Forex Volatility Levels Have Crept Higher

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

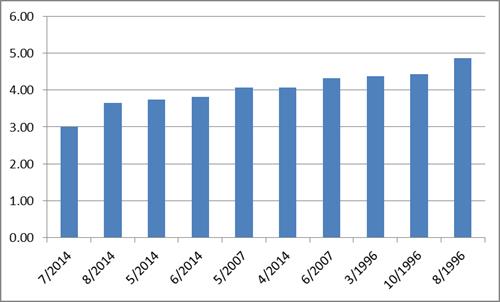

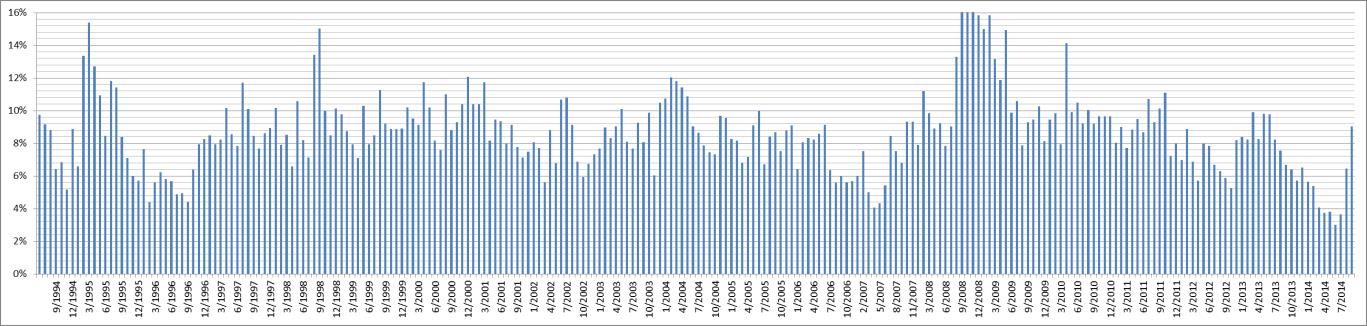

In March of this year, forex volatility was about as lifeless across GBP, DXY, EUR and JPY as it had been for the past five years: pretty much matching a low in October 2012. In April, volatility across those currencies was as low as it had been since before the 2008 crash, matching the record set in May 2007. July, August, May and June of this year were the four least volatile months for forex since 1994 (see chart, all data from IG’s forex pages). Before this summer, average volatility across those four currencies had only dropped below 4% once in 20 years.

In March of this year, forex volatility was about as lifeless across GBP, DXY, EUR and JPY as it had been for the past five years: pretty much matching a low in October 2012. In April, volatility across those currencies was as low as it had been since before the 2008 crash, matching the record set in May 2007. July, August, May and June of this year were the four least volatile months for forex since 1994 (see chart, all data from IG’s forex pages). Before this summer, average volatility across those four currencies had only dropped below 4% once in 20 years. Over the summer, it remained there for four consecutive months.

The true effects of such a sustained drought in forex will probably not be fully known for some time yet. For now, though, it appears that the rains have come: September saw volatility creep back up above 6%, and October 9%.

EUR/GBP/DXY/JPY average volatility over 20 years.

But it may be premature to declare that life on the markets has fully returned to normal: after all, there was an abnormal amount of activity across indices and equities in October, and forex hit a thoroughly average figure.

The record-low interest rates and policy of quantitative easing employed by major economies (specifically those of the four currencies examined above, though many others have followed suit) has often been blamed for the lack of currency movements. The logic behind such a claim is clear: the low return on cash makes trading forex less enticing to investors. Thus, removing liquidity takes away forex’s single biggest incentive.

