Meta Platforms Stock Price Forecast April 2022 – Time to Buy FB Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

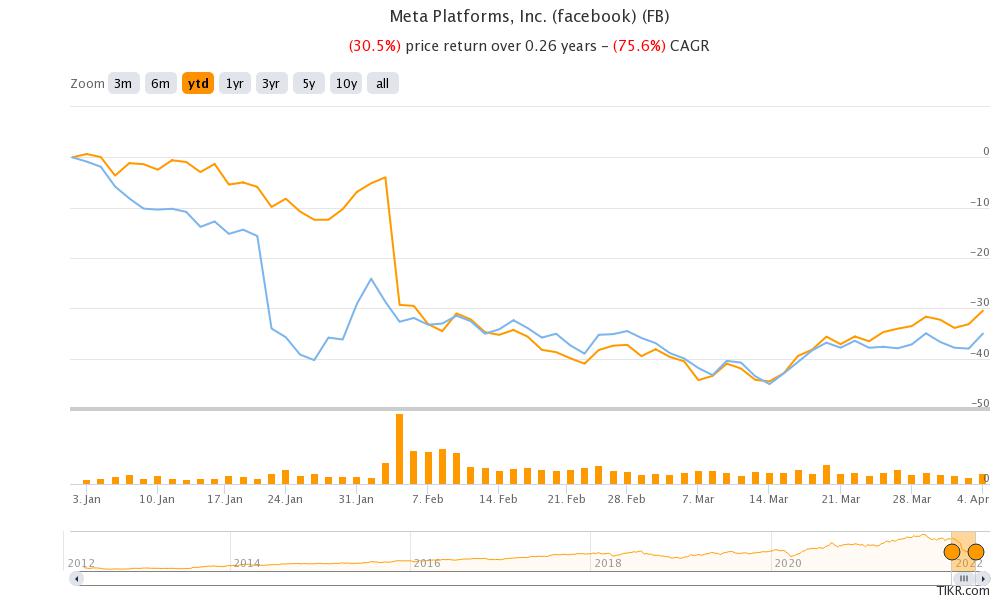

With a YTD loss of around 30%, Facebook parent Meta Platforms (FB) is the second-worst performing FAANG stock of 2022. Only Netflix has fared poorly this year and both these companies are underperforming not only fellow FAANG stocks but also the S&P 500 this year.

Despite having rebounded almost 25% from its lows, FB stock is still down almost 40% from its 52-week highs. What’s the forecast for the stock and is it a good buy in April 2022?

