Looking beyond rate rises as 2015 looms

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Despite a point in mid-week when it looked like the dollar might finally be in for a real correction, the dichotomy of economic performance between the US and most of the rest of the world appears to be growing once again.

The notes from the Federal Markets Open Committee on Wednesday caused a real retracement in the dollar across several currencies, the like of which has not been seen in several months. Over the course of an hour, the pound gained 128 pips against the dollar; AUD gained 91 and the yen 52. The euro managed to gain 89 pips in just over 30 minutes.

Despite a point in mid-week when it looked like the dollar might finally be in for a real correction, the dichotomy of economic performance between the US and most of the rest of the world appears to be growing once again.

The notes from the Federal Markets Open Committee on Wednesday caused a real retracement in the dollar across several currencies, the like of which has not been seen in several months. Over the course of an hour, the pound gained 128 pips against the dollar; AUD gained 91 and the yen 52. The euro managed to gain 89 pips in just over 30 minutes.

Underlining the lack of evidence for a rate rise, communicating that any change in policy would not come as a surprise or ahead of schedule, and forecasting weaker US growth thanks in part to the strong dollar had its desired effect: but not for long.

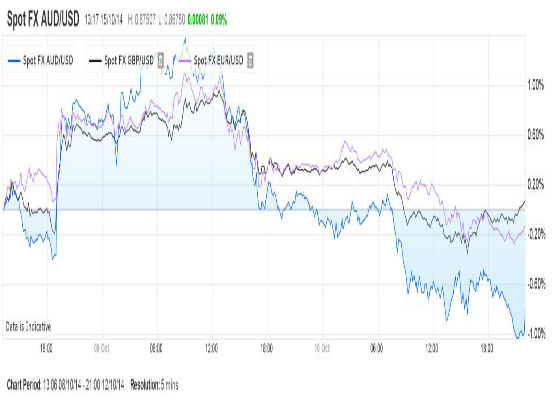

A combination of bad economic news from Germany, hawkish comments from key Federal Reserve committee members that appeared to contravene Janet Yellen’s doctrine, and the continued bullish endeavours of the markets ensured that the dollar started this week in a very similar position to last, as demonstrated by the chart (from IG’s global forex trading system) that shows AUD, GBP and EUR retracing gains made on Wednesday October 8 by Sunday 12..

Indeed, those in Australia, the eurozone or the UK could be forgiven for wondering whether the Fed minutes’ release actually happened and wasn’t dreamt. At 9am on Monday morning, the Australian dollar was just a couple of pips higher than it had been a week before. The pound and euro were both down; only the yen had made a gain against the dollar. The yen’s ability to buck the trend of dollar strength in the past couple of weeks has been remarkable, and possibly due to worries over international conflicts and the continuing horror of the Ebola outbreak.

Unless it becomes unmistakably clear that the US will not be the first major economy to instigate a rate rise, it appears that the dollar will continue to grow in the long term. And the markets seem extremely reluctant to pay heed to any other situation.

Pay heed they should, though. There are several other factors that will affect the markets in a major way come 2015. The long period of low interest rates that will shortly come to an end is unprecedented, and its repercussions will be far and wide.

It also became yet clearer last week that economies over most of the world are currently lagging someway behind the US. In a situation perhaps unthinkable at the beginning of the year, Germany is facing recession once more and desperately needs some positive economic news to improve its outlook. Germany underperforming makes the entire eurozone look even weaker, with Italy, France and Spain all written off as saviours for the region.

Of course, for most that will only push the dollar higher, as it becomes the only currency to benefit from higher interest rates. But there are other sides to the story. The US has been here before, with strong dollar runs in both the 80s and 90s eclipsing its current move. Studies have shown that those runs led to a decrease in manufacturing jobs, which in turn led to a suspicion that other economies were taking American jobs off of the back of weaker currencies. With so many other currencies currently in a position to do just that, allowing the dollar to gain even more strength could be problematic for both the Federal Reserve and Barack Obama.

And it isn’t just the eurozone that’s proving to be weaker than expected in 2014. Growth in key Asian markets has been seen to be slowing markedly faster than expected. Commodity trading is seeing all-time lows for key metals, food and oil. Whilst the dollar’s strength is currently a boon to many central banks, if it becomes completely dominant the story may change, and the US could start facing problems. A rate rise would compound the issue: debt is still very much a part of every country’s balance sheet, so raising rates could have the duel impact of both drastically increasing the value of the dollar and making other countries debt worse.

That picture becomes even starker in emerging economies, where the capital competition that would arise in the US would hugely undermine growth. Any rate rise in the US would cause an exodus of capital from emerging economies, forcing them to undertake drastic measures to keep investors interested. Not only could that exacerbate many of the issues already underlined, it could also have wider political and social implications that the US will be keen to avoid.

The story that was set out for 2014 – where markets blossomed as confidence, strength and capital returned to economies and equities – has so far failed to materialise. To assume that it will in 2015 is dangerously short sighted, especially as there is a raft of political, economic and market-led issues that do not look likely to be resolved anytime soon.

Spread bets and CFDs are leveraged products and can result in losses that exceed your deposits. The value of shares, ETFs and ETCs bought through a stockbroking account can fall as well as rise, which could mean getting back less than you originally put in.

This information has been prepared by IG, a trading name of IG Markets Limited. The material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.