5 Best Stocks to Buy in August 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

As a large percentage of companies have already reported their earnings for the second quarter of the year, investors now have more visibility on what to expect moving forward. During this season, tech firms have experienced certain unexpected trend reversals in their stock price as early buyers have taken some chips off the table after successfully pricing most of the positive results that were revealed lately.

Meanwhile, other companies have seen their share price affected by different external factors and that means opportunities for investors to step in and fish in troubled waters.

In the following article, I’ll bring to your attention five individual names you may want to consider based on the latest developments that have affected their share price.

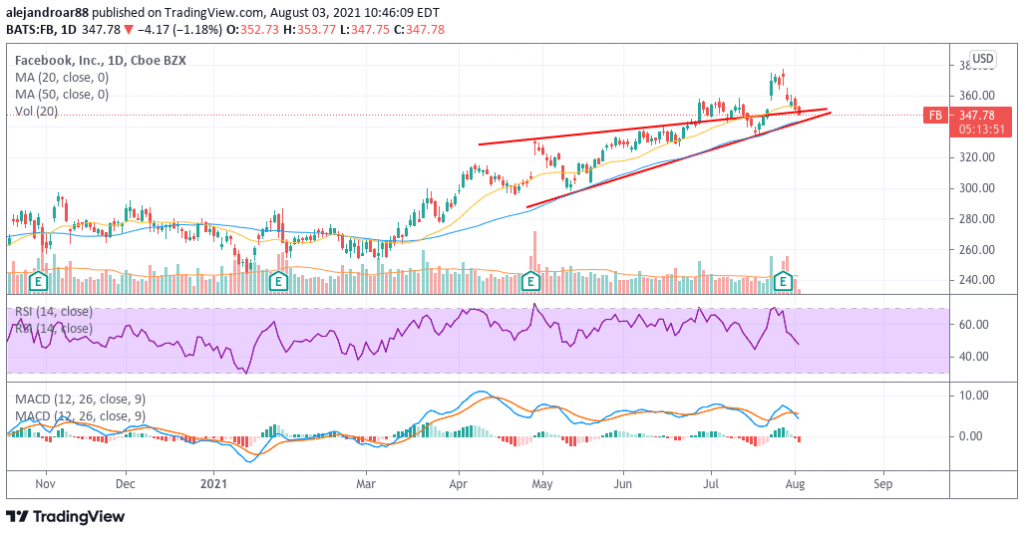

#1 – Facebook (FB)

The price of Facebook’s stock was severely hit after the company published its quarterly results, with shares diving as much as 4% on the day the report was published amid concerns that the firm’s growth rates could be decelerating.

For a company of the size of Facebook, a deceleration of this nature is not necessarily a bad omen considering that the parent company of Instagram already brings as much as $100 billion in revenue per year – a figure that only a handful of companies is able to produce.

Meanwhile, it is important to note that the firm experienced an important tailwind resulting from pandemic lockdowns and that created a higher comparative baseline for its future results.

Interestingly, Facebook’s path to future growth seems to be heavily tied to the development of a “metaverse” – a virtual version of the world through which individuals will interact in the future.

The firm’s successful pivot toward this innovative approach is quite promising and could bring further growth for the tech company. Based on how successfully its Chief Executive Mark Zuckerberg has executed its vision for social media, I wouldn’t bet against him in his path to turn Facebook into the leading force of this up-and-coming virtual environment.

Currently trading at only 25 times its forward earnings per share while boasting elevated profit margins and a conservatively financed balance sheet, Facebook remains a bargain for those willing to wait until the market comes to its senses.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#2 – JD.com (JD)

Best known as the Amazon of China, JD stock has been battered by the latest wave of hostile regulatory actions taken by the Chinese government toward the tech sector and other corners of the market as well.

However, this headwind has opened up an opportunity to buy a growing business at a fairly low price and even though risks of a severe crackdown remain on the table, the margin of safety at the moment seems to be high enough to classify JD.com as a potentially undervalued stock.

