitability.

Gross margins have moved from 79% to around 83% lately while the company has been progressively trimming its negative operating results and could soon swing to profits once the management decides to cut back on marketing and other similar expenditures.

At its current market capitalization of $5.7 billion, Upwork is being valued at 11.5 times its forecasted sales for this year. Even though this metric seems a bit stretched, the pandemic may accelerate growth rates for the firm moving forward as more employers have tested the benefits of incorporating freelancers into their workforce – a situation that will benefit the company in the long term.

Moreover, Upwork can also play a role in the development of the so-called metaverse as the company could tap on this technology to further improve the quality of the interactions and relationships between freelancers and employers through AR and VR interfaces.

67% of all retail investor accounts lose money when trading CFDs with this provider.

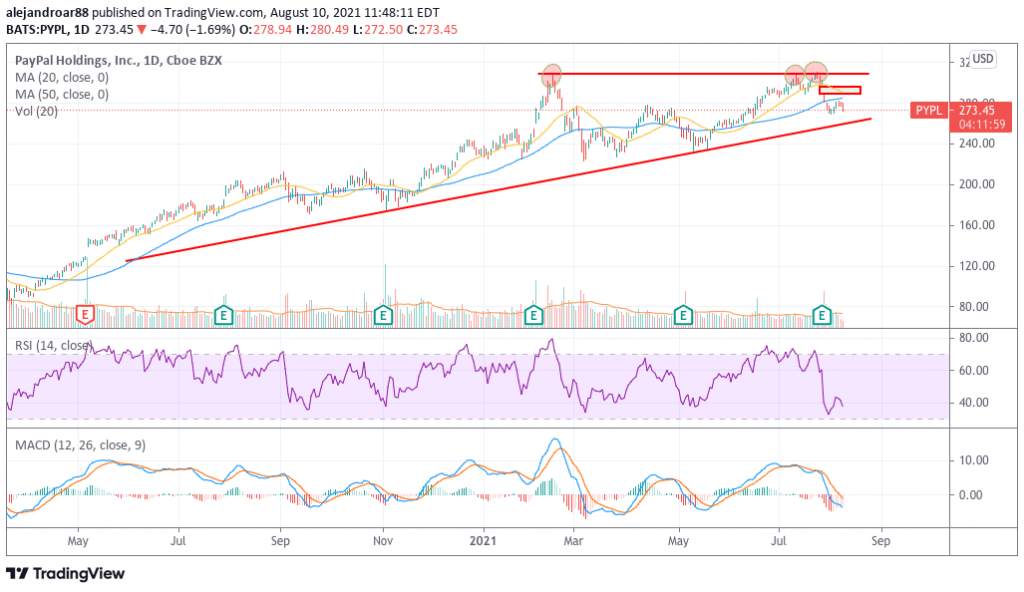

#2 – PayPal Holdings (PYPL)

PayPal shares dropped as much as 6% after the company reported its earnings covering the second quarter of the year as the management indicated that they expect a deceleration in business volumes moving forward as the world steps out of the pandemic.

This weakness in the share price might be providing investors with an opportunity to buy a high-growth business at a more attractive price, considering that PayPal is now trading at 55 times its NTM earnings per share, a number that seems fairly attractive for a company that is expected to grow its earnings at a rate of around 25% over the next three years or so and that has proven its ability to adapt and respond to changes in the competitive landscape as reflected by its decision to introduce cryptocurrency trading to its already ample portfolio of services.

Even though for some investors this multiple might sound too high, it is important to note that PayPal’s dominant position in the digital payments market makes it a top bet in this high-growth industry while the company has zero net debt, a positive track record of over $2 billion in share repurchases made every year, and a growing return on equity (ROE) metric that has moved from 13% in 2018 to 23% by the end of 2020.

67% of all retail investor accounts lose money when trading CFDs with this provider.

