5 Best Stocks to Buy Q3 2021 – The Rise of Tech

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The pandemic has accelerated the pace at which mankind has adopted technology for multiple purposes going from how we work to how we entertain ourselves as lockdowns forced us to rely on digital solutions to an extent not seen before the contingency.

Meanwhile, multiple reports from top-notch consulting firms like McKinsey & Company have highlighted that this shift may outlive the pandemic as both individuals and businesses have come to know the benefits of relying on technology to shop, work, entertain, and interact.

As we move forward into this decade, it seems that tech companies may continue to grow at an accelerated pace which is why the following selection of the five best stocks to buy during the third quarter of 2021 will be primarily focused on the tech firms that stand out from the crowd amid their relentless growth, strong fundamentals, and promising future prospects.

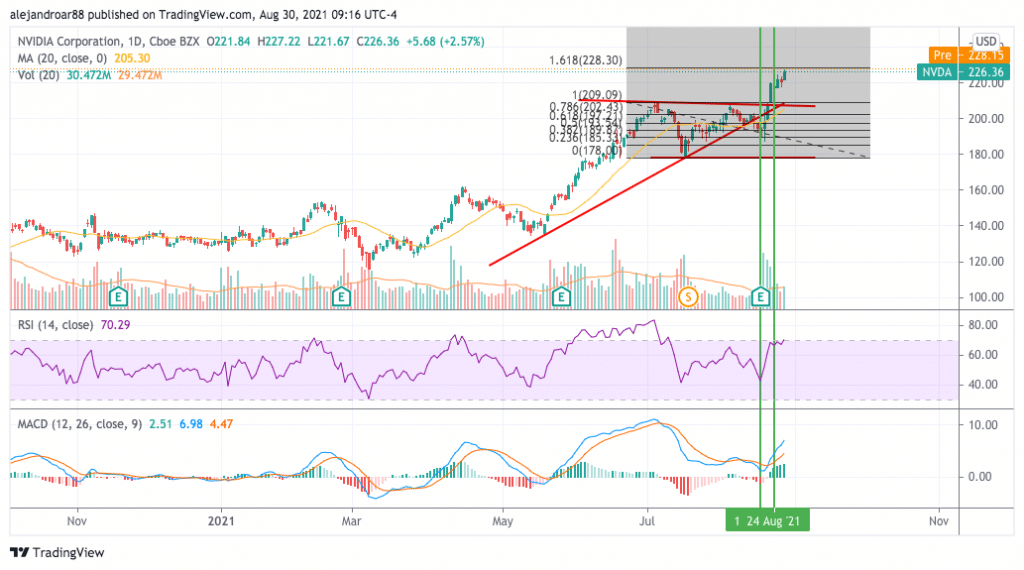

#1 – Nvidia (NVDA)

NVIDIA’s top-line results have been growing at a fast pace in the past four years at least, with the company more than doubling its sales during that period amid a significant rise in the demand for many of its products from consumers, data centers, cryptocurrency miners, and automotive companies.

Last year, sales of NVIDIA jumped 53% amid a strong pandemic tailwind that resulted in an ongoing global chip shortage. This temporary situation is allowing the firm to ramp up its prices while, even though such an imbalance might be resolved soon, its products may continue to experience above-average demand amid the rise of multiple positive markets including cloud services, cryptocurrency mining, gaming, and the metaverse.

Moreover, the company’s gross margins have been progressively improving, moving from an average of 60% before the pandemic to nearly 64% last year. Even though its bottom-line profitability has not displayed the same positive trend, the company is still fairly attractive on this particular front as its net margins have stood above 30% lately while its return on equity (ROE) in the past twelve months currently stands at 40%.

Only a few weeks ago, the company made an interesting announcement about its steps to become a leading provider of solutions for the up-and-coming metaverse market. Through a solution called the Omniverse, Nvidia has launched a platform on which developers can build simulated real-time experiences in 3D.