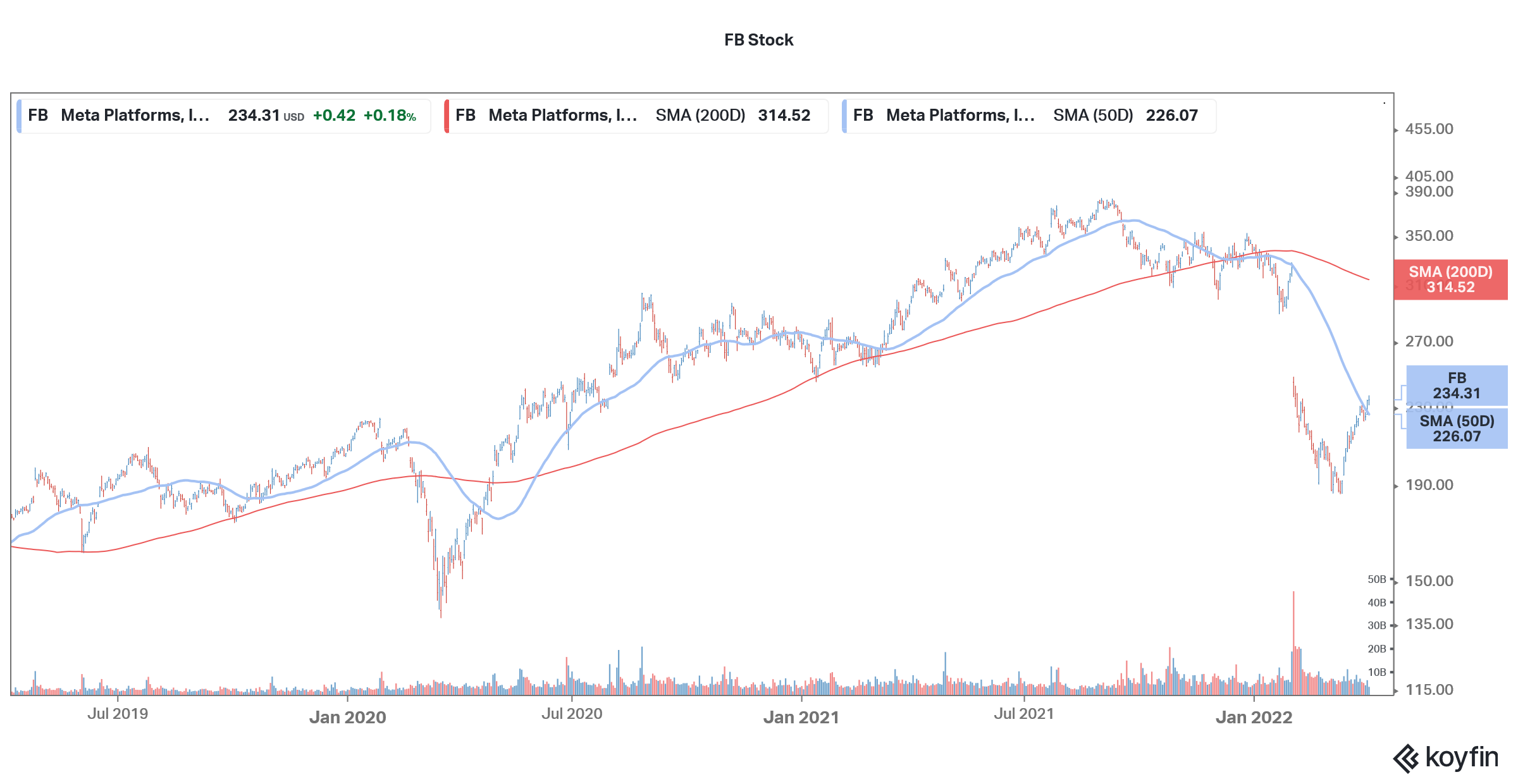

Meta Platforms stock has looked weak since the middle of 2021. The whistleblower controversy took a toll on its stock price. US lawmakers also blocked the company’s plans to launch an Instagram version for teens. However, the reach shocker came when the company released its fourth-quarter 2021 earnings.

Meta Platforms recent developments

Meta Platforms posted disappointing earnings in the fourth quarter of 2021. Its revenues increased 20% YoY to $33.67 billion in the quarter which was slightly ahead of the $33.4 billion that analysts were expecting. However, its EPS came in at $3.67 in the quarter which was below the $3.84 that analysts were expecting.

While its average revenue per user of $11.57 was higher than the $11.38 that analysts were expecting, its daily active user count of 1.93 billion was lower than the 1.95 billion that analysts were expecting. Also, it reported 2.91 billion MAUs (monthly active users), below the 2.95 billion that analysts were expecting. The company’s MAUs fell on a sequential basis in the quarter, a first in its history as a publicly-traded company.

68% of all retail investor accounts lose money when trading CFDs with this provider.

FB expects a massive hit from Apple iPhone privacy rules

If that wasn’t bad enough, the company’s guidance also spooked markets. Meta Platforms said that it expects to post revenues between $27-$29 billion in the first quarter, which was below the $30.1 billion that analysts were expecting. The company expects Apple’s iPhone privacy feature to negatively impact its sales by around $10 billion in 2022.

Starting the fourth quarter, Meta Platforms started to separately report the financials for its Reality Labs, which is building the metaverse. In 2021, the Reality Labs operation lost $10.2 billion. The losses don’t look surprising as the company is investing billions in building the metaverse. These investments would pay off in the long term even as they are a drain on the company’s profitability for now.

Wall Street is warming up to Meta Platforms stock now

While many Wall Street analysts lowered FB’s target price after the fourth-quarter earnings release, they have been warming up to the stock of late. Today, UBS raised its target price on the stock from $280 to $300 and said that markets are getting too apprehensive about the various risks associated with Meta Platforms.

