Peloton Stock Price Forecast March 2022 – Time to Buy PTON Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

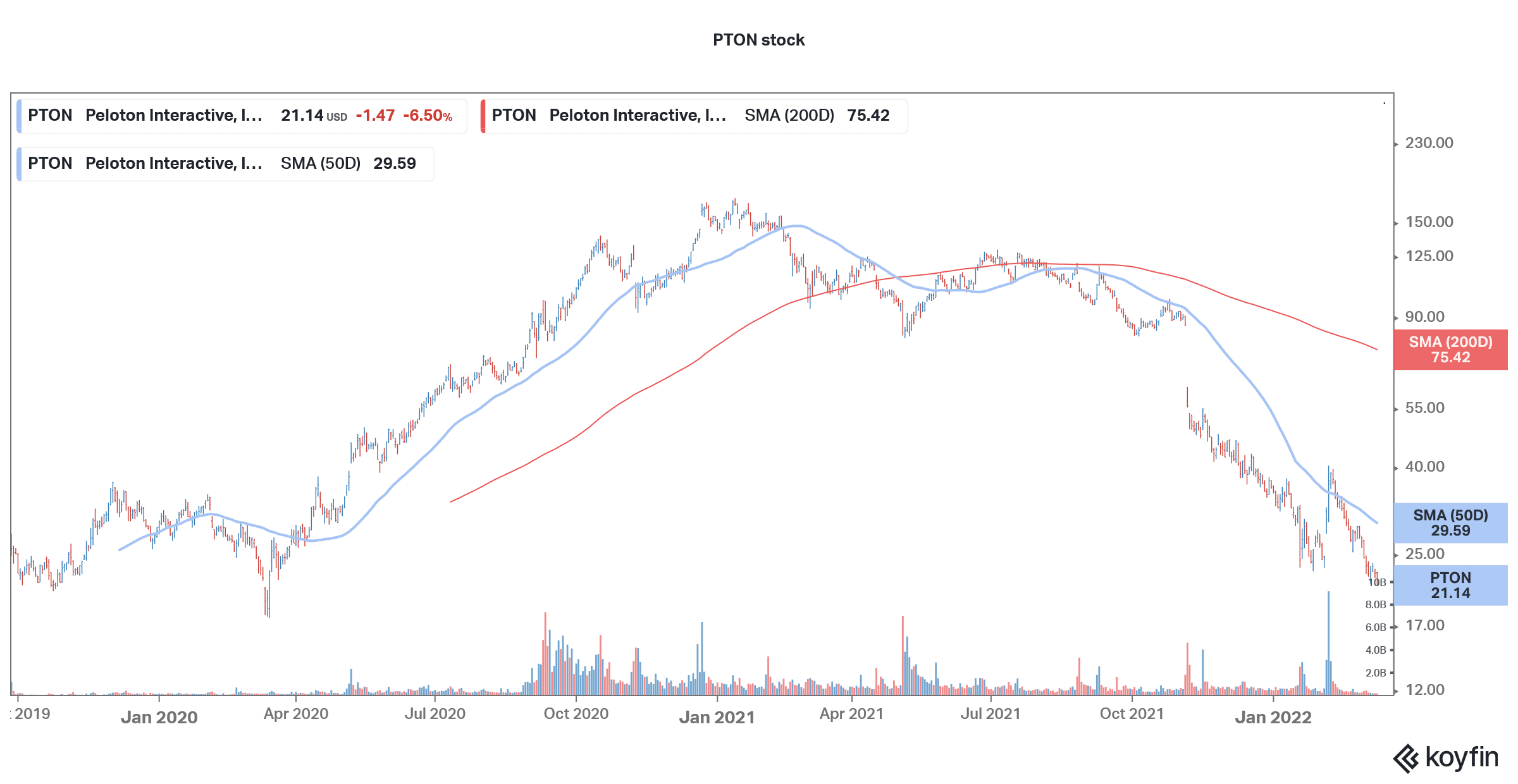

With a YTD loss of almost 40%, Peloton (PTON) stock is among the worst-performing stocks of the year. The stock hit a new 52-week low on Friday amid the broader market sell-off. Company-specific troubles have also been troubling the home fitness company.