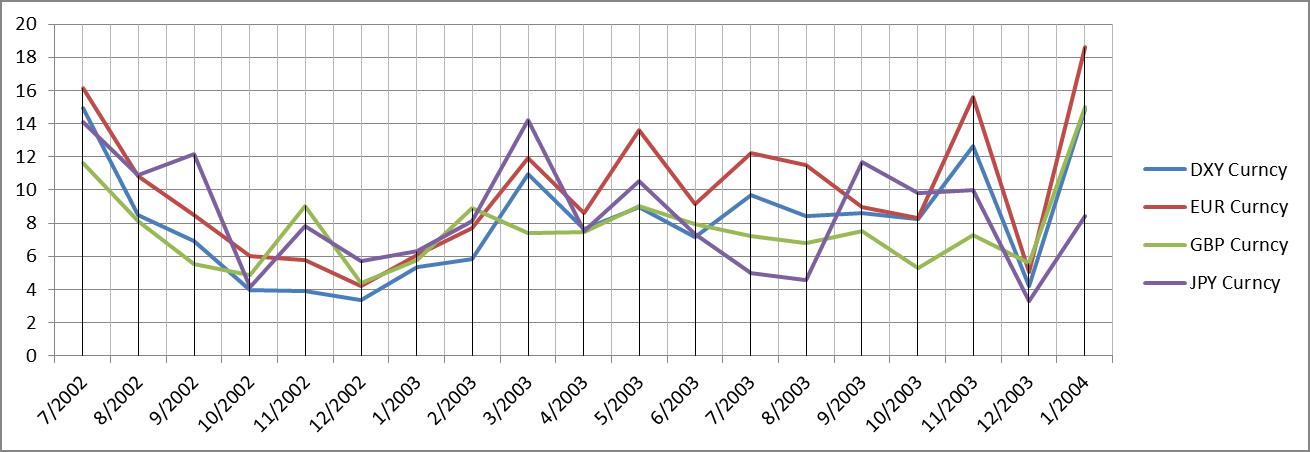

No interest rate rise has come about in the past two months, however, and forex movement has returned. This has also been true for previous periods when interest rates have been suppressed – by the Bank of Japan and Bank of England for several years after the millennium – which, while generally acting as a dampener on forex volatility, were also home to some notable peaks.

Of course, it is impossible to know whether those peaks would have been accentuated if the UK and Japan had higher interest rates; it does appear, though, that other currencies saw greater movement over the same period.

DXY, EUR, GBP & JPY volatility July 2002 – January 2004. UK currency movement suppressed by low interest rates, but occasionally very liquid.

The returning forex volatility in September and October may not have been caused by an anticipated rate rise, but it could have been caused by the final realisation on the markets that a rate rise was not in fact imminent.

October’s most volatile days were those that came immediately after the International Monetary Fund released a decidedly pessimistic view of global growth, and low inflation made it clear that no central bank would be going near rate rises for some time yet. The long running status quo, where America’s place at the forefront of the race to a rate rise ensured that investors stayed away from other currencies, was broken.

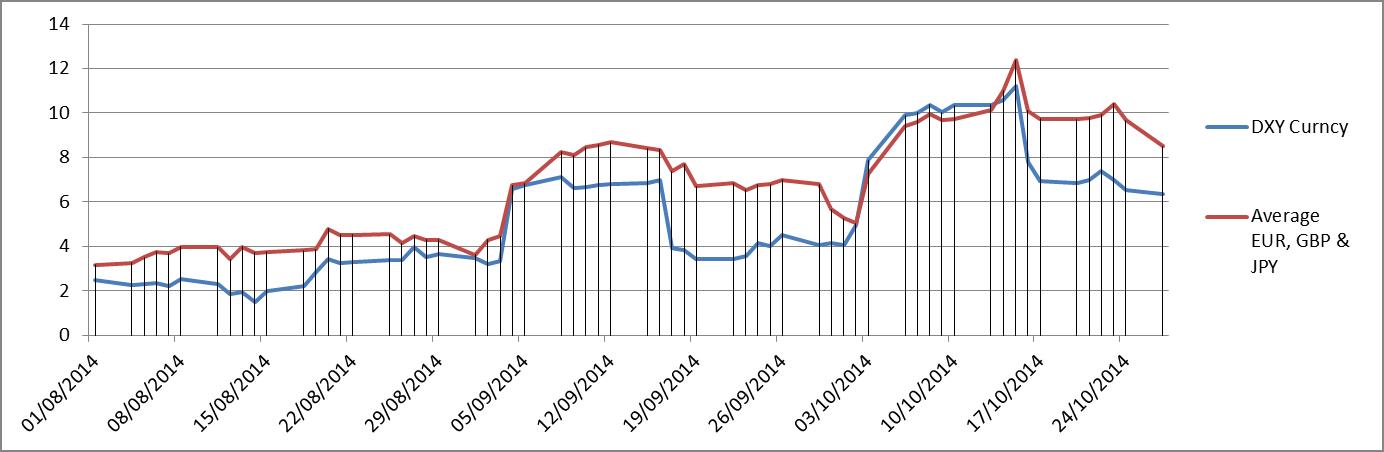

US vs EUR/GBP/JPY currency volatility Aug-Oct 2014. USD liquidity briefly catches up as fears of US strength take hold.

The playing field was abruptly levelled during the week of October 8 and beyond, as the dollar’s stability was eroded and it challenged the average volatility of EUR, GBP and JPY. Since then though, several releases have – once again – changed the game somewhat.

Stress tests across Europe have sent banks back into the doldrums once more. US QE is about to end. If more hawkish sentiment from the Federal Reserve arrives, combined with good non-farm payrolls and GDP data, a confident US bull market may once again take hold.

Two possible scenarios have become apparent, then. In one, forex volatility is back, part of the re-emergence of risk trading that will come to define this financial year. In the other, a wobble on the long road to recovery changed the picture briefly, and we will soon see currencies settle once again. In part, the choice of which one takes hold is in the hands of traders, central banks and businesses. Either way, more unpredictability is surely on the way in the next few months.

Forex volatility has come back, but for how long? is republished with permission from IG.com