Affirm Stock Sinks After Fiscal Q2 Earnings: Key Takeaways

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Affirm stock (NYSE: AFRM) plunged over 10% on Friday despite the company posting better-than-expected revenues. Here are the key takeaways from the buy-now-pay-later (BNPL) company’s fiscal second quarter 2024 earnings.

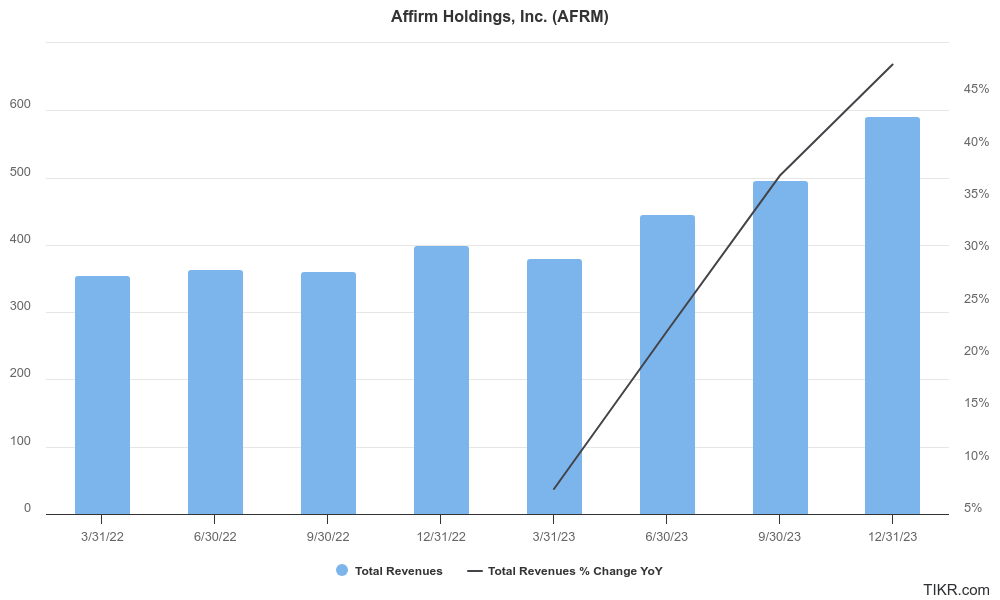

Affirm reported revenues of $591 million in the quarter which was up 48% YoY and $70 million higher than the corresponding quarter last year. The company’s GMV (gross merchandise value) rose 32% YoY to $7.5 billion while RLTC (revenue less transaction costs) surged 68% YoY to $242 million.

Table of Contents

Affirm posted better-than-expected earnings

The impressive rise in RLTC helped Affirm more than halve its operating losses to $172 million in the quarter while its adjusted operating income also rose to $93 million as compared to an adjusted operating loss of $62 million in the corresponding quarter last year.

In the shareholder letter, Affirm said, “RLTC as a percentage of GMV also increased by 70 basis points year over year and returned to our 3 to 4% long-term target range. This robust performance was driven by strong revenue growth with total revenue increasing $192 million year over year.”

It added, “In absolute terms, approximately two thirds of the revenue growth came from higher interest income, with the remainder coming from network revenue.”

Notably, despite the rise in GMV, Affirm’s credit quality was stable in the quarter and its shareholder letter, it said, “We believe credit performance has largely returned to pre-pandemic trends.”

It added, “This includes normal seasonality, which has historically led to seasonally lower delinquency rates during the second and third fiscal quarters and seasonally elevated delinquency rates in the first and fourth fiscal quarters.”

AFRM raised its guidance

After the stellar fiscal Q2 earnings, Affirm also raised its full-year guidance and now expects the GMV to be over $25.25 billion which is $1 billion higher than the previous guidance. Meanwhile, a section of the market believes that the guidance is quite conservative as the company beat GMV by $700 million in Q2 only.

Affirm’s CFO Michael Linford said during the earnings call, “we’re only providing a floor or our full year guide. And so, we did take our floor up by $1 billion, which we think is a pretty big step-up in what we would expect for the year.”

Jefferies analyst John Hecht said after the report that “expectations were high going into this print, but the strong beat and momentum lead us to believe the new guidance is also conservative, even when considering the increase in the outlook.”

For the fiscal Q3, Affirm forecast GMV between $5.8 billion to $6 billion which was higher than what markets expected at the midpoint. The company expects revenues between $530 million to $550 million in the quarter and RLTC to be between $205 million to $215 million.

Max Levchin on AFRM’s earnings

Affirm CEO Max Levchin was quite upbeat on the company’s performance in the quarter and started the shareholder letter by saying, “This time last year, we reiterated our commitment to building operating leverage without sacrificing credit performance, volume growth, or innovation. The market wasn’t exactly convinced then, but 12 months later, we have done exactly what we said we would.”

Affirm said the Shopify partnership helped support its growth

The company emphasized its partnership with Shopify and said that it was the key driver of GMV growth. Levchin said, “program at Shopify grew twice the speed of the overall Affirm growth on the GMV side of things. They have aspirations offline that they’re going after quite strongly, and there’s still a lot of synergies. And what we’re doing now there, we have a whole host of programs we’re contemplating going forward.”

Markets were bearish in AFRM stock in early 2023

Markets were quite bearish in Affirm and Trent Masters, fund manager at Alphinity Investment Management predicted that Affirm would not survive 2023. He said, “When it comes to BNPL, it really is that tip of the spear where [their customers] were getting filled with fairly free capital through all the stimulus programs.”

He added, “That was the kind of the business models that I’m talking about where the free and infinite capital not just underpinned the value and the growth, but it’s actually really essential to potentially the survival of those businesses.”

From Apple’s entry into the buy-now-pay-later space, regulatory uncertainty over the industry, multi-year high interest rates, and recession fears, Affirm faced several challenges at the beginning of 2023.

The company’s perennial losses were not helping matters either and it even shut down its crypto business to reduce its cost base.

At the beginning of 2023, analysts were quite apprehensive about Affirm stock but the company proved naysayers wrong and rose over 400% last year making it the best-performing stock among the companies with a market cap of $5 billion or higher.

Analysts on AFRM’s earnings

Despite strong earnings and guidance raise, Affirm shares closed lower on Friday. Wells Fargo analyst Andrew Bauch said in a client note that AFRM’s earnings had something for both bulls and bears and said, “We suspect bullish investors remain emboldened by [Affirm’s] stellar execution in recent prints.” He however added, “That said, while we believe bears may likely concede on that front, they may point to elevated valuation levels proving too difficult to own shares.”

Buch said that since AFRM does not have a listed peer, it’s “fruitless” to have discussions on the company’s valuation. He maintained his equal weight rating and $40 target price on the stock and said, “While unsatisfying, shares are subject to market momentum.”

However, Morgan Stanley continues to remain bearish in the stock and has a $20 target price and underweight rating on Affirm. In a client note, analyst James Faucette said, “We continue to believe that valuation is stretched and remain focused on [Affirm’s] ability to close the monetization gap with [Capital One] while accelerating margin expansion and maintaining revenue growth, a combination which may prove challenging.”

Meanwhile, Mizuho analyst Dan Dolev who is bullish on AFRM stock maintained his $65 target price on the shares and said, “We continue to believe that [Affirm] is one of the most innovative names in our coverage universe and therefore the ~2-turn premium is deemed appropriate.”