5 Best Industrial Stocks to Invest for July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

With most developed economies around the world now fully engaged in the process of reopening, industrial stocks have gained strongly this year as reflected by the performance of the SPDR Select Sector Industrial ETF (XLI), which has advanced 17.4% in 2021.

Multiple themes and pandemic-related tailwinds have helped these companies in thriving during the health crisis and some of those catalysts may outlive the virus situation, which results in more potential upside ahead for a selected group of industrial names.

The following five names display decent valuation metrics and interesting growth prospects based on the opportunities that have been presenting in the individual markets they serve.

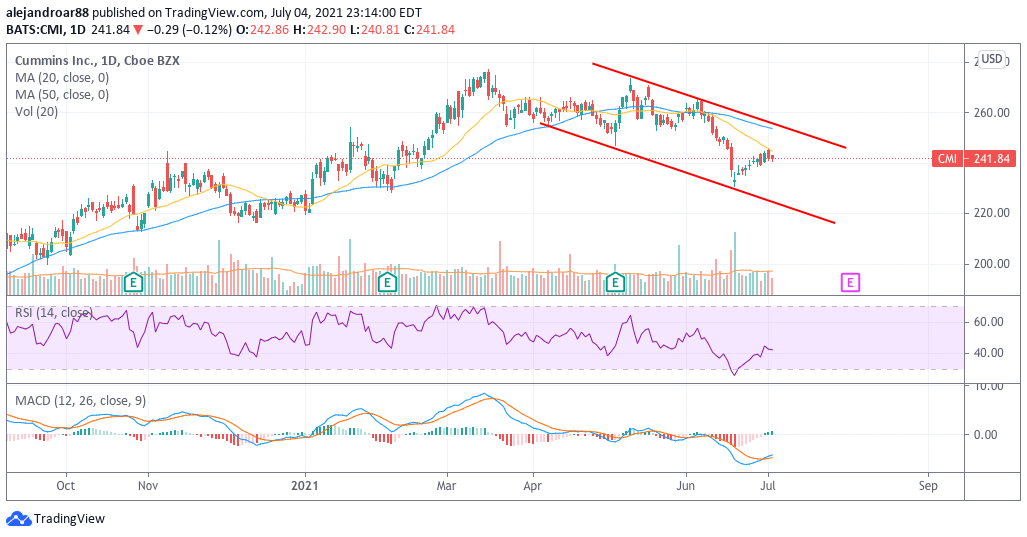

1. Cummins (CMI)

Founded in 1919, Cummins is one of the world’s largest suppliers of specialized diesel and gas-powered engines, currently generating over $21 billion in sales while employing over 57,000 people worldwide.

Before the pandemic stroke, the company’s track record of sales growth was decent, with top-line results growing from $19.1 billion in 2015 to $23.57 billion by the end of 2019 at a 5.4% compounded annual growth rate (CAGR).

Meanwhile, Cummins’ gross profit margin has remained steady between 24% and 25% while net margins have been improving lately as they moved from 7.3% in 2015 to 9.6% by the end of 2019.

The company’s long-term debt landed at approximately $4 billion by the end of the first quarter of 2021 while cash and equivalents ended the period at roughly $3.4 billion which results in a fairly small net debt of $600 million that represents only 23% of the company’s annual EBITDA generated in 2020.

In the past four years at least the company has managed to generate free cash flows of over $2 billion, which results in an estimated price-to-cash-flow metric of 18.

This cash flow generation capacity is providing ample coverage for the firm’s 2.2% dividend yield while Cummins has also used the cash to buy hundreds of millions in stock every year. Last year alone they bought $640 million while in 2019 the company bought back as much as $1.27 billion.

The combination of these buybacks, the company’s decent dividend yield, and its strong pre-pandemic revenue growth make Cummins a fairly attractive industrial company for value investors who like to invest in strong and well-reputed brands.

67% of all retail investor accounts lose money when trading CFDs with this provider.

