Lyft Stock Price Down 4% Today – Time to Buy LYFT Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

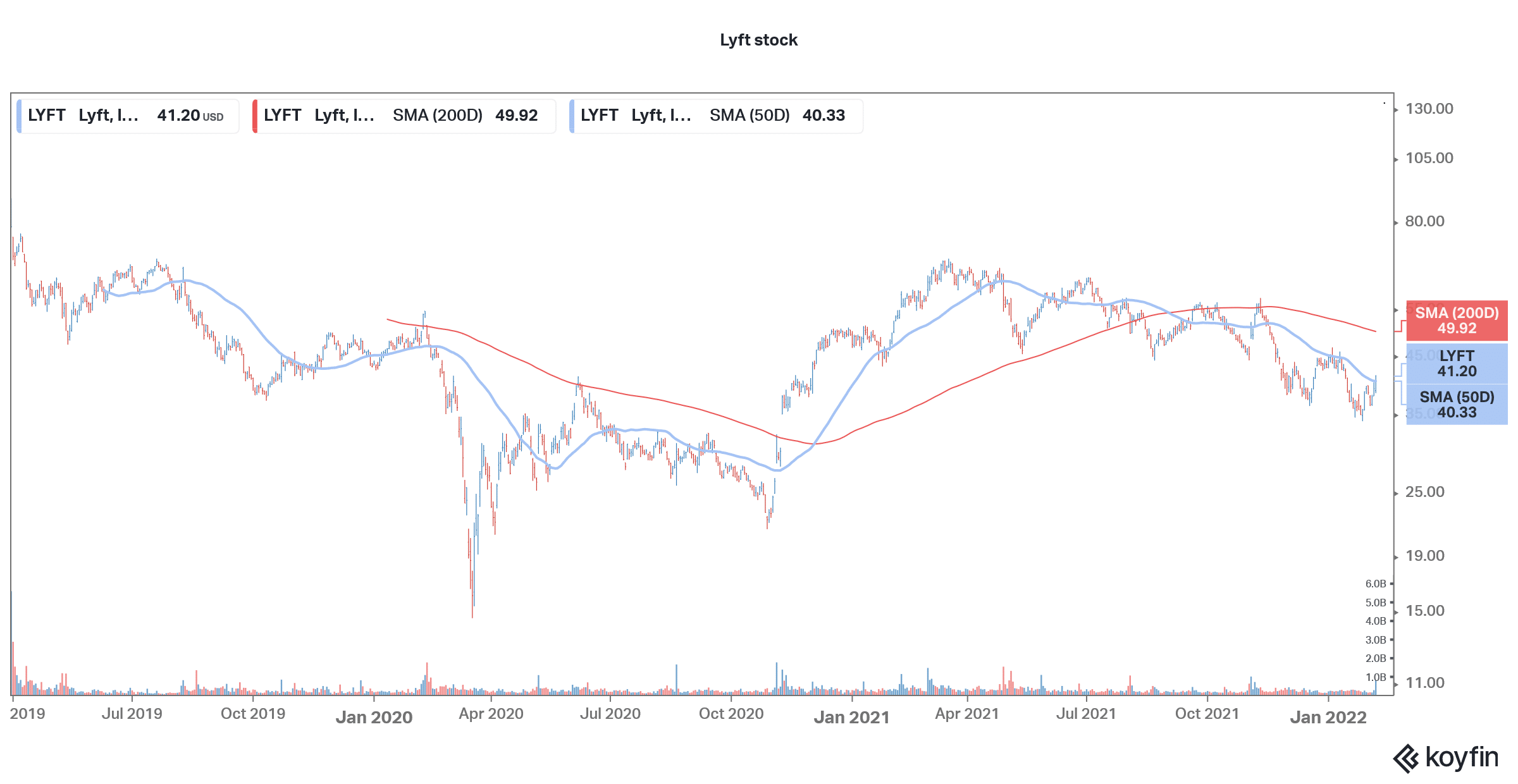

While Lyft (LYFT) stock gained over 5% yesterday, it is down almost 4% in today’s pre-market price action. The stock is now down almost 40% from its 52-week highs and is in a deep bear market. What’s the forecast for Lyft stock and is it a good buy in February 2022?

The crash is not limited to Lyft alone and we have seen sharp downwards price movement in other ride-hailing and delivery companies like Didi, Uber, DoorDash, and Grab.

Ride-hailing and delivery stocks have been weak

Lyft went public in 2019 and priced the IPO at $72. The stock saw a brief pop following the IPO but has since consistently traded below the IPO price. Uber is no different and the stock also trades well below the IPO price. Didi has been another disaster but the Chinese ride-hailing company’s misfortunes are more related to China’s tech crackdown and its eventual delisting than any industry-specific factor.

