Apple Reported Mixed Q4 Earnings: Here’s How Wall Street Reacted

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Apple (NYSE: AAPL) reported its fiscal Q4 2023 earnings last week and the stock closed marginally lower after the Cupertino-based company reported mixed earnings in the quarter. Here are the key takeaways from the report and how Wall Street reacted to the company’s earnings report.

Apple reported revenues of $89.5 billion in the fiscal fourth quarter which was 1% lower YoY but slightly ahead of $89.28 billion that analysts expected. Nonetheless, it was the fourth consecutive quarter when the iPhone maker reported a YoY fall in sales – a rarity for the company.

iPhone sales were in line with analysts’ estimate

Looking at the different business segments, iPhone sales came in at $43.81 billion which was in line with what the markets expected. Notably, in the previous quarter, iPhone sales trailed analysts’ estimates and Apple shares fell despite better-than-expected earnings. In fiscal Q4, markets were anyways circumspect about iPhone sales and had tepid expectations.

However, it was a September quarter record for iPhone sales and came amid tough macro conditions. In his prepared remarks, Apple’s CEO Tim Cook said, “We now have our strongest lineup of products ever heading into the holiday season, including the iPhone 15 lineup and our first carbon neutral Apple Watch models.”

iPhone sales in China were $15.1 billion which was 2.5% lower than the corresponding quarter last year and below street estimates. The company is facing intense competition in China from domestic smartphone companies, especially Huawei. Notably, China has also put restrictions on central government employees from using foreign smartphones – including Apple iPhones. According to CFO Luca Maestri, “China has always been the most competitive market in the world and we think it will continue to be like that.”

Apple Services hit record revenues

Apple’s Services business also hit an all-time high and posted revenues of $22.31 billion which were up 6.3% YoY and well ahead of the $21.35 billion that analysts expected. While the Services business faces several headwinds, it performed quite well in the fiscal fourth quarter.

The company’s installed base and active subscription on the platform have been rising steadily which has helped the Services segment. In his prepared remarks, Maestri said, “Our active installed base of devices has again reached a new all-time high across all products and all geographic segments, thanks to the strength of our ecosystem and unparalleled customer loyalty.”

Other product sales sag

Meanwhile, sales of other Apple products sagged and Mac revenues were $7.61 billion in the quarter – way below the $8.63 billion that analysts expected. iPad revenues however came in at $6.44 billion which was ahead of the $6.07 billion that analysts expected. Wearable revenues of $9.32 billion meanwhile slightly trailed analysts’ estimates.

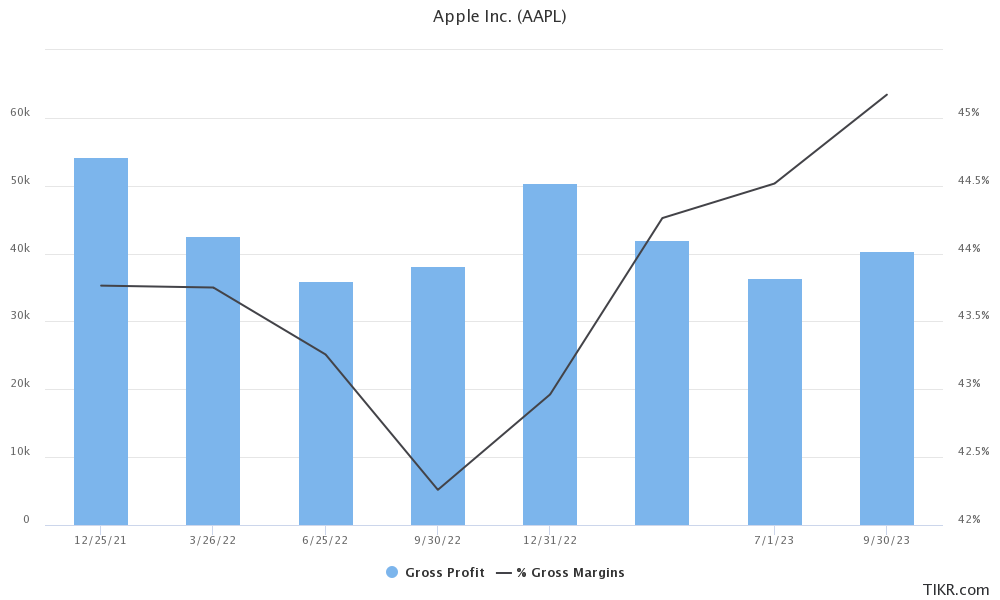

However, Apple’s gross margins hit a record 45.2% in the quarter which was higher than the 44.5% that analysts expected which helped the world’s largest company post an adjusted EPS of $1.46 – ahead of the $1.39 that analysts expected.

Apple gave tepid guidance

The biggest dampener in Apple’s earnings call was the commentary on December quarter sales and expects them to be “similar” to the corresponding quarter last year. Maestri however stressed that “the December quarter this year will last the usual 13 weeks, whereas the December quarter a year ago spanned 14 weeks. For clarity, revenue from the extra week last year added approximately 7 percentage points to the quarter’s total revenue.”

He added, “We expect iPhone revenue to grow year-over-year on an absolute basis. We also expect to grow after normalizing for both last year’s supply disruptions and the 1 extra week.”

While he said that the company expects Mac’s YoY performance to improve significantly as compared to the September quarter, he warned, “We expect the year-over-year revenue performance for both iPad and Wearables, Home and Accessories to decelerate significantly from the September quarter due to a different timing of product launches.”

Tim Cook on India

India has been a focus market for Apple and the company opened its first two retail stores there this year. Responding to an analyst question during the earnings call, Cook said, “We had an all-time revenue record in India. We grew very strong double digits. It’s an incredibly exciting market for us and a major focus of ours. We have low share in a large market. And so it would seem that there’s a lot of headroom there.”

While he admitted that the average selling prices in India are lower than the company’s worldwide average and did not draw himself into comparing the market with India he stressed: “we see an extraordinary market (in India), a lot of people moving into the middle class, distribution is getting better, lots of positives.”

How analysts reacted to Apple earnings

Morgan Stanley reiterated Apple as overweight and said, “Dec Q EPS are largely unchanged as record margins offset rev miss. Remain guarded NT until we get greater clarity on iPhone demand and the DOJ vs. GOOGL case. But last night’s results also strengthen the LT bull case, and we expect ARPU to inflect higher once the macro storm passes.”

Morgan Stanley analyst Eric Woodring said, “Near term, our focus is on iPhone sell-through, while longer term we believe last night’s results strengthen the bull case.”

Barclays analyst Tim Long meanwhile lowered Apple’s target price by $5 to $161. In his client note, Long said, “We are fine-tuning our revenue estimate for Dec-Q and now model flat revenue Y/Y, with demand continuing to weaken.”

Long added that Barclays’ rating is driven by “headwinds sustaining current demand levels as high-end consumers potentially weaken further, tougher comps on Macs/ iPads, regulatory overhang (App Store, Google TAC), lack of differentiation on designs and specs for the current iPhone 15 as well as a rich valuation vs. SPX.”

Gene Munster on Apple

Meanwhile, even as some analysts are concerned about Apple’s valuation, especially in light of the growth slowdown, Gene Munster, managing partner at Deepwater Management believes that Apple is now becoming like a consumer staples company and can command higher valuations. He also talked about the record base of installed devices and record gross margins to corroborate his views that Apple can continue to trade at higher multiples.