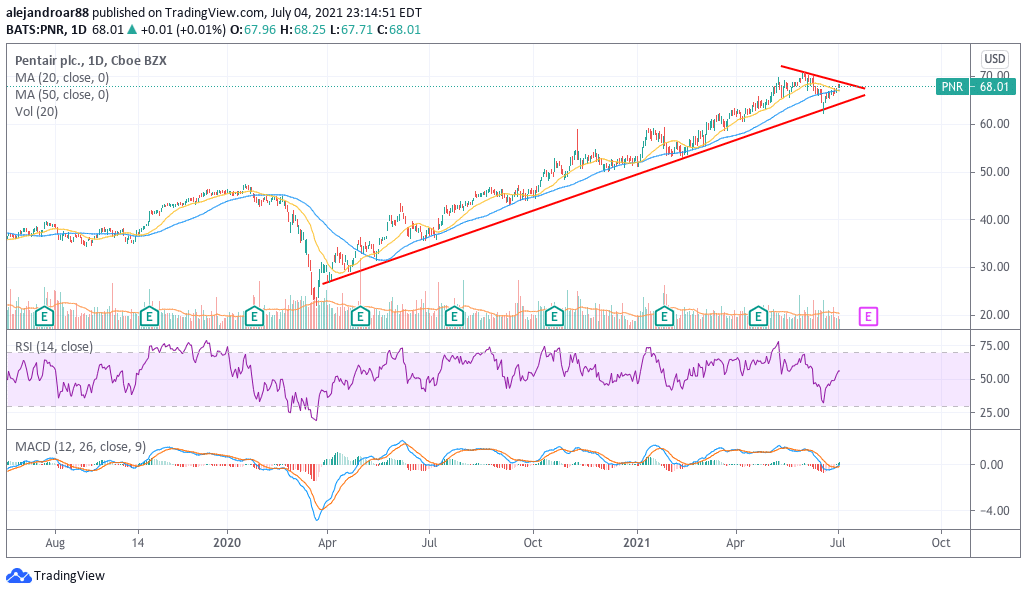

2. Pentair (PNR)

Pentair is a UK-based company that provides pool equipment and solutions for residential customers primarily, with most of its sales coming from the United States. Last year, the company sold $3.2 billion while it employed almost 10,000 people.

Pentair’s business had been declining for years until the pandemic stroked as consumers invested more money into improving their homes during lockdowns. Meanwhile, analysts expect a sustained surge in construction volumes due to higher demand for homes while demand from the commercial segment should continue to pick up as economies around the world keep reopening.

Last year, annual sales jumped above the $3 billion threshold for the first time since 2016 while the company managed to maintain its gross profit margins above 35% – in line with historical averages. Moreover, net margins landed at 12%, also in line with the performance seen in the two years preceding the virus crisis.

By the end of the first quarter of 2021, Pentair had almost $1 billion in long-term debt on assets of $4.4 billion including $100 million in cash and equivalents. Around $2.4 billion of those assets were goodwill.

Based on analysts’ forecasts, as compiled by Koyfin, sales should continue to grow to $3.7 billion by the end of 2022 which results in a forward price-to-sales ratio of 3 on a market capitalization of $11.3 billion.

Moreover, earnings per share are expected to land at $3.41 by the end of that same year, which results in a forward P/E ratio of 20 on an estimated annual growth rate of 17% for the firm’s earnings. That results in a fairly conservative price-to-earnings-to-growth ratio of 1.2.

Based on a potentially long-lasting tailwind caused by the pandemic in the form of higher demand from residential customers and a sustained pick-up in the demand from the commercial sector, chances are that Pentair’s valuation multiples could expand if more positive results start to come in.

67% of all retail investor accounts lose money when trading CFDs with this provider.

