5 Best Healthcare Stocks in August 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The healthcare sector has been one of the most benefitted by the pandemic as drugmakers, clinical research companies, and biotech firms have experienced a significant uptick in the demand for their products and services in the race to find a vaccine and effective treatments for the COVID-19 virus.

Even though vaccines are already being rolled out across the world and the virus crisis might eventually become an item in the rearview mirror, multiple companies in this sector will emerge from the contingency stronger and better amid the rapid expansion that they have experienced during the health emergency.

In the following article, I’ll share five picks in this sector that may be poised to deliver further upside even once the pandemic tailwind is no longer on the table.

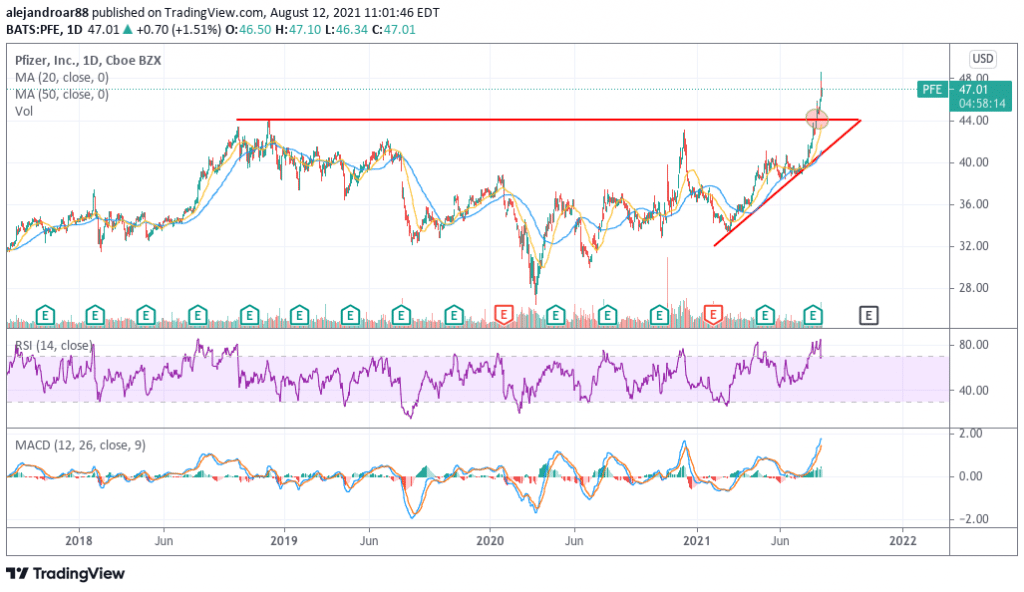

#1 – Pfizer (PFE)

Formerly deemed an excellent dividend pick, Pfizer shares are now becoming an appealing option for value investors amid the outstanding results the firm has been delivering recently on the back of higher vaccine sales.

On 28 July, the company reported its quarterly results covering the second quarter of the year, with Pfizer almost doubling its top-line results compared to the same period a year ago at $19 billion while adjusted earnings per share landed at $1.07 or 9 cents above the consensus estimate for the period.

Meanwhile, the company increased its guidance for the year to around $80 billion in revenues and $4.05 in adjusted EPS up from previously forecasted figures of $72.5 billion and $3.65 per share respectively.

At a price of $47 per share, Pfizer is trading at only 12 times that forecasted EPS while the firm is offering an attractive 3.2% dividend yield that could eventually be lifted as a result of above-expected free cash flows.

Moreover, the market seems to be expecting that this pandemic tailwind may eventually fade. However, due to the potentially seasonal nature of the COVID-19 virus, chances are that revenues for the pharmaceutical giant could remain above its historical averages for longer than expected.

67% of all retail investor accounts lose money when trading CFDs with this provider.

