Analysts Get Jittery About Tesla amid Expected Margin Erosion

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Some Wall Street analysts are getting jittery about Tesla ahead of the company’s Q3 earnings on fears that the price cuts would lead to a margin erosion for the electric vehicle (EV) giant.

After the most recent round of price cuts, Tesla’s website lists the starting price for the Model 3 at $38,990 while the Model Y at $45,990. After these price cuts, Tesla has lowered the prices of the Model 3 standard version by almost 17% in the US since the beginning of the year.

The Elon Musk-run company’s operating margins fell to 9.6% in Q2 2023 as compared to 14.8% in the corresponding quarter last year. The margins are now less than half of what they were at their peak.

TSLA’s margins fall amid price cuts

To be sure, Tesla has made a conscious decision to prioritize the growth in deliveries over profit margins and during the Q1 2023 earnings call Musk said, “We’ve taken a view that pushing for higher volumes and a larger fleet is the right choice here versus a lower volume and higher margin.”

Musk believes that Tesla can make up for lower margins through sales of autonomous technology and said, “We’re the only ones making cars that, technically, we could sell for 0 profit for now and then yield actually tremendous economics in the future through autonomy. No one else can do that. I’m not sure how many people will appreciate the profundity of what I’ve just said, but it is extremely significant.”

Analysts on Tesla stock

Meanwhile, the frequent price cuts and their impact on Tesla’s margins are making analysts apprehensive. Even Morgan Stanley analyst Adam Jonas – who’s among the biggest Tesla bulls and last month said in a note that the company’s Dojo compute can add $600 billion to its market cap – believes that concerns over near-term erosion in Tesla’s margins are not unfounded.

Yesterday, Jefferies analyst Philippe Houchois also lowered Tesla’s target price and said in his note “In the last few months, tracking Tesla fundamentals has felt a bit like watching paint dry.”

He added, “More margin erosion in Q3 and uncertain growth in 2024 still raise questions whether Tesla’s earlier profit edge was structural or a timing difference.”

Houchois raised some serious questions about Tesla’s lead in the EV market and said “We continue to think that everything Tesla does differently from the rest of the industry can also be done by others if given time, making speed essential to maintain an edge.”

Wells Fargo is also cautious ahead of Tesla’s upcoming earnings release amid concerns over margin erosion.