This solution will possibly enable businesses to provide augmented and virtual reality experiences to consumers in the future and may open a promising new revenue stream for the Santa Clara-based chipmaker.

So far this year, NVIDIA has delivered gains of 73.5% to investors on top of the 122.3% advance the stock experienced last year – a performance that highlights its strong positive momentum.

At the moment, the stock is trading at 52 times its forecasted adjusted earnings per share for the next twelve months. Moreover, the firm is trading at an EV/EBITDA multiple of 96 while its EBITDA has been growing at a 28% CAGR. Based on these multiples, NVIDIA seems to be a reasonably valued business based on its past earnings growth and promising future prospects.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#2 – Facebook (FB)

Facebook has become a poster child of how technology can revolutionize the world as we know it as the company has developed a platform through which people can interact, shop, share common interests, and keep themselves up to date with the most recent developments around the world.

Facebook’s social media platform currently has nearly 3 billion monthly active users (MAUs) while Whatsapp and Instagram have 2 billion and 1.4 billion MAUs as per the latest data released by the company.

As a result of its remarkable growth, the company headed by Mark Zuckerberg has more than tripled its sales in the past four years, moving from $27.6 billion to $85.6 billion from 2016 to 2020.

On the profitability front, even though gross margins have been declining, the company has managed to maintain positive bottom-line profitability ratios above the 45% level (EBITDA margin) and 30% level (net margin).

Moreover, its return on equity (ROE) has also landed above the 20% level for multiple years and has even hovered above the 30% threshold recently.

Facebook has recently made interesting announcements about its plans to set a footprint in the up-and-coming metaverse market and the company’s successful deployments of multiple solutions such as Messenger and WhatsApp Business increase the odds that it might become a dominant force in this promising yet-to-be-developed space.

The company’s valuation has been recently impacted by regulatory pressures in multiple corners of the world concerning the firm’s data privacy practices and monopolistic behavior.

As a result, Facebook is trading at an attractive forward P/E multiple of 26 while its LTM EV/EBITDA multiple is standing at 18.6 despite both its adjusted earnings per share and EBITDA have been growing at a CAGR of around 27% in the past four years.

The combination of this conservative valuation, a robust balance sheet, and promising growth prospects make Facebook one of the most attractively valued businesses in the mega-cap tech space at the moment and that makes it one of the best stocks to buy in Q3 2021.

67% of all retail investor accounts lose money when trading CFDs with this provider.

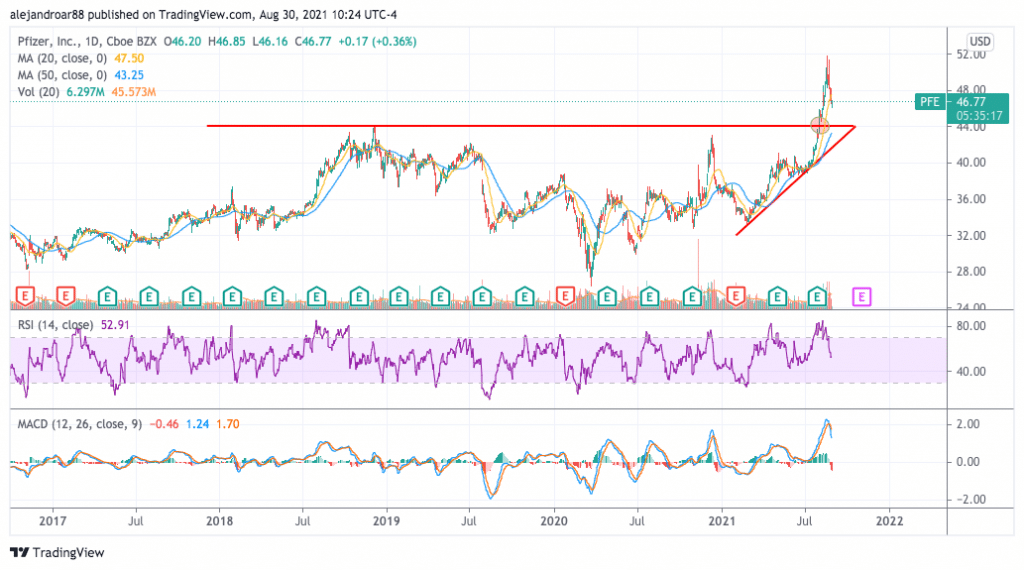

#3 – Pfizer (PFE)

