A Preview of What May Come in 2015

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

2015 might be a very important year for many economies across the globe. Last quarter of 2014, saw many fluctuations in the economic indicators of different countries. While US ended 2014 with a good performance, Russia faced double trouble with falling currency and oil prices. Satyajit Das, a former banker and author, in his article ‘How easy money has cracked the global economy’, writes that global financial markets face serious economic and non-economic risks in 2015 that are above and beyond the challenges seen in 2008.

2015 might be a very important year for many economies across the globe. Last quarter of 2014, saw many fluctuations in the economic indicators of different countries. While US ended 2014 with a good performance, Russia faced double trouble with falling currency and oil prices. Satyajit Das, a former banker and author, in his article ‘How easy money has cracked the global economy’, writes that global financial markets face serious economic and non-economic risks in 2015 that are above and beyond the challenges seen in 2008. This seems true when we look at the larger picture (beyond what we’ve already seen in 2014). In this article, we focus on a few countries that could trigger or see some big changes in 2015.

Table of Contents

Japan

After suffering from negative growth for two consecutive quarters, the Japanese economy fell into a technical recession, which raised doubts on the effectiveness of Abenomics. In 2015, Japan will struggle to keep up with its falling economy. Many new policies under Prime Minister Shinzo Abe may give hope to its economy. Prime Minister Shinzo Abe’s resounding victory in Japan’s snap election could give him the political capital to make tough concessions in areas such as agriculture and automotive. The Central bank of Japan (BoJ) has announced huge asset purchase programs (Quantitative Easing). Mr. Shinzo Abe is pushing towards changing the societal and corporate norms by promoting ‘Womenomics’. Even though the share of working women in Japan is more than that in the US, they still earn significantly less than the men. But there have been many criticisms regarding ‘Womenomics’ especially after Prime Minister Abe, himself appointed a record-tying five female ministers to his Cabinet, two of who resigned after scandals. In September 2014, the head of the International Monetary Fund, Christine Lagarde, said significant steps to close the gender gap could increase Japanese economic growth by a quarter of a percentage point. That is not small in a country that has averaged less than 1 percent growth for the last two decades.

United States

The United States will be on its path of revival since it has shown improvement in 2014 and will again prove to be the global engine. 2015 has brought good news for US. But the question remains whether the economy will perform better or will show a gradual slowdown after a couple of months. Many economists argue that reasons that could slow the U.S. economy is the geopolitical risk building up from countries like China, Russia and the rising dollar that could potentially damage the exports. But U.S. seems more insulated from the rest of the world’s ups and downs than other major economies are. Exports account for just 14 percent of U.S. output, the smallest share among the 34 mostly rich members of the Organization for Economic Cooperation and Development (OECD).

Eurozone

Eurozone crisis will continue from where it left off, only this time it maybe larger and more politically driven than before. 2015 will not be a year of improvement for the Eurozone since it struggles with high unemployment, little growth and low investment. Even though, Germany (relatively a stronger economy in the zone) has a low unemployment rate, inflation remains well below the European Central Bank’s 2% target. With large debts and situations worsening in Greece, it might not be a big surprise if Greece is shown the exit door (also known as ‘Grexit’) from Eurozone. On the other hand, upcoming elections in Greece may bring in a government (Left-wing party called Syriza) that does not want to leave the Eurozone but wants to end the German-led austerity. This means that the entire arrangement (renegotiating terms of bailout) made prior to the election would be put to question. In 2015, the flawed structural design of Eurozone will become more evident as the crisis deepens in some countries in the Eurozone. According to Paul Krugman, ‘Europe is at a dead end; if anything, Greece is doing the rest of Europe a favor by sounding a wake-up call’.

.png)

SOURCE: WORLD ECONOMIC OUTLOOK, OCTOBER 2014

China

As for emerging economies, China will see a fall in its growth and even if it manages to pick up, it will remain a slow recovery. The country has seen a decade of growth of 10% to 12% and now it’s going to have to adjust to 6.5% to 7% in the future. China has yet to absorb the production capacity created by large-scale investment in 2010-2011. A property slump could well be expected in 2015. China started on a weak note and situation can get worsened as companies may struggle to pay off their debts. Services sector will remain the one and only bright spot in China’s economy. In November 2014, China had cut its interest rates (first in 2 years), injected more capital in the banking system and relaxed restrictions to promote lending though risk-averse banks. Even though the economic planning agency is approving more infrastructure projects and central bank is trying to maintain its economic growth, 2015 will probably be a slow year for China.

Russia

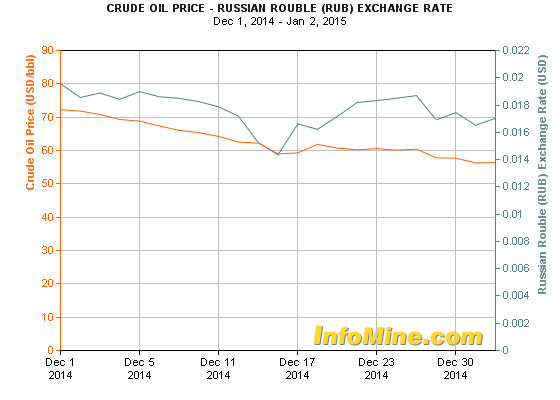

Out of the emerging markets, 2015 will prove very vital for Russia. Russia faces geopolitical risks, falling oil prices and loss of value of the ruble. After heavy sanctions, Russia cut off trade ties with the Eurozone. This could destabilize the markets since Russia was the second largest trade partner of Eurozone. This year will be testing times for both Russia and Eurozone. Oil and gas revenues bring about 60 percent of Russia’s export revenues. Oil prices have fallen by over 50% since June to below $50 a barrel, under the impact of growing supply due to US fracking and declining demand from a slowdown in China and recession in Europe. Western sanctions have intensified the impact. This year Russia will look at various options depending on how the prices of oil behave. Government estimates claim that food prices might increase by 12% and overall inflation rate will rise up by 10% towards the start of 2015.

2015 will be a year that will test many emerging economies like Brazil, Russia and China. Advanced countries will take measures to revive past growths and try to remain in the race. Low oil prices will lower inflation in many economies, while China’s ongoing economic slowdown will keep downward pressure on other commodity prices. While lower inflation levels will be a welcome development for high-inflation countries such as India, cheap oil will hurt producers such as Malaysia and Russia. Meanwhile, sluggish growth in Europe and Japan should weigh on Asian exporters.

The World This Year 2015 is republished with permission from The Financial Keyhole