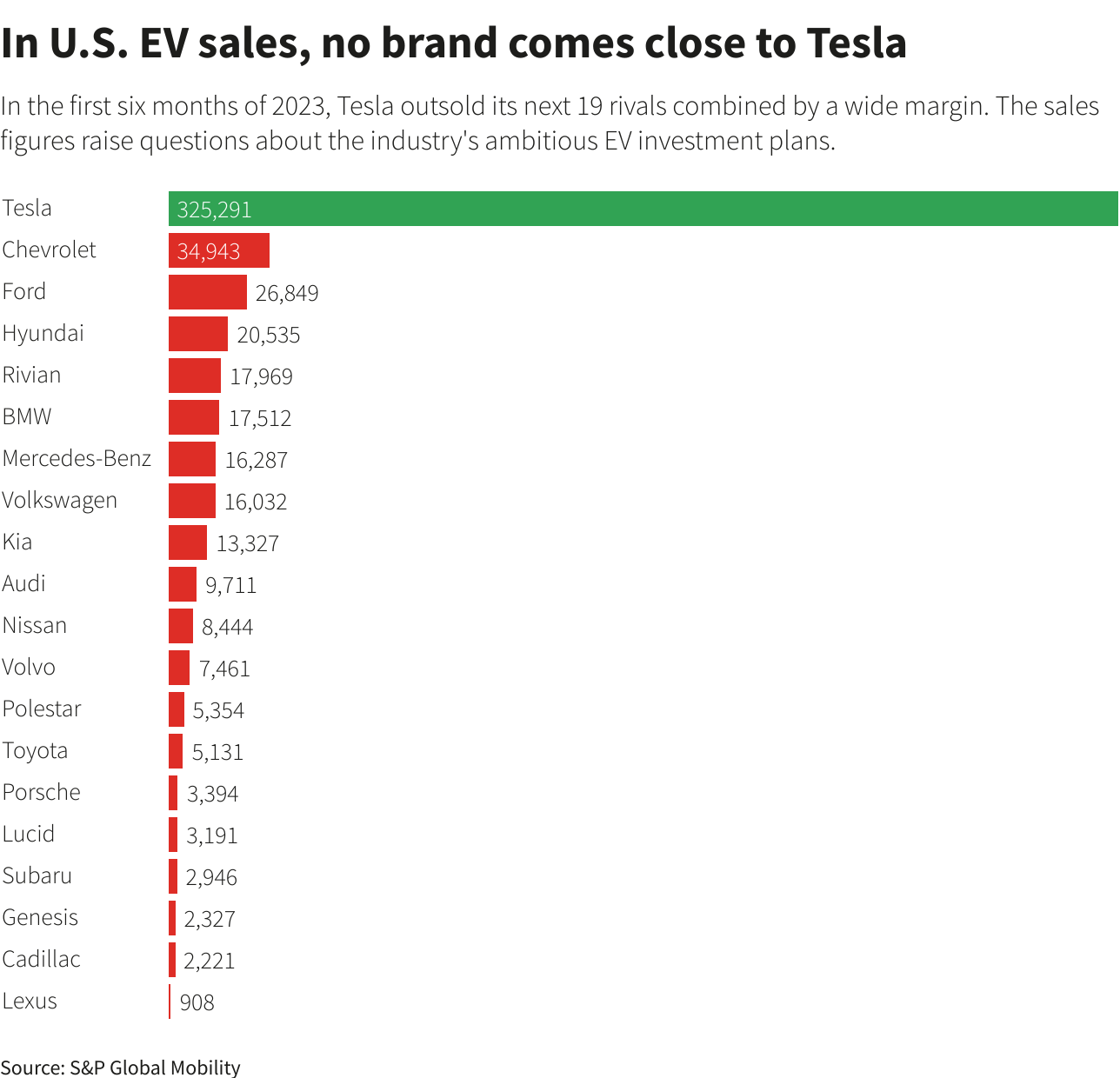

TSLA is the market leader in the US EV market

Meanwhile, even as Tesla’s market share in the US EV market has come down, it still leads the market by a wide margin. In the first half of 2023, Tesla sold over 325,000 vehicles in the US which is more than the next 19 rivals and almost 10x of what the runner-up General Motors sold during the period.

In terms of models, Tesla Model Y is the best-selling EV model followed by Tesla Model 3. Despite their percentage share in Tesla’s overall deliveries falling, the Model X and Model Y are also among the top 12 EV models in the US.

However, when it comes to the global markets, Tesla has lost the crown of the biggest seller of new energy vehicles, and looking at the rising sales of BYD it looks to dislodge Tesla as the largest EV seller as well.

Bank of America expects Tesla’s US EV market share to drop to 18% by 2026. That said, it does not mean that Tesla’s absolute deliveries are expected to fall as the US EV market share is expected to rise significantly over the next few years.

Tesla expects its deliveries to rise steeply

Tesla has set itself a target of producing 20 million cars annually by 2030. To put that in perspective, Toyota, the world’s largest automaker, sold just over 10 million cars in 2022.

To achieve the goal of 20 million deliveries, which amounts to a CAGR of over 41% between 2023 and 2030, Tesla might need to build many more Gigafactories. In the past, Musk said that the company would need over a dozen Gigafactories to reach that goal.

At the annual day, Musk said that the company can sell 5 million units of the two new models. Additionally, he said that it can deliver upto half a million Cybertrucks.

Tesla might need more models to spur sales and Houchois said, “Hyperscaling through model concentration remains a unique feature of Tesla’s auto business model but reaches its limits without the launch of more volume models.”

TSLA stock has more than doubled in 2023

Meanwhile, despite multiple price cuts, Tesla stock has more than doubled in 2023 and is outperforming EV peers. Musk incidentally believes that Tesla’s valuation is tied to its autonomous driving business – a view echoed by most Tesla bulls especially ARK Invest’s Cathie Wood who expects the stock to rise to $2,000 by 2027 under her base care.

Speaking at the Paris VivaTech innovation conference in June, Musk emphasized that Tesla’s valuation is linked to its autonomous driving business and said, “The potential for autonomy is that the value of autonomy is so high, that even if you have a discount, a percentage probability of autonomy happening, that is so incredibly valuable.”

He pointed to Tesla’s low share of the global auto market and said, “If you look at our total vehicle output, it’s almost 2 million vehicles this year or something like that. But that’s still only 2% of total vehicle production.”

Notably, despite selling far fewer cars than legacy automakers, Tesla is the most valued automaker and its market cap is more than the combined market caps of all leading automakers. While legacy automakers tend to trade at single-digit PE multiples – Tesla commands much higher multiples amid its perception as a tech company and not merely an automaker.