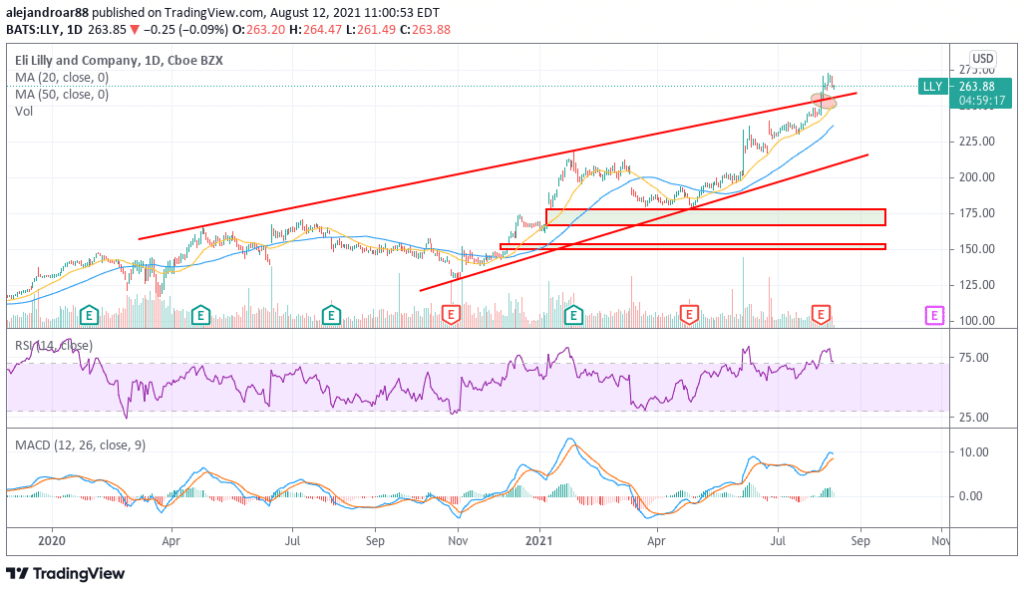

#2 – Eli Lilly Corporation (LLY)

Eli Lilly stock is one of the top-performing names in the health care sector this year, with the company delivering a 58% gain to investors so far in 2021 on top of the 31% advance it reported in 2020.

On 3 August, the company reported a solid second quarter with sales topping estimates by $150 million as they landed at $6.74 billion while earnings per share came in at $1.87 per share or 2 cents below analysts’ estimates.

Eli Lilly’s track record of revenue and profit growth makes it a top pick in this space as revenue growth has been accelerating lately with top-line results expected to jump by around 11% this year.

Moreover, diluted earnings for the company have also progressively grown from $3 per share back in 2018 to an estimated EPS of $8 per share this year resulting compounded annual growth rate of 38.7%.

Currently trading at a forward P/E multiple of 33, Eli Lilly qualifies as an undervalued stock based on its historical and forecasted earnings growth rate.

67% of all retail investor accounts lose money when trading CFDs with this provider.