In this regard, JD’s profit margins have been going up progressively, with net margins swinging to positive territory in 2019 at 2% and surging to 6.5% by the end of 2020.

Meanwhile, the company’s diluted earnings per share have moved from $0.59 per share in 2019 to $2.44 last year as a result of the pandemic tailwind while they are expected to decelerate to $0.87 by the end of 2021 to then pick up their pace to $1.63 in 2022 and $2.37 per share.

Based on those estimates, which seem fairly conservative based on the company’s latest track record, JD.com is being valued at 81 times its forecasted earnings per share for this year.

Even though this multiple seems fairly stretched, the company is being valued at $110 billion even though it is expected to bring a quarter of the earnings that its US peer (Amazon) does at some point in the future.

Despite these regulatory headwinds, the company’s valuation seems fairly conservative if we use that of Amazon as a plausible comparable and it would be fairly possible to see the market capitalization of this company at least tripling once the dust settles.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#3 – Logitech (LOGI)

Shares of this Swiss tech and gaming equipment manufacturer took a beating after it revealed its quarterly earnings a few days ago as market participants seem to have priced in too much optimism for the company’s post-pandemic performance.

However, nothing really changed for the business in terms of its fundamentals and growth prospects while its gross margins remained above historical averages.

Moving forward, the company expects flat revenue growth – which is not that bad considering that the firm has moved to a higher plateau as it is now reporting quarterly revenues above $1 billion amid a surge in the demand for its products during the pandemic.

The tailwind provided by the virus crisis, which includes higher demand for gaming products and video conference equipment, seems to be enduring and could keep the company’s profits and revenues at elevated levels for longer than the market expects.

Last year, earnings per share landed at $5.51 but estimates see a 28% drop in those numbers this year at $3.97 per share. If that is not the case and the firm maintains its EPS near last year’s levels, Logitech would only be trading at around 20 times its 2020 EPS – a highly conservative multiple for a company that has no debt and that plans to deploy as much as $1 billion in buying back shares in the near future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

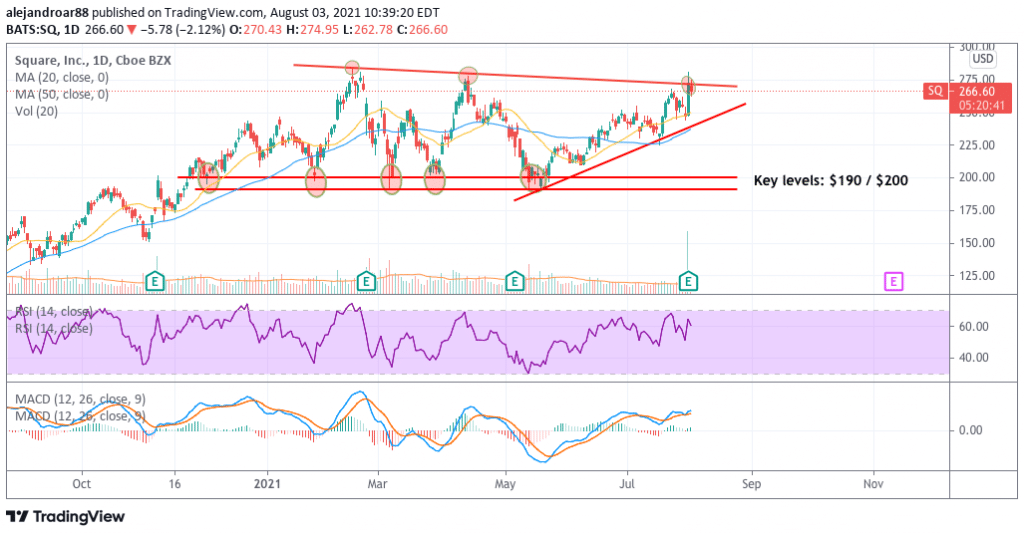

#4 – Square (SQ)

Yesterday, Square announced that it will be acquiring the Australian firm AfterPay as part of its effort to set its foot in the growing “buy now, pay later” market. The company will be giving up as much as 18.5% of its equity to complete this transaction and the market reacted quite positively as the fintech business led by Twitter’s founder Jack Dorsey is progressively becoming the Mastercard and Visa of both traditional and online retail.