Pfizer shares have been on an uptrend since the firm released its financial results covering the second quarter of its 2021 fiscal year as the company has managed to reverse a former downtrend in its top-line results on the back of eye-popping COVID-19 vaccine sales.

In its latest quarterly report, the company said it expects to see its revenues rising to around $80 billion this year, more than twice what the company sold the previous year, of which $33.5 billion are expected to come from the sale of its BNT162b2 COVID vaccine developed alongside the German biotech company BioNTech.

Moreover, Pfizer’s adjusted diluted EPS is expected to land at around $4.05 by the end of 2021 resulting in a 234% jump compared to the figure reported in 2021 while this number should probably allow the company to declare either a special dividend or significantly increase its upcoming quarterly dividend.

At its current price of $46.6 per share, the stock offers an appealing 3.4% dividend that was already fairly sustainable based on its past cash flow generation capacity while it may be deemed as rock solid now as cash inflows will likely surge this year amid these higher top-line volumes.

Moreover, the company is being valued at only 11 times its forecasted earnings for the next twelve months, possibly as analysts are expecting a significant deceleration in the company’s growth once the pandemic is over.

However, with billions of people around the world still in dire need of a vaccine, chances are that these COVID-related revenues will likely keep Pfizer’s top-line results above their pre-pandemic levels for longer than the market seems to be expecting.

Additionally, improved financial conditions may give the firm a much-needed boost to further ramp up its dividend distributions. This situation could lead to a sustained appreciation in its share price moving forward.

All things considered, Pfizer appears to be both a great value and dividend stock pick and that is why it made its way to this list of best stocks to buy in Q3 2021.

67% of all retail investor accounts lose money when trading CFDs with this provider.

#4 – FuboTV (FUBO)

FuboTV is an up-and-coming player in the growing video streaming industry that specializes in broadcasting sports content – primarily soccer.

All of the company’s metrics have been displaying a consistent uptrend starting with its revenues, which have moved from $4.3 million back in 2019 to $218 million in 2020 while the management guided for sales of $565 million for this year.

Meanwhile, the number of subscribers is expected to triple during that same period from 316,000 to 915,000 while average revenues per user (ARPU) have been steadily rising from around $50 to nearly $72 per subscriber from Q2 2019 to Q2 2021.

Moreover, the firm’s adjusted EBITDA margin, which adds back non-cash expenditures, has been improving from minus 140% in Q2 2019 to minus 36.2% by the end of Q2 2021.

Multiple factors make FuboTV an attractive long-term growth pick. First, the company is trading at a conservative price to sales multiple of 7 even though its sales have been growing by the triple digits.

Moreover, the management has already shown that it can deliver on its promises as reflected by the broadcasting deals it has signed for different competitions including the CONMEBOL ‘s qualifying matches for the 2022 Qatar World Cup and its recently acquired rights to stream Series A and Coppa Italia matches in Canada.

Additionally, through its subsidiary Fubo Gaming, the company has signed multiple market access deals that will allow it to offer a sports betting service to customers from different corners of the United States.

Finally, Fubo has been increasing its advertising revenues progressively to further diversify its revenue mix.

All in all, this company has demonstrated its ability to reach important milestones and has delivered the kind of results that make it stand out as a top growth pick in what is already a hot industry. With the cord-cutting trend accelerating beyond pre-pandemic levels, FuboTV may stand to become a major player in the sports streaming industry in the future and this is the reason why I have picked it for this list of best stocks to buy in Q3 2021.