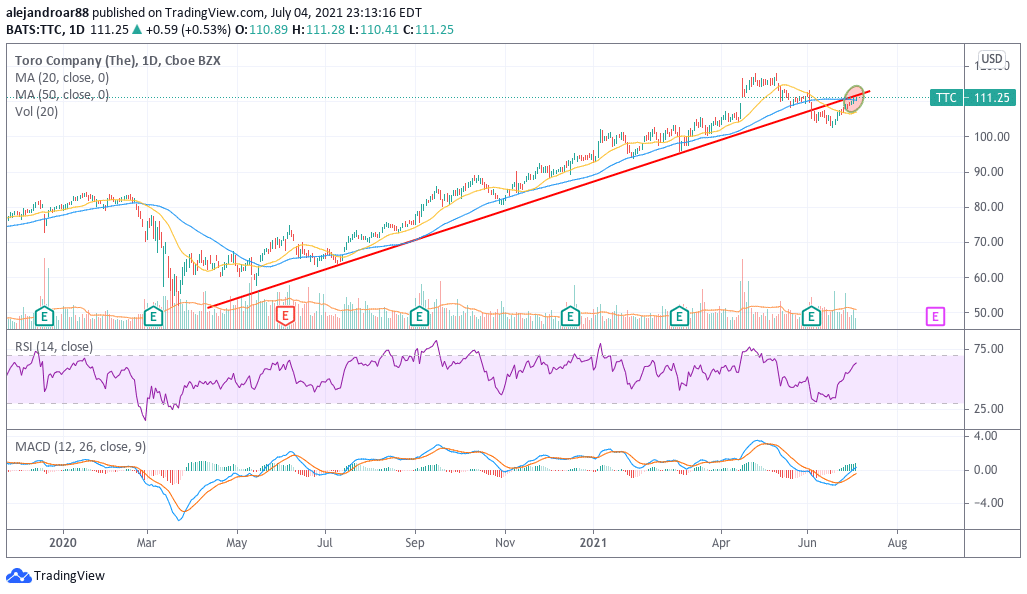

3. The Toro Company (TTC)

The Toro company specializes in providing turf equipment and irrigation solutions for residential and commercial clients all across the world, currently employing over 10,000 people to run its operations while selling almost $4 billion a year.

The company has managed to grow its sales steadily in the past five years, with top-line results moving from $2.39 billion in 2016 to $3.4 billion by the end of last year. Turf equipment was in high demand during the pandemic amid higher volumes sold to residential customers, which offset the decline in other segments including landscaping and professional solutions.

Since most of the sales made by the company come from the United States – around 80% as of last year – it would be plausible to see the company’s commercial segments recovering now that the pandemic is becoming an item in the rearview mirror.

Meanwhile, the tailwind that pushed residential sales higher during the pandemic could outlive the health crisis amid the implementation of hybrid work methodologies by companies in the US as well.

By the end of 2021, Toro had almost $700 million in long-term debt on long-term assets of almost $3 billion that include a fairly small amount of goodwill ($412 million) considering the number of acquisitions the firm has made. The remaining $520 million in intangibles are mostly associated with customer relationships and other valuable areas of the core business.

By the end of last year, free cash flows for Toro landed at $460 million, which results in a P/FCF multiple of 26. Meanwhile, analysts are estimating that earnings per share should land at around $4.45 per share by the end of 2023 which would result in a forward P/E multiple of 25.

That results in a price-to-earnings-to-growth multiple of almost 2 based on a forecasted annual growth rate of 13% for the company’s earnings.

Although this company is not particularly cheap at current levels, the chart above shows that a long-dated uptrend has been broken and was retested just last Friday. If that area of support becomes resistance, chances are that this high-quality stock could experience a short-term pullback that could open up a window for investors to enter a long position at a more reasonable valuation.

67% of all retail investor accounts lose money when trading CFDs with this provider.

