Apple Stock Rallies After Q2 Earnings and Analysts See More Gains Ahead

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Apple stock (NYSE: AAPL) rallied almost 6% yesterday and had its best day since November 2022 after the iPhone maker’s fiscal Q2 2024 earnings were better than feared. Here are the key takeaways from the report and how analysts reacted to the earnings.

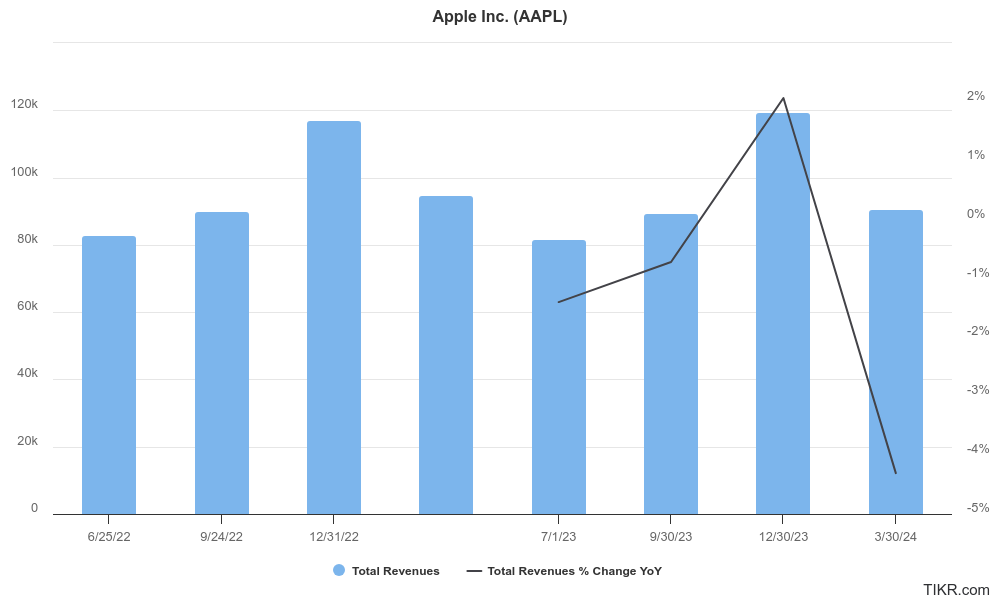

Apple reported revenues of $90.75 billion in the fiscal Q2 as compared to $94.83 billion in the corresponding quarter last year. During their previous earnings call, the company said that after adjusting for $5 billion in pent-up sales in fiscal Q2 2023, its revenues in the quarter would be “similar.”

Eventually, its topline performance turned out to be slightly better than its guidance and was also north of the $90.01 billion that analysts were expecting.

Apple Reported Better Than Expected Earnings

Diving deep into the earnings, Apple reported iPhone revenues of $45.96 billion which trailed analysts’ estimate of $46 billion. iPad revenues came in at $5.6 billion which too fell short of the $5.91 billion that analysts were expecting. Other Product revenues of $7.9 billion were also lower than the consensus estimate of $8.08 billion.

However, Services was a bright spot and revenues rose 14.1% YoY to $23.86 billion. The metric easily surpassed analysts’ estimate of $23.27 billion and was a new quarterly record. Mac revenues were also much better than expected at $7.5 billion which was over $600 million higher than consensus estimates.

While Apple’s gross margin of 46.6% was in line with estimates, its EPS of $1.53 was slightly ahead of the $1.50 that analysts were expecting.

China Sales Were Better Than Feared

During the earnings call, Apple said that it set revenue records in more than a dozen countries and regions, including Canada, India, Spain, and Turkey. While there are concerns over iPhone sales in China, Apple CEO Tim Cook was quite upbeat and said sales grew in Mainland China during the quarter. Citing data from Kantar he said iPhone 15 and iPhone 15 Pro Max were the top two selling smartphones in the country during the quarter.

Commenting on the outlook for China business, Cook said, “I maintain a great view of China in the long-term. I don’t know how each and every quarter goes and each and every week. But over the long haul, I have a very positive viewpoint.”

Apple expects revenues in the current quarter to rise in the low single digits from the corresponding quarter last year despite a 2.5 percentage point headwind from adverse currency movements. It expects Services revenues to grow in double digits – in line with the fiscal second quarter.

Apple on the Generative AI Opportunity

Cook said that the company was very bullish on the opportunity in generative AI and added, “we’re getting ready for an exciting product announcement next week that we think our customers will love. And next month, we have our Worldwide Developers Conference, which has generated enormous enthusiasm from our developers. We can’t wait to reveal what we have in-store.”

Apple also announced a record share buyback of $110 billion. The company had net cash of $58 billion at the end of the quarter and continues to generate billions of dollars of cash every year.

Analysts See More Upside in AAPL Stock

Analysts were impressed with Apple’s earnings and are now awaiting more AI-related announcements. Citi added a positive catalyst watch on the stock and said, “We are opening a positive catalyst watch into Apple WWDC24′ developer conference on June 10th as Apple CEO Tim Cook sounded bullish on AI on earnings call and expect Apple to unveil multiple AI developer tools to enhance interactivity.”

Bank of America reiterated Apple as a top pick and raised its target price by $5 to $230 and said, “The thesis for our upgrade to Buy earlier this year is playing out with: (1) strong multi-year iPhone upgrade cycle coming driven by GenAI (mgmt. commentary on earnings call very bullish), (2) Services growth reaccelerating.”

JPMorgan analyst Samik Chatterjee maintained his overweight rating and raised Apple’s target price from $210 to $225. In his client note, Chatterjee wrote, “The confluence of better-than-feared results in relation to F2Q (March-end) revenue and guidance for stronger than expected revenue growth in F3Q (June-end) are setting up a strong launch pad for the company in relation to results in FY24 as focus turns to the impending AI smartphone upgrade cycle in the coming years.”

Apple’s Installed Base Is Rising

Apple’s installed base of active devices reached an all-time high during the quarter. The steadily growing base represents a cross-sell opportunity and also bodes well for Apple’s Services business.

Goldman Sachs analyst Michael NG is particularly bullish on the rising installed base. In his client note, he said, “We believe that the durability of AAPL’s installed base is underappreciated, and AAPL should improve revenue per user by increasing hardware units per iPhone user, Product price/mix, and Services attach & monetization as AAPL invests in its ecosystem.”

Meanwhile, despite the sharp rise on Friday, Apple shares are slightly in the red for this year. Also, the company is yet to reclaim its title as the world’s largest company as well as the $3 trillion market cap.