67% of all retail investor accounts lose money when trading CFDs with this provider.

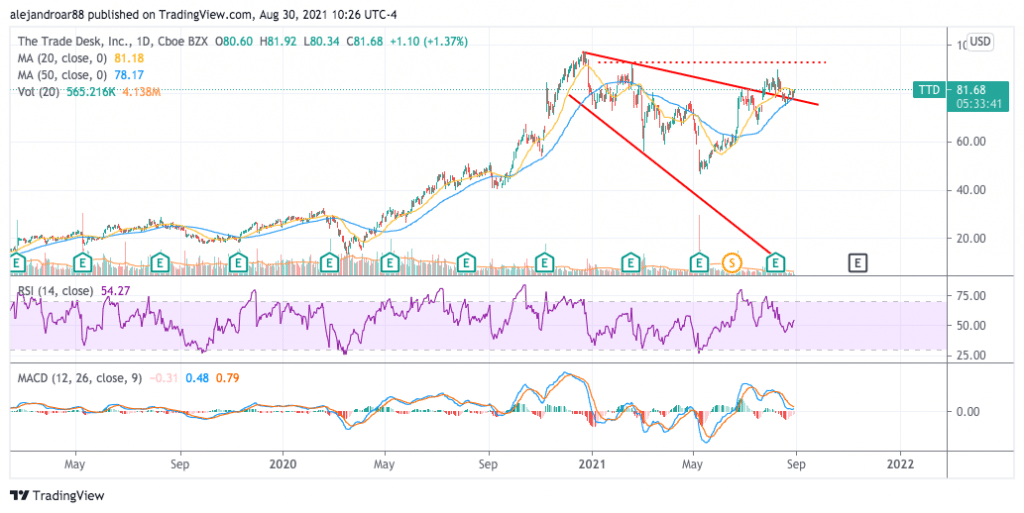

#5 – The Trade Desk (TTD)

In an increasingly digital world, online advertising has become the leading form of marketing for corporations, small-to-mid-sized businesses, and professionals around the world. In this particular context, the services provided by The Trade Desk platform will likely see their demand accelerate as more and more businesses may progressively turn to the internet to ramp up their top-line results.

Sales of TTD have quadrupled from 2016 to 2020 moving from $202.9 million to $836 million while the company has delivered profits every single of those years. During that same period, bottom-line profit margins have improved dramatically moving from around 10% in 2016 to nearly 29% last year while its return on equity (ROE) has progressively climbed above the 20% threshold during that period as well.

Meanwhile, GAAP diluted earnings per share have been advancing at a positive pace after the company swung to positive EPS in 2017 at $0.12. Last year, TTD reported $0.50 resulting in a 60.9% 3-year CAGR.

Even though analysts are expecting a slowdown in its growth rates moving forward, as the demand for digital advertising continues to grow, a business such as The Trade Desk will likely be benefitted from an accelerated digital adoption.

Therefore, these forecasted EPS may not fully reflect the business’s future prospects and might be undervaluing its upside potential.

At the moment, TTD stock is trading at 118 times its forecasted earnings per share for the next twelve months. Considering the rate at which the firm has been growing its bottom-line results, this multiple doesn’t seem as stretched as it looks at first glance. Moreover, TTD has nearly no debt.

So far this year, the stock has gone up less than 2% after a solid 208.3% gain it delivered last year. Moving forward, investors may either wait for a temporary pullback to enter a position at more reasonable multiples or may progressively purchase the stock through dollar-cost averaging (DCA) to smooth the short-term fluctuations that TTD stock could experience over the coming months.

Even though the current valuation seems relatively fair considering the firm’s past performance and future prospects, a lower entry price may increase the odds of generating gains in a shorter period.

67% of all retail investor accounts lose money when trading CFDs with this provider.