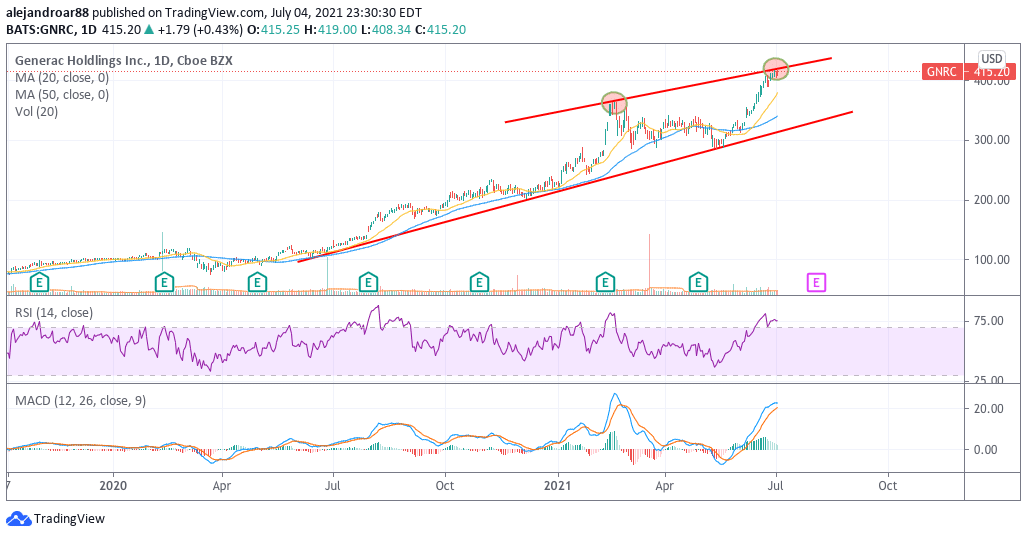

The Final 2: Generac Holdings (GNRC) & Trex Company (TREX) – Growth among industrials

Generac’s business has been booming for years, with sales moving from $1.32 billion in 2015 to as much as $2.49 billion by the end of last year at a 13.5% CAGR. Meanwhile, the company has managed to improve both its top and bottom-line profitability, with gross margins moving from 35% to 39% while net margins jumped from 6% to 14% during that same period.

A fairly conservative balance sheet and analysts’ expectations of strong earnings growth for the next two to three years have currently pushed the forward P/E ratio of this firm to 40. However, this number seems fairly conservative for a company that has managed to grow its earnings at a 37.5% CAGR in the past five years.

67% of all retail investor accounts lose money when trading CFDs with this provider.

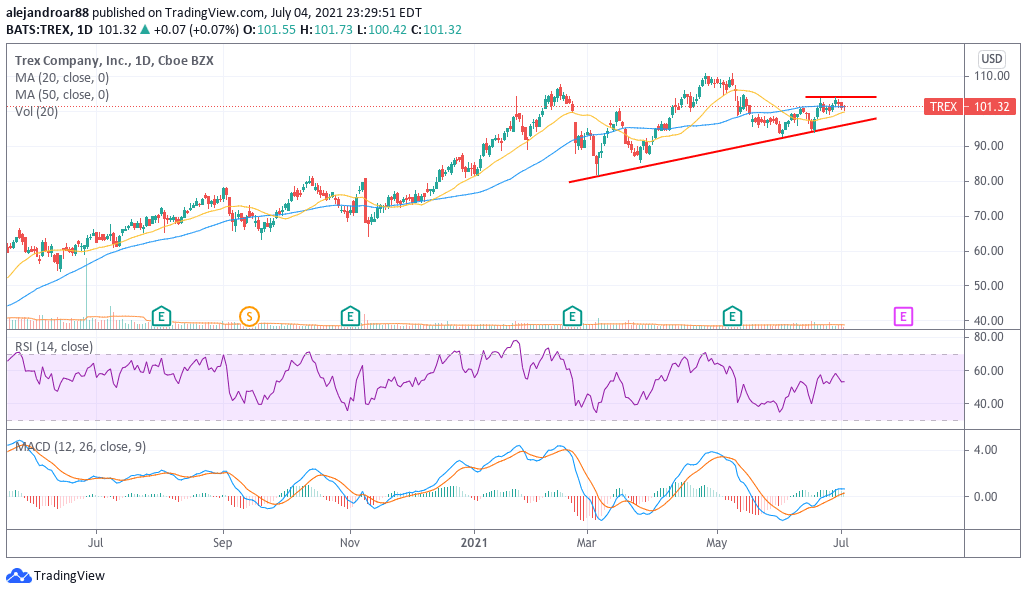

Similarly, Trex Company (TREX), a business that manufactures wood and plastic products for decking and railing applications, exhibits a similar pattern of strong revenue growth, with revenues doubling in the past 5 years from $440 million to $880 million (15% CAGR), while earnings per share have grown from $0.38 to $1.52 at a 32% CAGR during that same period.

However, for this company, the balance sheet situation is even better as Trex has no long-term debt, which is possibly the reason why its P/E ratio is a bit higher than Generac’s at 47 as analysts expect a 36% jump in its bottom-line results this year.

Buy Stocks at eToro, the World’s #1 trading platform!