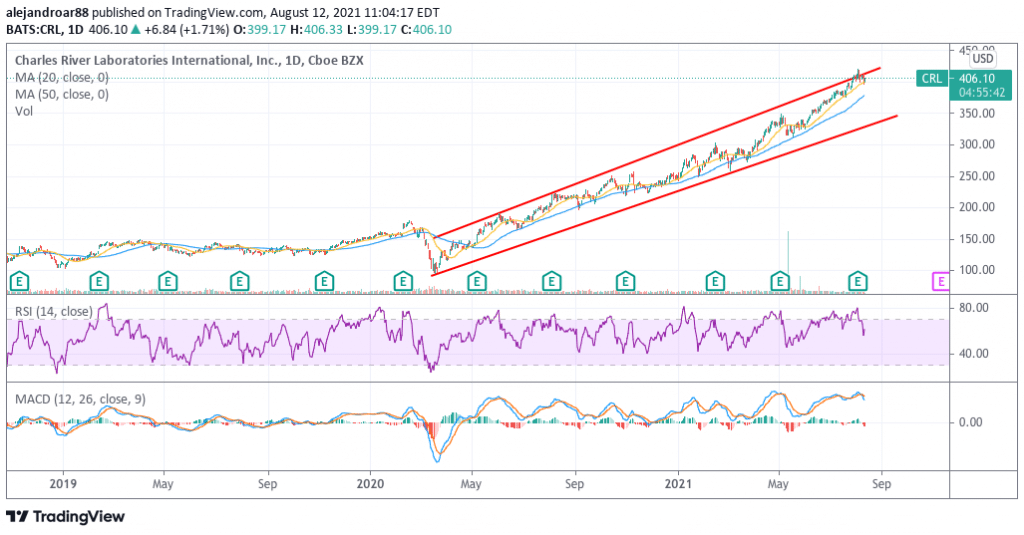

#3 – Charles River Laboratories (CRL)

The performance of Charles River stock this year has also been remarkable, reporting a 62.6% gain so far in 2021 on top of an impressive 64% advance last year.

The Wilmington-based healthcare company has been delivering solid revenue growth in the past three years, with top-line results growing from $2.27 billion back in 2018 to $2.92 billion last year at a 13.4% CAGR while this year’s revenue growth is expected to accelerate to around 22.5% according to the management’s guidance.

Moreover, bottom-line results have also been surging in the past few years, moving from $4.6 per share back in 2018 to $7.20 per share in 2020 while the management shared an EPS guidance of $10.35 for 2021 resulting in a 27% leap compared to the adjusted figures reported a year ago.

Currently trading at 38 times its forecasted earnings per share for the next twelve months, this company presents itself as a top growth pick within the healthcare sector amid the rapid expansion of both its revenues and earnings on the back of the positive momentum that the demand for its services has been experiencing. increased demand from the biotech sector.

67% of all retail investor accounts lose money when trading CFDs with this provider.

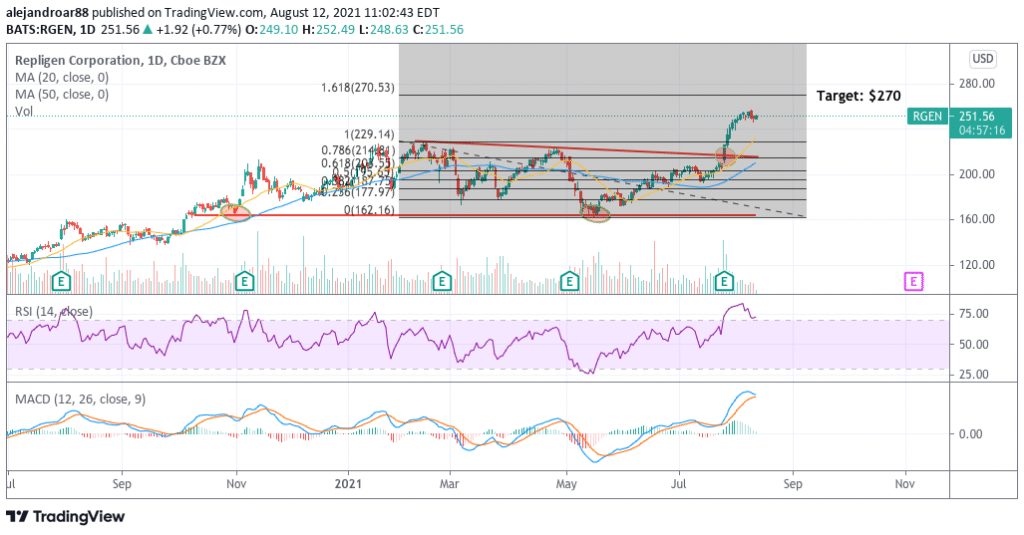

#4 – Repligen Corporation (RGEN)

With shares more than doubling in 2020 while surging another 30% or so this year, Repligen is another top growth pick that can hardly go unnoticed amid the increased demand that the firm’s services have experienced lately and could continue to see in years to come.