In 2021, PTON stock fell 76% and was the worst-performing Nasdaq stock. While the entire stay-at-home pack saw selling pressure, PTON was especially under pressure. The stock had risen 440% in 2020 as stay-at-home stocks rallied. However, now the stock has fallen to levels where it traded during the March 2020 sell-off. It is now well below its IPO price. What’s wrong with PTON stock and should you buy the dip in the stock?

Peloton stock recent developments

Peloton is testing a new pricing model where the customer can buy the bike and the bundled monthly subscription for a monthly fee. Previously, the company used to offer the products on a standalone basis, and the connected fitness service was offered as a subscription. Now, as part of the business restructuring, the company is experimenting with new business models, hoping to increase its customer base.

This is among the changes that PTON’s new CEO Barry McCarthy has been working on. He took over the baton from the company’s CEO and co-founder John Foley who quit amid the crash in the stock price. In an interview with Jim Cramer last month, McCarthy had said, “I think there’s enormous opportunity for us to flex the business model and dramatically increase the [total addressable market] for new members by lowering the cost of entry and playing around with the relationship between the monthly recurring revenue and the upfront revenue.”

68% of all retail investor accounts lose money when trading CFDs with this provider.

McCarthy took over the CEO from Foley

In a note to employees, McCarthy had said, “We have to be willing to confront the world as it is, not as we want it to be if we’re going to be successful.” He added, “And now that the reset button has been pushed, the challenge ahead of us is this … do we squander the opportunity in front of us or do we engineer the great comeback story of the post-Covid era?”

Meanwhile, PTON stock’s fortunes haven’t really revived under McCarthy as it continues to fall to newer lows. The broader market sell-off hasn’t been helping matters either for the company.

Will Peloton’s new business model work?

Wall Street analysts are divided on the new subscription model. BMO Capital Markets analyst Simeon Siegel is not too convinced that the model would work and is instead worried about its impact on the company’s earnings and brand image. Siegel said in his note “For a company that has been plagued with logistic issues, they are now effectively allowing people to return their piece of equipment, at a moment’s notice.” He added, “They’re actually throwing themselves more into the delivery and logistics game. Rather than walking away from it.”

Siegel is also concerned that the company’s churn rates, which are currently below 1%, could rise under the new model. He said, “But if it becomes easy to cancel, and easy to return, what’s that going to do to churn?” He added, “Does Peloton become a winter experience for customers who every year rent the bike for four months, and then give it back when the weather’s nice? That becomes a very expensive customer.”

Cowen is bullish on PTON after the new model

Meanwhile, Cowen reiterated its overweight rating on PTON stock after the new pricing model. “Underscoring the limited nature of PTON’s pricing test, customers will need to sign up either in-store or at Peloton studios, and it will not be available online, where the company presumably consummates the vast majority of hardware sales.”