“We believe Instagram Newsfeed changes and improving Reels content/algo can drive better engagement that we expect to monetize later in 2022 and in 2023,” said UBS analyst Lloyd Walmsley in his note. He added, “While the timing is unclear, we think a ramp in Reels monetization, easing comps, and improvements in targeting/measurement can drive the multiple back towards its 3-year average of a ~9% premium to the S&P 500.”

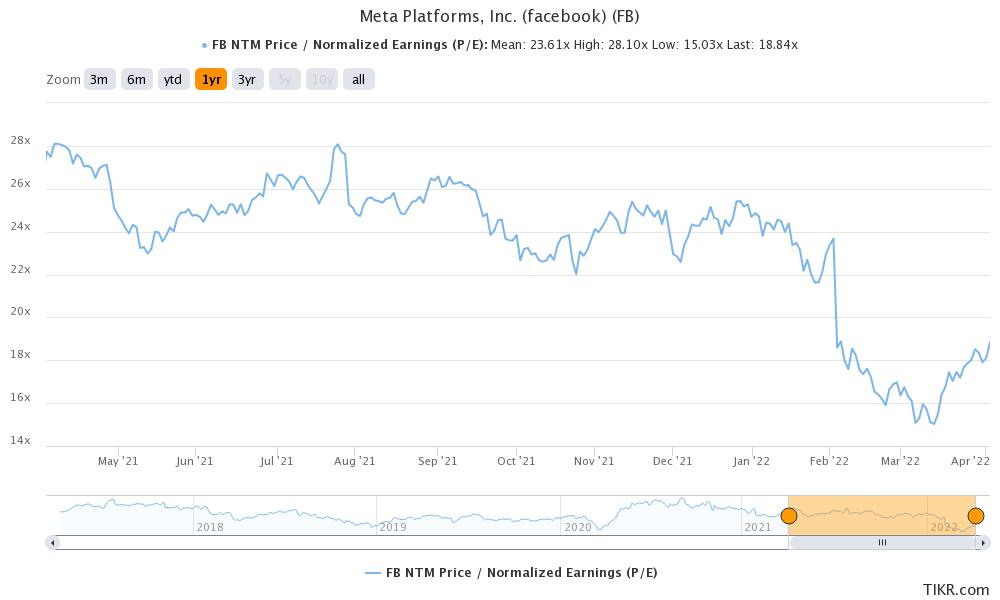

FB stock’s valuation multiples have tumbled

Notably, Meta Platforms was the cheapest FAANG stock based on forward PE multiples. The stock’s valuation multiples have contracted further after the steep fall and it now trades at a discount to S&P 500. While there are genuine concerns over FB and its business practices, the valuation looks too cheap to ignore.

Even Mohnish Pabrai believes that FB stock can easily double over the next couple of years. Notably, Pabrai hasn’t even accounted for any contribution from the metaverse business.

Jefferies reiterates Meta Platforms as a buy despite headwinds

Last week, Jefferies reiterated its buy rating on Meta Platforms stock even as it pointed to several headwinds. It said, “Key takes from our call with an ad agency expert: 1) Macro softness and tougher comps should drive slower digital ad growth in ’22 vs. ’21. 2) FB’s Q1 ad budget grew 9% y/y with our expert forecasting 11% growth in Q2. 3) TikTok growth is impressive, but young demographic and lack of audience data are gating factors for broader advertiser adoption.”

FB stock forecast

Wall Street analysts are reasonably bullish on Meta Platforms stock. 38 analysts have a buy or equivalent rating on Meta Platforms stock while 17 have a hold rating. One analyst rates the stock as a sell. Its median target price of $322.50 is a premium of almost 38% over current prices.

Meta Platforms stock long term forecast

The long-term forecast for Meta Platform stock looks positive. It has a strong moat in social media which is difficult to emulate given the network effect. There has been a rise in conservative social media networks. However, unlike Twitter, which has faced the ire of conservative audiences multiple times, FB hasn’t faced much backlash from those on the right of the political divide.

Also, metaverse could be a key long-term driver for Meta Platforms stock. The company is trying to have the first-mover advantage in the industry and if the plan succeeds it could take the stock much higher in the long term.

Should you buy FB stock?

Meta Platforms has been in one or other controversy and its ad practices can be creepy for many users. That said, from an investment perspective, FB stock looks like an island of undervaluation in a market that otherwise looks a bit stretched.

Buy FB Stock at eToro from just $50 Now!