During the second quarter of the year, the company reported revenues of $163 million, effectively beating the Street’s estimates by more than 10%, while non-GAAP earnings per share landed at $0.79 or nearly 50% above the consensus estimate for the period.

Moving forward, Repligen’s management is expecting to see revenues landing at around $645 million this year while non-GAAP EPS are expected to come in at $2.78. Based on that estimate, the stock is being valued at 90 times its forecasted EPS for this year at the current price of $252 per share.

Even though that multiple seems fairly stretched, it is important to note that the company’s earnings have nearly tripled in the past two years and they are expected to more than double this year alone.

Based on the rate at which the business is growing, this multiple seems fairly justified and even though analysts are expecting a deceleration in these growth rates as the world steps out of the pandemic, the company had already been growing at a similar pace when this tailwind was absent.

On top of that, Repligen has no long-term debt, over $700 million in cash, and has been generating positive free cash flows consistently in the past three years at least. This robust financial position should help the firm in expanding its operations further either through the acquisition of other businesses or through the organic expansion of its current operations.

67% of all retail investor accounts lose money when trading CFDs with this provider.

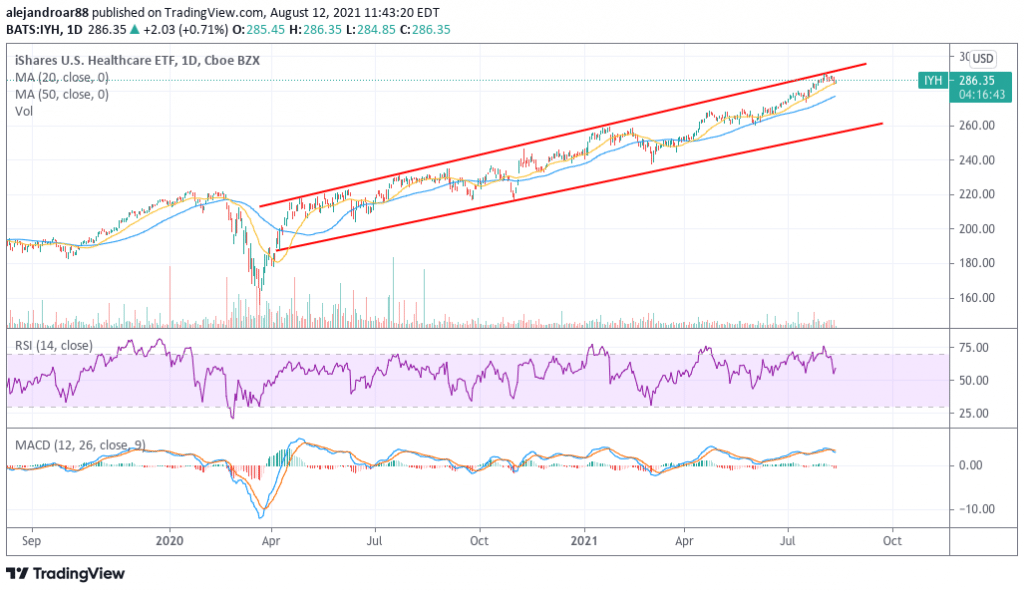

#5 – iShares US Healthcare ETF (IYH)

For those who prefer to take a more conservative approach when investing in this promising sector of the economy, the iShares US Healthcare ETF (IYH) focuses on investing in companies within this sector based in the United States.

According to data from ETF Database, the fund currently invests in 129 different companies while its top ten holdings at the moment account for 46% of its portfolio. These top ten holdings include Johnson & Johnson (JNJ), UnitedHealth Group (UNH), Pfizer (PFE), and Abbott Laboratories.

In 2020, IYH delivered a 15.6% gain to investors while in 2021 its value has already moved 17% higher. On top of that, the ETF currently offers an attractive 1% dividend yield.

The fund currently oversees $2.92 billion for investors while it charges a 0.43% annual expense ratio.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Buy Stocks at Cedar FX, the World’s #1 trading platform!