DoorDash was an outlier and was trading above the IPO price. However, it has also fallen prey to the sell-off in growth names. Southeast Asian ride-hailing company Grab has been another wealth destroyer for investors. It went public through SPAC and now trades at a discount of almost 50% from the SPAC IPO price. The stock briefly fell into the penny stock category and even now is not far away from the threshold price of $5.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Lyft stock latest developments

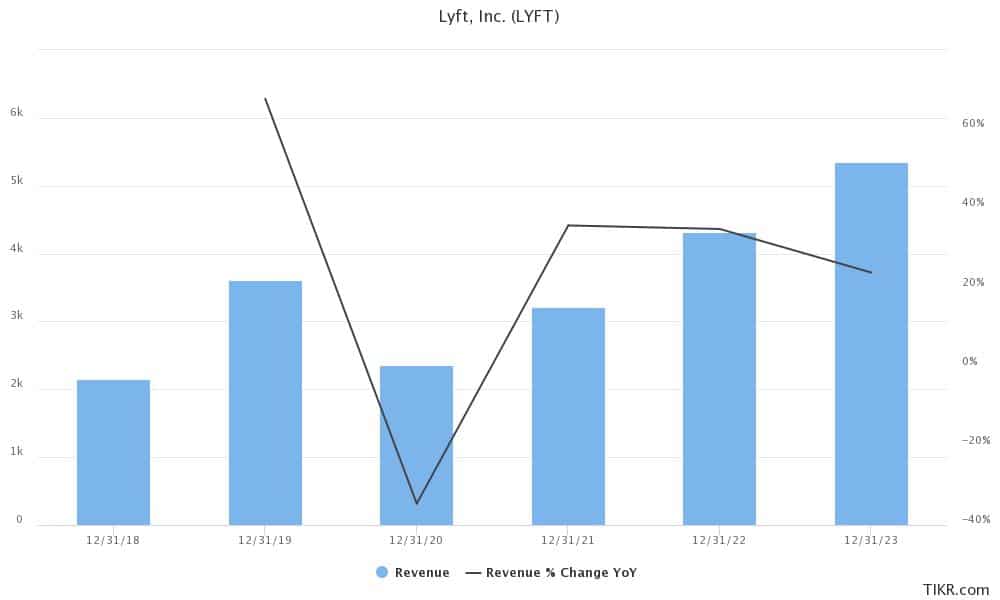

Lyft reported its fourth-quarter earnings yesterday after the close of markets. The company reported revenues of $970 million which were higher than the $940.1 million that analysts were expecting. It reported revenues of $3.2 billion in the full year which were 36% higher than the previous year. While the company termed the performance as “solid” it was a mixed bag considering the Wall Street expectations.

The company’s ride volumes hit a pandemic high during the quarter. Its contribution margin, revenue per active rider, and adjusted EBITDA also soared to a record high in the quarter. Its adjusted EPS of 9 cents was also slightly higher than the 8 cents that analysts were expecting.

Its GAAP loss in the full year was $1 billion, which is below the $1.8 billion that it posted in the previous year. Stock-related compensation was the biggest contributor to the net loss. While companies try to exclude the stock compensation in adjusted earnings, which is a perfectly legit practice, for all practical purposes it is as much an expense as employee salaries and bonuses.

Outlook

While Lyft’s financial performance was better than street expectations on most metrics, its active riders were 18.73 million in the quarter, which was below the 20.2 million that analysts were expecting. Meanwhile, what made the markets apprehensive was the company’s guidance.

Omicron wave dented the fortunes

It expects the omicron wave in the US to dent its financial performance in the first half of 2022. In the first quarter, it expects revenues to fall to between $800-$850 million, which is way below the $990 million that analysts were expecting. It expects the adjusted EBITDA to be between $5-$15 million, as compared to the $75 million that it posted in the fourth quarter. We have seen something with several companies including Netflix and Meta Platforms. While their earnings were largely in line, the guidance took a toll on their shares.

Sounding upbeat on the company’s fortunes, Lyft’s new CFO Elaine Paul said “Despite short-term headwinds from omicron, we remain optimistic about full-year 2022.” The company said that if not for the omicron wave it would have seen the revenues rise on a sequential basis in the quarter.

Lyft stock forecast

Of the 42 analysts covering Lyft, 27 have rated it as a buy while 13 have a hold rating. The remaining two analysts have a sell rating. Its median target price of $59 is a premium of 43% over current prices while the street high target price of $85 is a premium of 106%.

Last month, Jefferies downgraded Lyft stock from a buy to neutral. While it said that the company is a “Strong #2 in the U.S. duopoly for ride-hailing. Pure-play, N.A. focused, on-demand transportation platform that is levered to post COVID recovery,” it said that it prefers Uber.

Analysts prefer Uber

Needham also prefers Uber over Lyft. Notably, Uber has been working on its perennial losses and has exited several money-losing businesses like the flying taxi and autonomous driving verticals. Also, it’s a dual play on both food delivery and ride-hailing. After exiting some markets, it is now only present in markets where it has a strong competitive position. One overhang for Uber stock has been its stake in Didi which it got after selling its Chinese operations. Didi stock has plummeted after the delisting news and so has the dollar value of Uber’s investment. SoftBank, which is the largest stockholder in Didi and some other Chinese companies like Alibaba, has been the worst affected by the slide in Chinese stocks.

Should you buy Lyft stock?

Lyft stock trades at an NTM (next-12 months) EV-to-EBITDA multiple of 3.1x which is slightly below Uber’s 3.27x. The valuation discount is similar to what we’ve seen historically. Meanwhile, Didi trades at a steep discount to US ride-hailing apps, a reflection of how much damage China’s tech crackdown has done for the country’s tech giants.

From a technical perspective, Lyft has been facing strong resistance at the 50-day SMA (simple moving average). It crossed above the trendline recently but looks set to fall again looking at the pre-market price action. Lyft also trades below the 200-day SMA.

All said, Uber could be a better bet than Lyft at these price points. The company has a market-leading position and the food delivery business makes it a better investment proposition.

Buy LYFT Stock at eToro from just $50 Now!