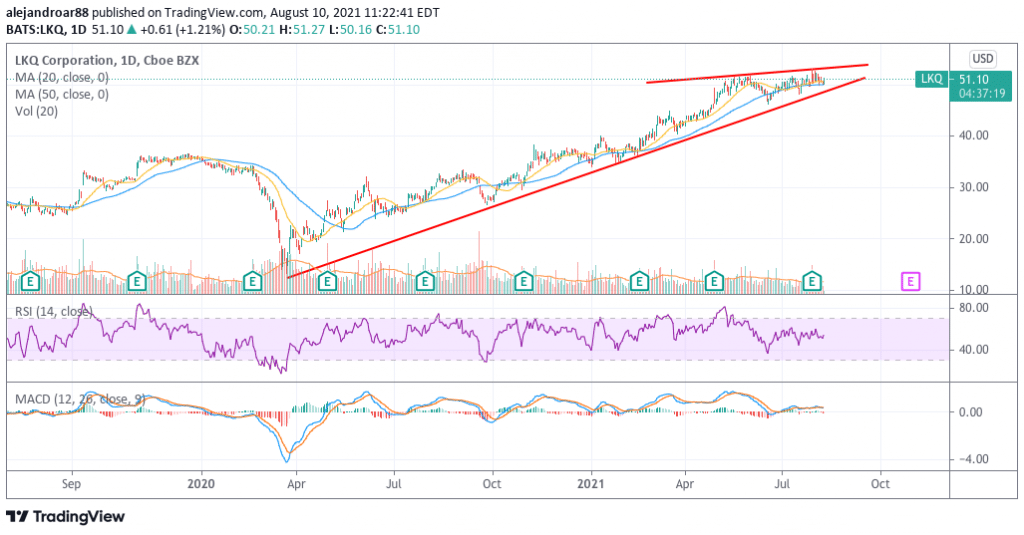

#3 – LKQ Corporation (LKQ)

The pandemic has proven to be just a bump in the road for LKQ Corporation as the company’s positive track record of top-line growth seems to be resuming as indicated by its latest positive quarterly results.

By the end of the second quarter of this year, the company reported sales of $3.44 billion for a 30% year-on-year jump while it also exceeded its pre-pandemic levels for the same period by 5.5%.

The firm has been improving its profit margins in the past few years – currently standing at around 40% – while its EBITDA margins have also been increasing from 10.5% back in 2018 to almost 14% in the past twelve months.

Moreover, the company’s diluted earnings per share have been progressively moving higher from $1.50 back in 2016 to $2.09 by the end of 2020 at an 8.7% CAGR while earnings are expected to jump 64% this year at $3.43 per share.

Based on that estimate, the stock is trading at only 15 times its 2021 forecasted EPS while the company’s cash flows have been growing steadily from around $460 million in 2018 to $1.3 billion by the end of 2020 at a 68% CAGR.

At a market capitalization of $15 billion, that results in a P/FCF ratio of only 11.5 that seems fairly attractive for a company with a positive track record of revenue and earnings growth, multiple strong brands, and a robust balance sheet comprised of only $3.6 billion in long-term debt on assets of $12.44 billion.

67% of all retail investor accounts lose money when trading CFDs with this provider.

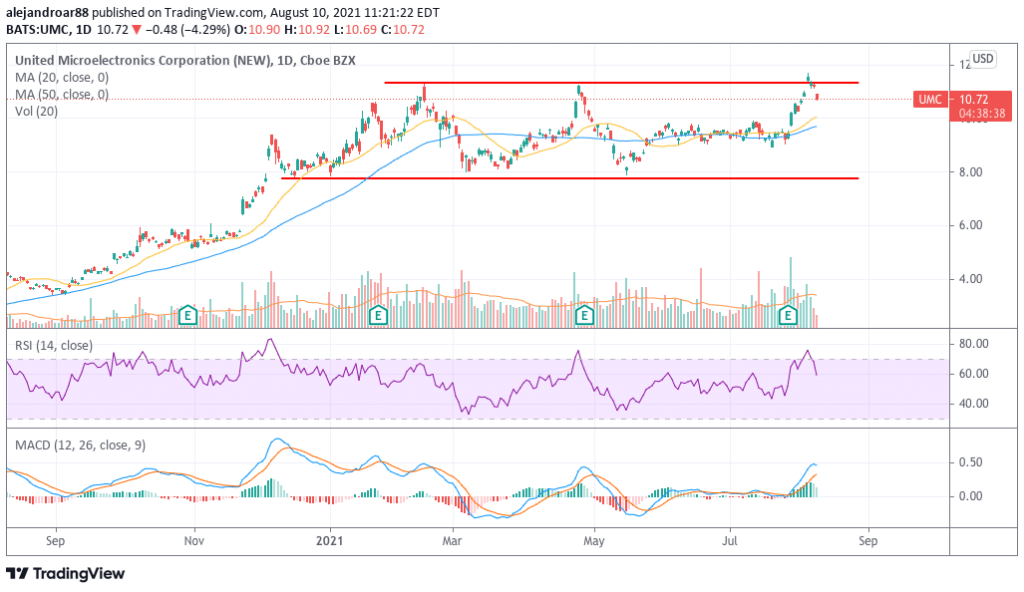

#4 – United Microelectronics Corporation (UMC)

UMC is a Chinese company operating in the promising semiconductor market that has displayed an appealing track record of revenue, earnings, and cash flow growth and that stands to benefit from the ongoing global chip shortage.