Only days before this announcement, the company also said that it will be offering financing to the small businesses within its Seller ecosystem – effectively opening up a brand new revenue stream that could further boost the firm’s top-line results moving forward.

Meanwhile, during the second quarter of the year, Square reported $1.96 billion in revenue excluding its Bitcoin dealings resulting in $3.5 billion in revenue brought in during the first six months of the year.

Based on a simple run rate of these results, Square is being valued at approximately 17.5 times its 2021 sales without accounting for the impact that the AfterPay transaction will have on the firm’s top-line results.

At the moment, both Visa (V) and Mastercard (MA) are trading at around 24 times their 2020 revenues while their growth prospects are fairly less attractive than those of Square. In light of those peer comparables, if Square manages to keep pushing its revenues closer to those of Mastercard, which could happen in only a few years, the combination of higher multiples and higher sales could result in a significant expansion of the firm’s valuation – possibly eyeing the $300 billion mark as a plausible target.

67% of all retail investor accounts lose money when trading CFDs with this provider.

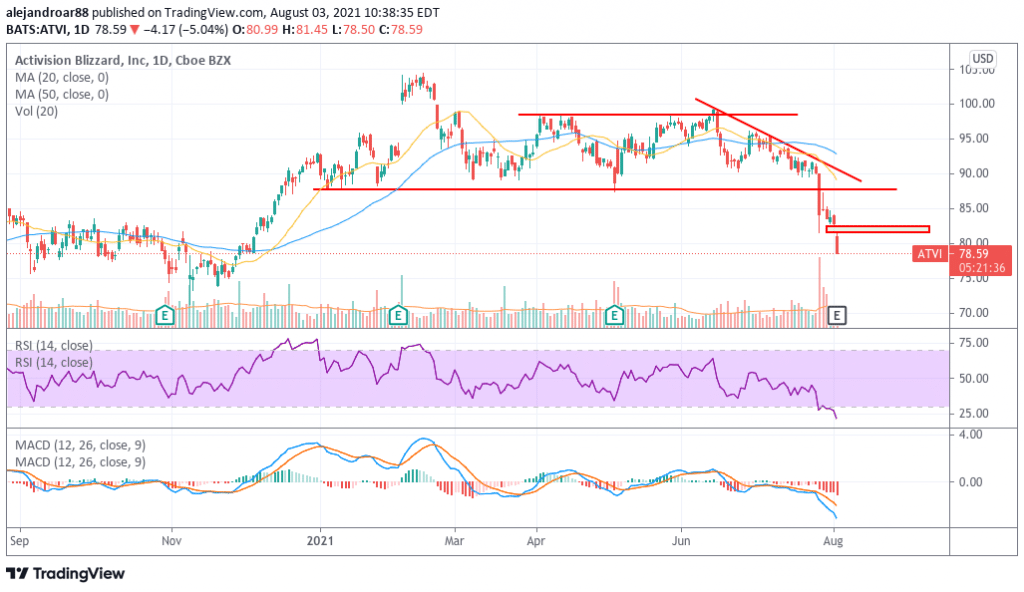

#5 – Activision Blizzard (ATVI)

Activision shares have been dropping significantly amid controversies about its workplace environment and a recently approved compensation package granted to its Chief Executive.

As a result, the stock is trading almost 25% below its 52-week high while it is dropping 4.3% this morning amid news of multiple class-action lawsuits being brought up against the company on sexual harassment claims and other accusations.

Even though this headwind could do a fair share of damage to the business bottom-line results in the short term in the form of higher legal expenses, the company’s value proposition, brands, and business model remain fairly robust.

At a market capitalization of $65 billion, Activision is trading at only 29.5 times its 2020 net earnings and that seems like a fairly conservative multiple for a company that is favorably positioned to exploit multiple growing trends in the gaming space including augmented reality and the metaverse.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Buy Stocks at Cedar FX, the World’s #1 trading platform!