Peloton stock forecast

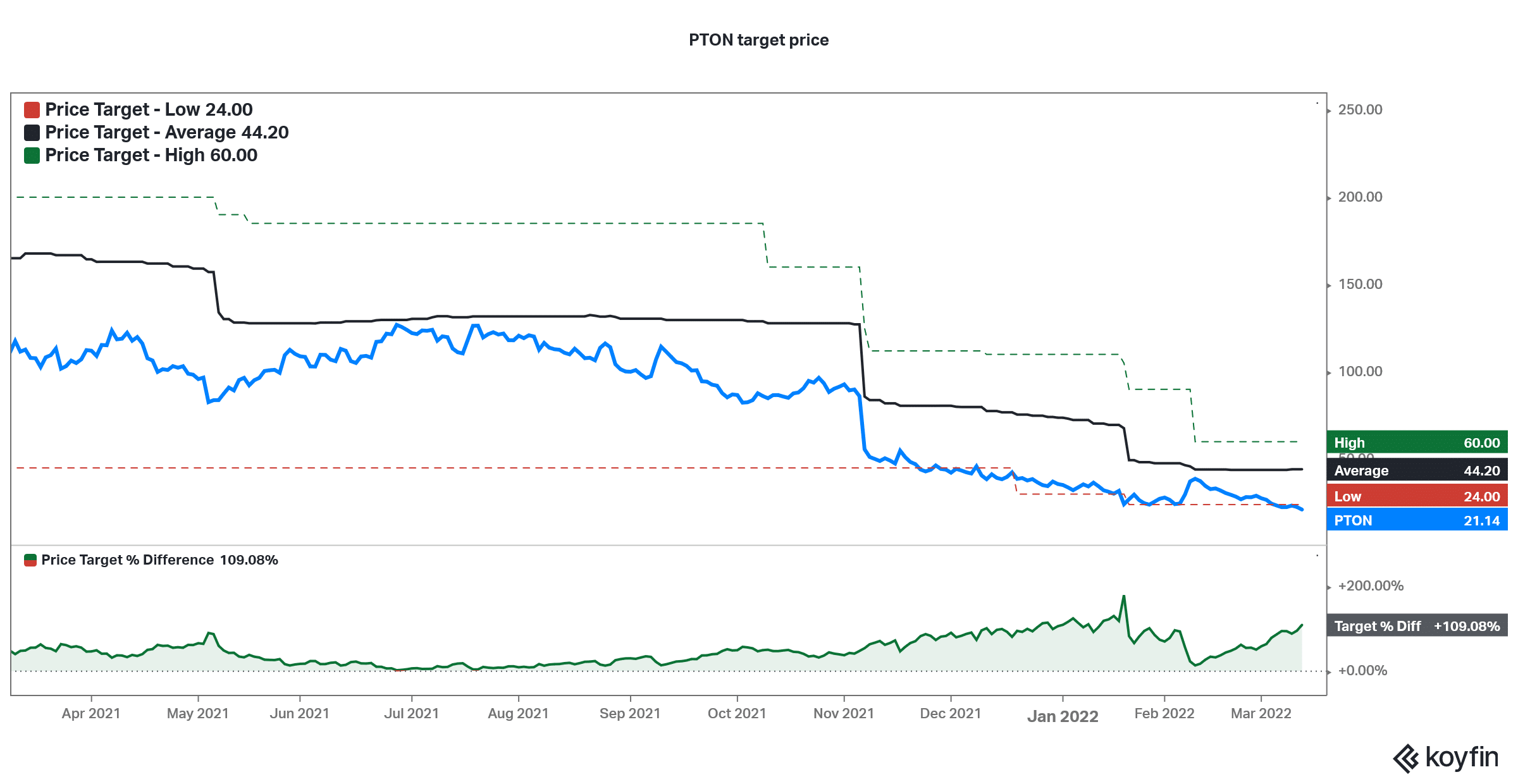

Wall Street analysts have a split rating on PTON stock. 14 out of 28 analysts polled by Koyfin rate it as a buy. 12 analysts have a hold rating while two analysts rate it as a sell. The stock’s average target price of $44.2 is a 109% premium over current prices. Wall Street analysts have been gradually lowering PTON’s target price over the last six months

PTON stock long term forecast

The long-term outlook for home fitness equipment companies like Peloton looks positive. While the growth rates of 2020 might not be sustainable, the industry should see secular growth over the long term. PTON is also building a factory in the US to support the demand.

From the home fitness market, Peloton is now also diversifying into the commercial market. Earlier this year, it had acquired Precor and is now integrating the two businesses to target the hospitality sector. International expansion would also drive value for Peloton.

We could see a hybrid model in workouts also and both gyms and home equipment companies can flourish.

Should you buy Peloton stock?

Peloton is battling several issues. The company’s sales growth has come down and the brand has been tarnished after the fatal accident last year. In what looked damaging for Peloton’s brand, a fictional character in Sex and the City died while using Peloton equipment. While the company hit out at the ad with a counter ad, there has been a lot of damage to the brand.

It also had to lower its financial projections. Also, on the costs side, it is facing higher costs which it might need to pass on to the customers. The new pricing model also looks risky for PTON.

The stock’s valuation has now come down and it trades at an NTM (next-12 months) EV-to-sales multiple of 1.8x and the market cap is just around $7 billion. While the stock looks attractive at these levels, it might continue to remain under pressure in the short term amid the broader market sell-off.

Buy PTON Stock at eToro from just $50 Now!