The company’s revenues were fairly stalled lately at around $5 billion but leaped to $6.3 billion last year and are expected to land at $7.48 billion this year and $8.6 billion by the end of 2023.

Meanwhile, the firm managed to reverse a downtrend in its profit margins, delivering gross profit margins of 22% last year for an 800 basis points leap compared to the previous year while net profit margins also came in higher at 13% compared to an average of 5% in the preceding two years.

Moreover, the firm’s earnings per share have moved from a range between $0.02 and $0.03 to $0.07 per share and are expected to land at $0.12 by the end of 2021 and 2022.

Additionally, the firm has a solid track record of free cash flow growth in the past three years at least, generating over $1 billion in free cash flows in 2019 and 2020 while pushing the figure to $2 billion by the end of 2020.

All these positive developments contributed to the 226% gain the stock delivered last year while UMC shares are up another 30% this year as market participants keep jumping on board on the back of the company’s improving fundamentals.

At its current market capitalization of $27.7 billion, the business is trading at only 14 times its free cash flow from 2020 and at 18 times its forecasted earnings for next year. Those multiples make it a reasonably valued business that is favorably positioned to keep benefitting from the current tailwind the industry as a whole is experiencing.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#5 – EOG Resources (EOG)

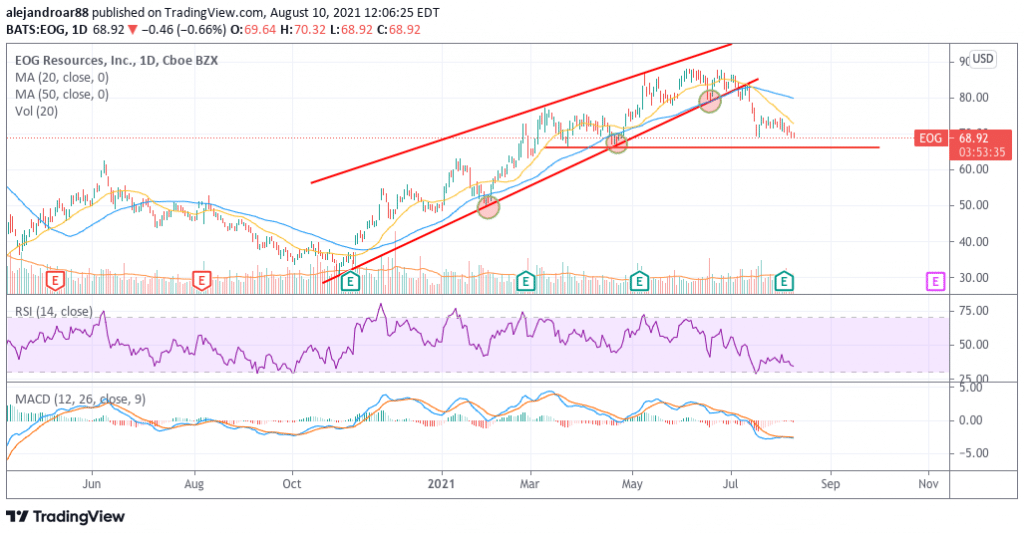

Even though the latest weakness in the price of oil has broken EOG’s latest uptrend, the business fundamentals remain strong and the company’s track record of positive top and bottom-line growth seems poised to continue in the current favorable environment.

Sales for EOG Resources more than doubled from 2016 to 2019 – before the pandemic stroked – landing at $16.9 billion by the end of that year to then drop to $9.8 billion in 2020 amid the hit that the oil market took during the virus crisis.

With robust operating margins above 45%, this company is one of the most efficient players in the oil & gas industry and that efficiency has not been affected by the pandemic as demonstrated by its latest quarterly report in which the firm reported solid gross margins of 64.5% and operating margins of 46%.

Currently being valued at 8.7 times its forecasted earnings for the next twelve months, EOG remains a fairly attractive bet on the oil sector and its balance sheet is conservative enough to allow the firm to withstand any short-term hit the market may take as its long-term debt stands at only $5 billion on total assets of $36.9 billion including $3.9 billion in cash.

So far this year, the stock has gone up 43% and is standing near its pre-pandemic levels although it has given up some of that advance amid the latest weakness in the oil market. Moving forward, the current price of oil is still high enough to support a promising outlook for this efficient oil & gas driller.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Buy Stocks at Cedar FX, the World’s #1 trading platform!